THE CONSTRUCTION OF ECONOMIC MODEL EVALUATION

SYSTEM BASED ON THE ECONOMIC MODEL OF RESOURCE

PLATFORM

Rong Ruan, Zhenji Zhang

School of Economics and Management, Beijing Jiaotong University, Haidian District, Beijing, China

Jingjing Meng

School of Economics and Management, Beijing Jiaotong University, Haidian District, Beijing, China

Keywords: Economic model, Evaluation system, Index, Weight, Analytic hierarchy process, Capability coefficient.

Abstract: With the development of computer and information technology, more network technology have been

applied into teaching area. The economic model resources platform is firstly built by schools of economics

and management, which hosting a economic model library. And those models come from classical or

innovation models and are built by teachers and students, using technologies such as Matlab and website

development to display on the platform. As one kind of teaching resources, the economics model should be

well built on the platform to enable the learners easily understanding. Then what standard can we find to

determine the quality of the economic models? So we need construct a evaluation system to help students

select models for learning. This article combines AHP with qualitative and quantitative method and Delphi

to construct the evaluation system. Finally we applicate the system to evaluate the economic models. It can

help the learners to select high quality models. And for the bad quality models, the managers can improve

them.

1 INTRODUCTION

With the rapid development of information

technology, network technology has been inserted in

teaching (Huang Dequn, 2005). But how to raise the

quality of growing teaching resources? It becomes a

topic people concerns, especially the designing and

evaluation of the network resources.

In order to study the interdependence quantitative

relationship between economic phenomena and help

people solve real economic problems, we build the

economic model library. For example,

Black_Scholes Options Pricing Model and Cartel

model of oligopoly market. Its website is

http://211.71.64.167/exper.

Now the quality of the models is uneven, how to

judge those models' quality and give reference for

the teachers and students has become the focus of

the model management. This article gives researches

on how to construct and use the economic model to

evaluation system by using AHP from management

and development perspective.

2 CONSTRUCT EVALUATION

INDEX SYSTEM OF

ECONOMIC MODELS

The economic model evaluation system is study on

the economic models on the platform, and it is used

by the manager and users of the platform. Whether a

model has the value to learn, the standard we trust is

very important.

We use analytical method (Sun Wenhong, 2010)

and AHP (Jin Zhilong, 2009) to get the evaluation

index system, following the two principles (Zhao

Yang, 2006): comprehensive and independent.

According to the principle of AHP, we divide the

system into three lever: target, rule and program

layers (Xu Wenxue, 2010). After consulting criteria

376

Ruan R., Zhang Z. and Meng J..

THE CONSTRUCTION OF ECONOMIC MODEL EVALUATION SYSTEM BASED ON THE ECONOMIC MODEL OF RESOURCE PLATFORM.

DOI: 10.5220/0003547603760379

In Proceedings of the 13th International Conference on Enterprise Information Systems (ICEIS-2011), pages 376-379

ISBN: 978-989-8425-53-9

Copyright

c

2011 SCITEPRESS (Science and Technology Publications, Lda.)

of teaching resources and combining the

characteristics of the economic models, we get the

target layer indicators. Then we use analytical

method to decompose the target layer indicators one

by one (Zhuang Yu, JI Meiru, 2008), and we get 11

indicators of the rule layer. Similarly as the program

layer indicators. Evaluation is like the table 2.

3 THE WEIGHT

DETERMINATION OF THE

ECONOMIC MODEL

EVALUATION SYSTEM

Because mature and easily to use, this article initially

adopts AHP method after comparison. There are 5

steps to determine the weight:

Step 1: Structuring Variables

As mentioned above, the first-level indicators are

assumed to A1, A2, A3, A4.then its corresponding

second-level indicators were set to B1m, B2n, B3k

(m, n, k are natural number). The same as the third-

level. The corresponding weight of the first-level

indicators are assumed as

w

1

,w

2

,w

3

,w

4

, then:

4

1

0 1 ( 1,2,3) (1)

1 (2)

i

i

i

iω

ω

=

⎧

≤≤ =

⎪

⎪

⎪

⎪

⎨

⎪

=

⎪

⎪

⎪

⎩

∑

Step 2: Constructing the Matrix

When comparing the same level indicators, it can

generally use "important", "slightly important ",

"obviously important ", "extremely important " to

describe the importance of one factor relative to

another factor. The results of pair wise comparison is

denoted in 1-9 scale (Wang Hao, Ma Da, 2003).

We invited 55 experts to rate economic model in

order to create a comparison matrix by questionnaire

and we got the initial data.

Steps 3: Calculating Index Weight and the Largest

Eigen Value

Determine the matrix data (Table 3 2-5 data) in

accordance with the formula and calculate the

maximum eigen value of each index and weight, the

results in Table 1.

Step 4: Consistency Test

Because the matrix structure made by the experts

do not necessarily meet the matrix consistency. In

order to limit this error, it is necessary to test the

consistency. Denoted by:

, (n is equal to the number of

indicators in matrix.)

If

2n ≤

,the matrix is always exactly the same, it

means

0CI =

.When

2n >

,the matrix's consistency

index and the ratio of the average random

consistency index are random consistency ratio. We

denote it as:

RC

.

If

R<0.1C

, the comparison matrix has satisfactory

consistency and the calculated feature vector is

reliable. Otherwise it needs to re-adjust the matrix

until with satisfactory consistency.

After calculation, all comparison matrix are

consistent, and the results credible.

Step 5: Calculation of the Total Weight

Following the step4 we can calculate every

indicator's weight and test its consistency.

Supposing the indicator i 's weight is equal to

a

i

,

its j secondary-level indicator's relative weight is

j

b

.Then this secondary-level indicator's total weight

is

ij

ab

×

.

Then use the following formula to calculate the

total random consistency index:

1

1

n

ii

i

n

ii

i

aCI

CR

aRI

=

=

=

∑

∑

While:

i

a

: the i first-level indicator's weight.

i

CI

:

the i first-level indicator's consistency index

value.

i

RI

:

the i first-level indicator's average random

consistency index values.

The final overall consistency test result is

0.028312 which is far less than 0.1. So it is

consistent with consistency. Evaluation index

system's weights are shown in Table 2.

4 VALIDATIONS AND

APPLICATION OF THE

EVALUATION SYSTEM

4.1 Example Demonstrating of the

Evaluation System

When an evaluation system is established, we need

to verify its validity and rationality. We do a

sampling survey and use two methods (lever

evaluation and evaluation system) to test the quality

of the models. By comparing the two groups, they

match very well. Through this validation, it indicates

max

1

n

CI

n

λ −

=

−

THE CONSTRUCTION OF ECONOMIC MODEL EVALUATION SYSTEM BASED ON THE ECONOMIC MODEL

OF RESOURCE PLATFORM

377

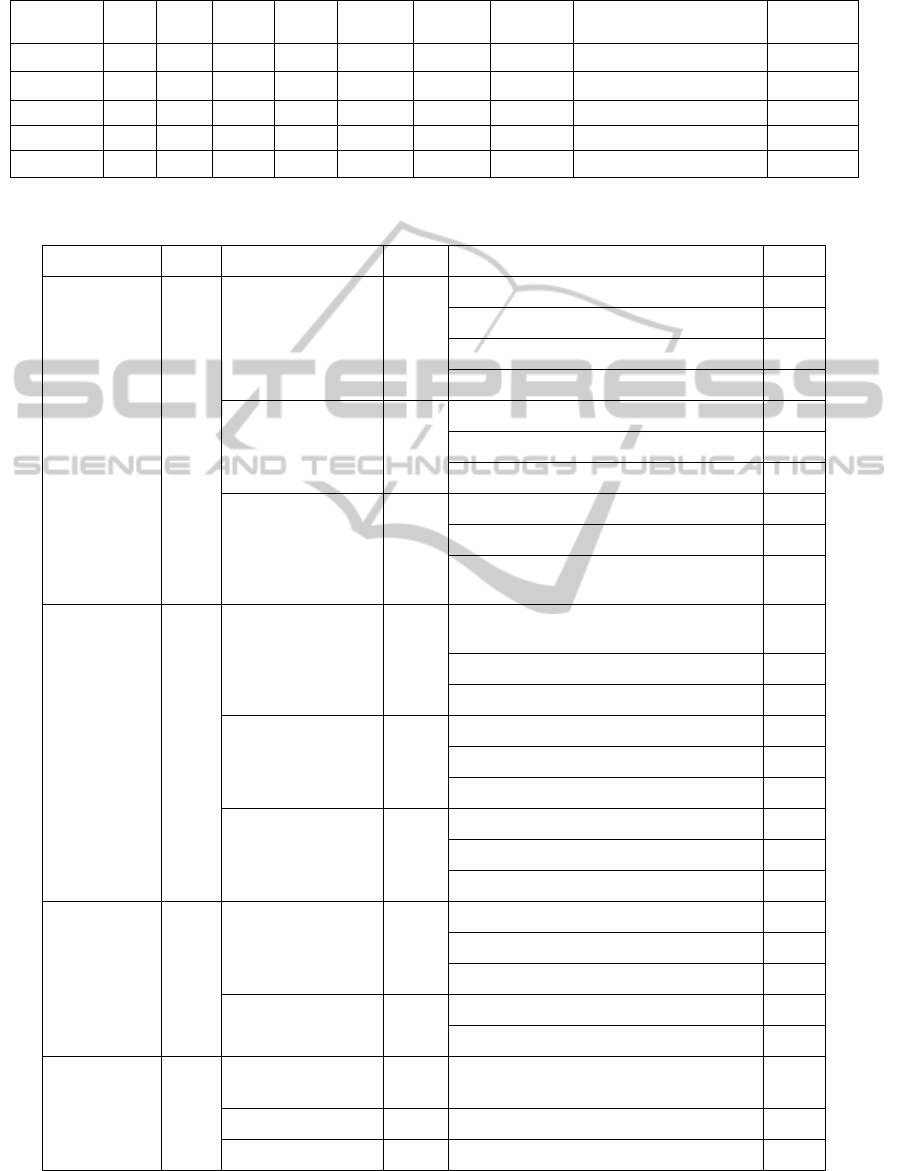

Table 1: Single evaluation index weights and the largest Eigen value.

Indicators A B C D Mi Wi (AW)i maximum Eigen value weight

A 1 2 2 1 1.41 0.34 2.04 0.696 0.505

B 0.5 1 2 2 1.19 0.29 1.58 0.451 0.327

C 0.5 0.5 1 1 0.71 0.17 0.51 0.087 0.063

D 1 0.5 1 1 0.84 0.20 0.71 0.144 0.104

total 4.15 1 1.378

Table 2: Evaluation of economic models and the corresponding weight.

A Target layer

B Rule layer

C Project layer

1 content 0.276

11 Integrity 0.124

111 Theoretical source

0.029

112 Assumptions

0.017

113 Theory to explain

0.048

114 Analysis

0.047

12 Accuracy 0.089

121 Interpretation accuracy

0.038

122 The accuracy of the understanding

0.018

123 Whether to seize the essence

0.027

13 Understandability 0.063

131 Example

0.018

132 Analogy to explain

0.009

133 Whether has interpretation of the

academic term

0.036

2 Technical 0.455

21 Operability 0.256

211 Whether the output of experimental

operation

0.148

212 Whether the result is that the process

0.053

213 Whether has input data validation

0.053

22 Friendly interface 0.067

221 Tips range of input data

0.028

222 Sample data

0.016

223 The reasonable of the control

0.022

23 Experiment to

explain

0.131

231 Experiment description

0.041

232 Interpretation of results

0.057

233 whether is the steps to explain logical 0.030

3 effectiveness 0.102

31 Intuitive 0.027

311 Text

0.015

312 Graphic description

0.008

313 Other visual presentation methods

0.004

32 Data Validation 0.075

321 The length of time to get result

0.054

322 Error rate 0.018

4 application 0.167

41 Case relevance 0.096 0.096

42 Case Study 0.035 0.035

43 Questions 0.035 0.035

ICEIS 2011 - 13th International Conference on Enterprise Information Systems

378

that the evaluation system is reasonable and

available.

4.2 The Application and Achievement

of the Evaluation System

After constructing the evaluation system, this article

introduced the correlation coefficient method (Wang

Sufen, 2007) and use the weighted average to

represent the quality. And we use the Asp and Ajax

technology to set up the system on the platform and

let it function on the management of the models.

5 CONCLUSIONS

After constructing the evaluation system, we apply it

in the evaluation of economic models on the

platform. By evaluating all models on the platform,

we can get a overall understanding of the quality of

all the economic models. Also we can know the

quantity of models on every lever. According to the

statistical results, now there are 22 models in good

lever, 110 models in middle and 38 models needing

to be improved. The evaluation result helps the

learners to select high quality models to learn, also it

provides foundation of model management for

manager.

Building a suitable and scientific evaluation

system for the pioneering economic models has been

finished, but its follow-up work which how to make

the evaluation system function well need continuing

researching. So next step we need to study the

operating mechanism of the evaluation system.

ACKNOWLEDGEMENTS

In this thesis writing process, we give special thanks

to my mentor's guidance and supervision and thank

her for understanding and tolerance.This article has

referenced to the large number of documents,and we

pay tribute to all the academic predecessors!

REFERENCES

Huang Dequn. The research based on the network teaching

evaluation [J]. Journal of remote education

magazine

2005, (4): 23-26.

Jin Zhilong, Li Duanmei. Local research institutions

performance evaluation indicator and its weight

calculation [J]. Journal of technical management

research, 2009, (12): 103-106.

Sun Wenhong. The safety evaluation index weight study

based on the analytic hierarchy process (AHP) railway

dangerous cargo standing[J]. Railway operation

technology, 2010,(2): 55-58.

Wang Hao, Ma Da. AHP scale-free evaluation and new

scale method [J]. Journal of system engineering theory

and practice, 2003, (9) : 82-86.

Wang Sufen. The methods using the correlation coefficient

to improve the principle and grading [J]. Journal of

simulation experiment on information technology,

2007, (17): 37.

Xu Wenxue. AHP in financial warning index weight the

design application [J]. Journal of accounting new

horizons, 2010, (1): 20-2

ZhaoYang. Project management achievement evaluation

system [D]. Beijing: university of north China: electric

power management science &engineering, 2006.

Zhuang Yu, JI Meiru. A Data Analysis of the Index

System of Assessment Water environmental Carrying

Capacity The National Social Science Foundation

2008 pp 1-4.

THE CONSTRUCTION OF ECONOMIC MODEL EVALUATION SYSTEM BASED ON THE ECONOMIC MODEL

OF RESOURCE PLATFORM

379