ADAPTIVE CONTINUOUS HIERARCHICAL MODEL-BASED

DECISION MAKING

For Process Modelling with Realistic Requirements

Kamil Dedecius

Institute of Information Theory and Automation, Academy of Sciences of the Czech Republic

Pod Vod´arenskou vˇeˇz´ı 4, 182 08 Prague, Czech Republic

Pavel Ettler

COMPUREG Plzeˇn, s.r.o., N´adraˇzn´ı 18, 306 34 Plzeˇn, Czech Republic

Keywords:

Bayesian modelling, Hierarchical model, Parameter estimation, Cold strip rolling, Rolling mills.

Abstract:

Industrial model-based control often relies on parametric models. However, for certain operational conditions

either the precise underlying physical model is not available or the lack of relevant or reliable data prevents its

use. A popular approach is to employ the black box or grey box models, releasing the theoretical rigor. This

leads to several candidate models being at disposal, from which the (often subjectively) prominent one is se-

lected. However, in the presence of model uncertainty, we propose to benefit from a subset of credible models.

The idea behind the multimodelling approach is closely related to hierarchical modelling methodology. By

using several modelling levels, it is possible to achieve relatively high quality and robust solution, providing a

way around typical constraints in industrial applications.

1 INTRODUCTION

Industrial model-based control or prediction is con-

nected with several practical but often contradictory

requirements:

– The model should respect physical relations of the

process yet be simple enough;

– The model should approximate process behaviour

in all possible working conditions;

– Imperfection of measured data feeding the model

should not deteriorate control or prediction qual-

ity.

Possible solution of the first two above-mentioned is-

sues consists in switching amongseveral proven mod-

els according to actual working conditions. The third

problem is much more difficult to be solved in princi-

ple. The data driven (black box) models could seem

to be most appropriate but they almost always con-

tradict the first two requirements. See, e.g., (Bohlin,

1991) for remarks on black and grey box modelling.

On-line mixing of several proven process mod-

els – which can be considered as continuous decision

making – turns out to be a solid compromise solution

of all three requirements, at least for the process of

cold strip rolling from which comes the motivation

for this research (Ettler and Andr´ysek, 2007).

The presented method of model mixing is closely

related to dynamic model averaging (Raftery et al.,

2010). However, two additional requirements stimu-

lated the need for a specific solution:

– Sum of weights corresponding to particular mod-

els is required to be always equal to one;

– An offset term should be continuously estimated

to eliminate any residual discrepancy, whatever it

comes from.

While the first restriction can be easily justified

from the probabilistic point of view, insistence on the

second requirement comes purely from practical ex-

perience, although the existence of the offset might

theoretically be superfluous. Presented solution at-

tempts to reconcile both requirements.

The method is developed in the Bayesian frame-

work, treating the unknown parameters as random

variables. Each model is represented by a condi-

tional probability density function (pdf) of the mod-

elled variable, given a set of features and parameters.

The layout of the paper is as follows: Section 2 de-

scribes the structure of the multimodel and its levels;

in Section 3 we derive a particular case of the model.

284

Dedecius K. and Ettler P..

ADAPTIVE CONTINUOUS HIERARCHICAL MODEL-BASED DECISION MAKING - For Process Modelling with Realistic Requirements.

DOI: 10.5220/0003533402840289

In Proceedings of the 8th International Conference on Informatics in Control, Automation and Robotics (ICINCO-2011), pages 284-289

ISBN: 978-989-8425-74-4

Copyright

c

2011 SCITEPRESS (Science and Technology Publications, Lda.)

Section 4 contains an example of application. Finally,

Section 5 concludes the achievements.

2 HIERARCHICAL MODELLING

CONCEPT

Assume, that there is a stochastic system observed at

discrete time instants k = 1, 2, . . . , which is to be mod-

elled. The statistical framework employs, among oth-

ers, parametric models, expressing the dependence of

the output variable of interest y

k

on a nonempty or-

dered set of observed data

D (k) = {d

κ

}

κ=0,...,k

, d

κ

∈ R

n

.

d

0

is the prior knowledge represented, for instance,

by an expert information or a noninformative distri-

bution. The task is to predict the future output y

k+1

,

e.g., for control.

Often there is a whole set of available models,

mainly those based on underlying physical principles

of the process. However, since in many applications

either the precise physical model is not available or

the lack of reliable data prevents its use, the user em-

ploys black box or grey box models. Then, either the

(subjectively) best model or models are selected and

switched or, alternatively, a rich-structure model be-

ing a union of several candidate models is built. De-

spite the potential applicability of the latter case, the

over-parametrization in combination with unreliable

measurements and their traffic delays is expected to

be fatal.

Our method provides a way around most of disad-

vantages of the mentioned approaches. We propose a

hierarchical model composed of three levels:

Low-level Models comprise arbitrary count of plau-

sible parametric models like the regressive and the

space-state ones. They are independent of each

other, but their aims are identical – modelling of

the same quantity of interest.

Averaging Model is intended for merging the infor-

mation from the low-level models. The resulting

mixture of predictive pdfs of low-level models,

weighted by their evidences, is used to evaluate

the predictions.

High-level Model – since industry has several spe-

cific requirements related, e.g., to stable control,

we add a high-level model. It provides stabiliza-

tion of the prediction process. However, the goal

of this level can differ from case to case according

to specific needs of the field of application being

addressed.

The ensuing sections describe these levels in some de-

tail.

2.1 Low-level Models

The low-level modelsexpress the relationbetween the

actual system output y

k

and the given data D (k) by a

pdf

f(y

k

|D (k− 1), Θ), (1)

where Θ denotes a multivariate finite model parame-

ter which, underthe Bayesian treatment, is considered

to be a random variable obeying pdf

g(Θ|D (k− 1)). (2)

If this pdf is properly chosen from a class conjugate

to the model (1), the Bayes’ theorem yields a poste-

rior pdf of the same type (Bernardo and Smith, 2001).

Then, the rule for recursive incorporationof new mea-

surements into the parameter pdf reads

g(Θ|D (k)) =

f(y

k

|D (k− 1), Θ)g(Θ|D (k− 1))

I

k

,

(3)

where

I

k

=

Z

f(y

k

|D (k− 1), Θ)g(Θ|D (k− 1))dΘ (4)

= f(y

k

|D (k− 1)) (5)

is a normalizing term. It assures unity of the resulting

pdf and it is a suitable measure of model’s fit, often

called evidence. The equality of (4) and (5) follows

from the Chapman-Kolmogorov equation (Karush,

1961). Furthermore, this equation also yields the pre-

dictive pdf f (y

k+1

|D (k)) providing the Bayesian pre-

diction, formally

f(y

k+1

|D (k)) =

Z

f(y

k+1

|D (k), Θ)g(Θ|D (k))dΘ

=

I

k+1

I

k

. (6)

The last equality follows from the recursive property

of the Bayesian updating (3).

Although the described methodology is important

per se, it strongly relies on invariance of Θ. However,

this assumption is often violated in practical situations

and the evolution ofΘ must be appropriatelyreflected

by an additional time update according to model

g(Θ

k+1

|Θ

k

, D (k)). (7)

Generally, we can distinguish two significant cases:

(i) The evolution model (7) is known a priori. Then,

Θ is called the state variable and, under certain

conditions, the modelling turns into the famous

Kalman filter (Peterka, 1981).

ADAPTIVE CONTINUOUS HIERARCHICAL MODEL-BASED DECISION MAKING - For Process Modelling with

Realistic Requirements

285

(ii) The model (7) is unknown, but slow variability

of Θ is assumed. This case is usually solved ei-

ther by finite window methods or by forgetting.

The latter heuristically circumvents the model ig-

norance by discounting of potentially outdated in-

formation from the parameter pdf. Formally, it

introduces a forgetting operator F modifying the

posterior pdf,

g(Θ

k+1

|D (k)) = F [g(Θ

k

|D (k))] .

The class of available forgetting methods com-

prises, e.g., exponential forgetting (Peterka,

1981), directional forgetting (Kulhav´y and K´arn´y,

1984), partial forgetting (Dedecius, 2010) and

others.

Since the issue of parameter variability is behind the

scope of the paper, we can stick with unsubscripted Θ

without a loss of generality.

2.2 Averaging Model

Assume that there is a nonempty finite set of differ-

ent low-level models M = {M

(1)

, . . . , M

(S)

}, S ∈ N,

which are considered as candidates to represent the

system under study. Formally, we have

M

(s)

: f(y

k

|D (k− 1), Θ

(s)

, M

(s)

), s = 1, . . . , S, (8)

which directly coincide with (1). These models are

independently evaluated in accordance with Section

2.1. Their probabilitiesare expressed by a distribution

h(M |D (k)) ≡ h(M

(1)

, . . . , M

(S)

|D (k)). (9)

The averaging model evaluates this distribution with

respect to evidences (5) of low-level models (8) on

base of marginal pdfs, namely

h(M

(s)

|D (k)) ∝ h(M

(s)

|D (k− 1)) I

(s)

k

, (10)

where ∝ denotes equality up to a normalizing factor.

The prior distribution h(M

(s)

|D (0)) can be chosen ei-

ther on base of expert information or as noninforma-

tive pdf with equal marginals.

The predictive pdf of the system output given the

set of data D (k) and the set of models M is repre-

sented by a mixture

f(y

k+1

|D (k), M )

=

K

∑

k=1

f(y

k+1

|D (k), M

(s)

)h(M

(s)

|D (k)). (11)

The point estimate of y

k+1

provides the mixture (11)

in the form of a convexcombination of weightedpoint

estimates E

h

y

k+1

|D (k), M

(s)

i

. It coincides with the

method of Dynamic model averaging (Raftery et al.,

2010).

2.3 High-level Model

The purposeof the high-level model is stabilization of

the prediction, particularly for its further use in con-

trol. Inclusion of the third modelling level is justified

by practical experience with averaging models which,

in contrast to theoretical assumptions, may provide

biased results. The most basic high-level model can

be represented by a pdf

f(˜y

k+1

|D (k), ˆy

k+1

,

˜

Θ), (12)

where ˜y

k+1

is recursively modelled given the features

– point estimates of ˆy

k+1

obtained from the averag-

ing model. The high-level model is parametrized by

a multivariate parameter

˜

Θ. The point estimate ˜y

k+1

is the output of the hierarchical model. This provides

the solution to the task stated in Section 2.

3 ELABORATION FOR

INDUSTRIAL APPLICATION

This section elaborates the method for a particular but

important case of normal regressive models at the low

level. The generalization for another cases, e.g., the

state-space models like the Kalman filter and its vari-

ants is straightforward and the averaging model re-

mains unchanged. For the sake of convenience, the

evolution of parameters will not be discussed.

3.1 Low-level Models

We consider a normal linear regressive model with a

regressor ψ

k

∈ R

n

and a vector of regression coeffi-

cients θ of the same dimension, i.e.

y

k

= ψ

′

k

θ + e

k

, (13)

where e

k

∼ N (0, σ

2

) is the additive normal white

noise. The Bayesian framework relates it with (1)

through pdf

f(y

k

|D (k− 1), Θ) ∼ N (ψ

′

k

θ, σ

2

), (14)

where

Θ ≡ {θ, σ

2

}.

An appropriate distribution conjugate to the model

(14) is of the normal inverse-gamma type (Murphy,

2007),

g(Θ|D (k)) ∼ N iΓ(V

k

, ν

k

), (15)

where V

k

∈ R

N×N

is an extended information matrix,

i.e., a symmetric positive definite square matrix of di-

mension N = n + 1, and ν

k

∈ R

+

is a number of de-

grees of freedom. The Bayes’ theorem (3) updates

these two statistics by new data as follows:

ICINCO 2011 - 8th International Conference on Informatics in Control, Automation and Robotics

286

V

k

= V

k−1

+

y

k

ψ

k

y

k

ψ

k

′

ν

k

= ν

k−1

+ 1.

It may be proved(Peterka, 1981) thatthe estimator

of θ = (θ

1

, . . . , θ

n

)

′

is

ˆ

θ =

ˆ

θ

1

.

.

.

ˆ

θ

n

=

V

21

.

.

.

V

N1

′

V

22

. . . V

2N

.

.

.

.

.

.

.

.

.

V

N2

. . . V

NN

−1

.

This relation is equivalent to the recursive least

squares (Peterka, 1981) and it provides the estimates

for prediction with (13). The normalizing integral I

k

is nontrivial, it can be found, e.g., in (Peterka, 1981;

K´arn´y, 2006).

Since the information matrices are often ill-

conditioned and their inversions can lead to signif-

icant numerical issues, it is reasonable to evaluate

calculations on factorized forms, e.g., the Cholesky,

UDU’ or SVD ones.

3.2 Averaging Model

The averaging model introduced in Section 2.2 is re-

sponsible for merging the informationfrom the under-

laying low-level models. For the sake of better read-

ability, let us denote

α

(s)

k

≡ h(M

(s)

|D (k)).

The point prediction of the output at this modelling

level follows from (11), hence it reads

ˆy

k+1

=

K

∑

k=1

E

h

y

t+1

|D (k), M

(s)

i

α

(s)

k

. (16)

From the statistical viewpoint, two cases can occur.

The latter one is a generalization of the former one;

both are described below.

3.2.1 Two Low-level Models

Assume that we have two models M

(1)

and M

(2)

with

real nonnegative scalar statistics a

(1)

and a

(2)

. We

want these models to have probabilities α for M

(1)

and 1 − α for M

(2)

. Then, the distribution of mod-

els can be viewed as the beta distribution (Gupta and

Nadarajah, 2004) with pdf

f(α|a

(1)

, a

(2)

) =

Γ(a

(1)

+ a

(2)

)

Γ(a

(1)

)Γ(a

(2)

)

α

a−1

(1− α)

a

(2)

−1

where Γ stands for the gamma function. The point

estimate of the mean value and the variance are

ˆ

α = E

h

α|a

(1)

, a

(2)

i

=

a

(1)

a

(1)

+ a

(2)

, (17)

var(α) =

a

(1)

a

(2)

(a

(1)

+ a

(2)

)

2

(a

(1)

+ a

(2)

+ 1)

.

The rule for update of statistics a

(1)

and a

(2)

is as

follows:

a

(1)

k

= α

k−1

I

(1)

k

a

(2)

k

= (1 − α

k−1

)I

(2)

k

(18)

3.2.2 Multiple Low-level Models

The distribution of probabilities of multiple models

M

(1)

, . . . , M

(S)

can be derived as a generalization of

the beta pdf. Let a = (a

(1)

, . . . , a

(S)

) be a vector of

nonnegative real statistics. Furthermore, let us intro-

duce independent identically distributed (i.i.d.) ran-

dom variables W

(s)

∼ Γ(a

(s)

, 1), s = 1, . . . , S and set

W = (W

(1)

, . . . , W

(S)

), T =

S

∑

s=1

W

(s)

,

α = (α

(1)

, . . . , α

(S)

) where α

(s)

=

W

(s)

T

. (19)

Obviously, (19) imposes constraints α

(s)

∈ [0, 1] and

∑

α

(s)

= 1. Since the pdf of a gamma distribution for

W

(s)

is

f(W

(s)

|a

(s)

, 1) =

1

Γ(a

(s)

h

W

(s)

i

a

(s)

−1

e

−W

(s)

,

the pdf for the multivariate W with i.i.d. elements has

the form

f(W |a, 1) =

S

∏

s=1

1

Γ(a

(s)

)

h

W

(s)

i

a

(s)

−1

e

−W

(s)

.

Since α’s should sum to unity, we need only (S−

1)-variate vector α = (α

(1)

, . . . , α

(S−1)

). The change

of variables theorem (Rudin, 2006) provides a way to

interchange of W

(s)

and α

(s)

,

f(α|·) = f

W

(α|·)detJ

W →α

.

Here, J

W →α

denotes the Jacobian matrix contain-

ing partial derivatives of the projection and f

W

(α|·)

is originally a function f(W |a, 1) with α substi-

tuted for W . Since W

(s)

= Tα

(s)

is bijective for

s = 1, . . . , S− 1 andW

(S)

= T(1−α

(1)

−. . . − α

(S−1)

),

the necessary condition is fulfilled and the theorem

may be used. The determinant of the Jacobian

J

W →α

= det

∂W

∂α

,

∂W

∂T

= T

S−1

provides

f(α, T) = T

A−1

e

−T

S

∏

s=1

1

Γ(a

(s)

)

h

α

(s)

i

a

(s)

−1

,

ADAPTIVE CONTINUOUS HIERARCHICAL MODEL-BASED DECISION MAKING - For Process Modelling with

Realistic Requirements

287

where A =

∑

k

a

(s)

. Integrating T out with the rule

Z

T

A−1

e

−T

dT = Γ(A)

leads to the pdf of α as follows:

f(α|a) =

Γ(A)

∏

S

s=1

Γ(a

(s)

)

S

∏

s=1

h

α

(s)

i

a

(s)

−1

This pdf is a variant of the Dirichlet distribution

(Geiger and Heckerman, 1997), with nonnegative real

statistics a

(s)

. Since the marginal distributions are of

beta type B(a

(s)

, A−a

(s)

), the estimator of kth element

of α is

E

h

α

(s)

i

=

ˆ

α

(s)

=

a

(s)

A

=

a

(s)

∑

S

s=1

a

(s)

and its variance is

var(α

(s)

) = α

(s)

A− α

(s)

A

2

(A+ 1)

.

The rule updating statistics a

(s)

is a straightfor-

ward generalization of (18)

a

(s)

k

= α

(s)

k−1

I

(s)

k

.

3.3 High-level model

The high-level model discussed in Section 2.3 stabi-

lizes the prediction according to specific needs of the

application field of interest. In our case, we use a nor-

mal regressive model equivalent to (14) with a regres-

sor being composed of the averaging model output

ˆy

k+1

(16) and an offset term,

ψ

k

= ( ˆy

k+1

, 1)

′

D (k), M .

Its evaluation, i.e., parameter estimation and output

prediction, follows from Section 3.1.

4 REAL DATA EXAMPLE

Let us demonstrate the presented method on a simpli-

fied example. Used data come from a four-high cold

rolling mill and the aim consists in reliable instanta-

neous prediction of the output strip thickness devia-

tion (denoted h

2

), measurable only with a significant

time delay. The true evolution of the modelled out-

put strip thickness deviation (h

2

) is depicted in Fig. 1.

Apparently, we can experience modelling difficulties

around k ≈ 800, where the data abruptly changed.

Three simple low-level models were chosen to

Figure 1: Evolution of the output strip thickness deviation

h

2

[µm].

Table 1: Statistics of the prediction error.

Statistics \ Model averaging high-level

mean error 0.20 0.04

standard deviation 6.42 5.78

median 0.27 -0.06

approximate relations among selected process vari-

ables. They are characterized by the following regres-

sor structures:

M

(1)

: ψ = (v

r

, h

1

v

r

, 1)

′

,

M

(2)

: ψ = (h

1

, z, 1)

′

,

M

(3)

: ψ = (h

1

, z, v

r

, 1)

′

,

where v

r

denotes the ratio of the input and output strip

speeds, h

1

is the deviation of the input strip thick-

ness from its nominal value and z stands for the so

called uncompensated rolling gap. See (Ettler and

Andr´ysek, 2007) for details.

The initial setting was as follows: the low-

level models started with noninformative priornormal

inverse-gamma distributions (15). Forgetting factor

of the applied exponential forgetting (Peterka, 1981)

was set to 0.99. The averaging model started with

uniformlydistributed prior statistics a

(s)

0

, s = {1, 2, 3}.

The high-level model with the structure given in Sec-

tion 3.3 started with a noninformative prior pdf with

similar initial statistics as the low-level models. For-

getting factor was set to 0.98 in this case.

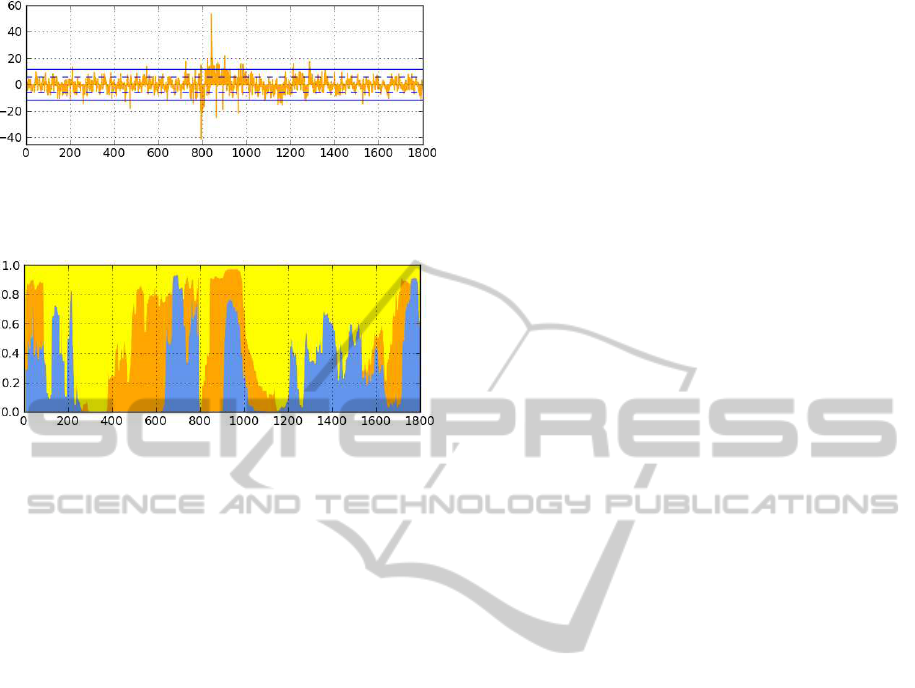

The evolution of probabilities of the averaged

models M

(s)

, s = {1, 2, 3} is depicted in Fig. 3. The

evolution of prediction error for h

2

is depicted in Fig.

2. Obviously, the announcedabrupt change in the data

course led to higher prediction errors. Statistics of the

prediction error stated in Tab. 1 demonstrate the role

of the high-level modelling.

5 CONCLUSIONS

A method of multilevel modelling was proposed to

improve instantaneous prediction of a key variable in

the process of cold strip rolling. The resulting hier-

archical model consist of three modelling levels – the

ICINCO 2011 - 8th International Conference on Informatics in Control, Automation and Robotics

288

Figure 2: Absolute prediction error [µm]: dashed and solid

line denote the distance of one and two standard deviations,

respectively.

Figure 3: Evolution of probabilities of models: M

(1)

(blue),

M

(2)

(orange) and M

(3)

(yellow).

low-level models, i.e., from the statistical viewpoint

usual parametric models, the averaging model merg-

ing their results and the high-level model, reflecting

specific needs of the application field. Each mod-

elling level is treated in the Bayesian framework, i.e.,

both the models and their parameters are represented

by conditional distributions. Current state of the re-

search was demonstrated on a simple example utiliz-

ing real industrial data. Extensive tests will be accom-

plished to refine the method and prepare algorithms

for a true on-line industrial application.

ACKNOWLEDGEMENTS

This research was supported by project M

ˇ

SMT

7D09008 (ProBaSensor) and project 1M0572 (DAR).

REFERENCES

Bernardo, J. and Smith, A. (2001). Bayesian Theory. Mea-

surement Science and Technology, 12:221.

Bohlin, T. (1991). Interactive System Identification:

Prospects and Pitfalls. Springer-Verlag, Berlin, Hei-

delberg, New York.

Dedecius, K. (2010). Partial Forgetting in Bayesian Es-

timation. PhD thesis, Czech Technical University in

Prague.

Ettler, P. and Andr´ysek, J. (2007). Mixing Models to Im-

prove Gauge Prediction for Cold Rolling Mills. In

Proceedings of the 12th IFAC Symposium on Automa-

tion in Mining, Mineral and Metal Processing, Que-

bec, Canada.

Geiger, D. and Heckerman, D. (1997). A Characterization

of the Dirichlet Distribution Through Global and Lo-

cal Parameter Independence. The Annals of Statistics,

25(3):1344–1369.

Gupta, A. and Nadarajah, S. (2004). Handbook of Beta Dis-

tribution and its Applications. CRC.

K´arn´y, M. (2006). Optimized Bayesian Dynamic Advising:

Theory and Algorithms. Springer-Verlag New York

Inc.

Karush, J. (1961). On the Chapman-Kolmogorov Equation.

The Annals of Mathematical Statistics, 32(4):1333–

1337.

Kulhav´y, R. and K´arn´y, M. (1984). Tracking of Slowly

Varying Parameters by Directional Forgetting. In 9th

IFAC World Congress, Budapest, Hungary.

Murphy, K. (2007). Conjugate Bayesian Analysis of the

Gaussian Distribution.

Peterka, V. (1981). Bayesian Approach to System Iden-

tification In P. Eykhoff (Ed.) Trends and Progress in

System Identification.

Raftery, A., K´arn´y, M., and Ettler, P. (2010). Online Pre-

diction Under Model Uncertainty via Dynamic Model

Averaging: Application to a Cold Rolling Mill. Tech-

nometrics: a journal of statistics for the physical,

chemical, and engineering sciences, 52(1):52.

Rudin, W. (2006). Real and complex analysis. Tata

McGraw-Hill.

ADAPTIVE CONTINUOUS HIERARCHICAL MODEL-BASED DECISION MAKING - For Process Modelling with

Realistic Requirements

289