THE EXPERTONS METHOD APPLIED IN THE

DIALOGUE WITH STAKEHOLDERS

Anna M. Gil Lafuente and Luciano Barcellos Paula

Faculty of Economics and Business. University of Barcelona, Av. Diagonal 690, 08034 – Barcelona, Spain

Keywords: Stakeholder Theory, Corporate Sustainability, GRI G3, Fuzzy Subsets, Expertons Method.

Abstract: According to numerous scientific studies one of the most important points in the area of sustainability in

business is related to dialogue with stakeholders. Based on the Theory of Stakeholder try to analyze

corporate sustainability and the process of elaboration a business report prepared in accordance with the

guidelines of the guide G3 - Global Reporting Initiative. With the completion of an empirical study seeks to

understand the expectations of stakeholders regarding the implementation of the contents of the

sustainability report. To achieve the proposed aim we use “The Expertons Method” algorithm that allows

the aggregation of opinions of various experts on the subject and represents an important extension of fuzzy

subsets for aggregation processes. At the end of our study, we present the results of using this algorithm, the

contributions and future research.

1 INTRODUCTION

The Stakeholder Theory postulates that a company's

ability to generate sustainable wealth over time and

thus its long-term value is determined by its

relations with its stakeholders (Freeman, 1984).

Donnelly, the stakeholder of a company is (by

definition) any group or individual who can affect or

is affected by the achievement of the objectives of

the organization. From Freeman, other authors

(Alkhafaji, 1989; Carroll, 1989; Brummer, 1991;

Clarkson, 1991; Goodpaster, 1991; Hill & Jones,

1992; Wood, 1991; Donaldson, T. and Preston, L.E.

1995; Mitchell, R.K., Agle, B.R. and Wood, D.J.,

1997; Post, J.E., Preston, L.E. and Sachs, S. 2002;

Rodríguez, M.A., Ricart, J.E. and Sánchez, P. 2002;

Aguilera, R.V. and Jackson, G. 2003; Hart, S.L. and

Sharma, S. 2004) have given primary emphasis on

the concept of the stakeholders. According to the

authors (Post, Preston and Sachs, 2002),

stakeholders of a firm are individuals and groups

who contribute voluntarily or involuntarily, to its

capacity and wealth creation activities and therefore,

are potential beneficiaries and / or risk bearers.

In the Stakeholder Theory (Olcese et al. 2008),

the enterprise is defined as a socioeconomic

organization formed to create wealth for the multiple

groups that compose it. The constructive

engagement of stakeholders (Elkington, J. 1998),

companies can increase external confidence in its

intentions and activities, helping to improve

corporate reputation and catalyze the diffusion of

more sustainable practices in the enterprise system

in general. In this new economy of stakeholders

(Olcese Santoja, 2009) we can speak of two types of

companies: traditional company and sustainable

company. Its characteristics can be differentiated as

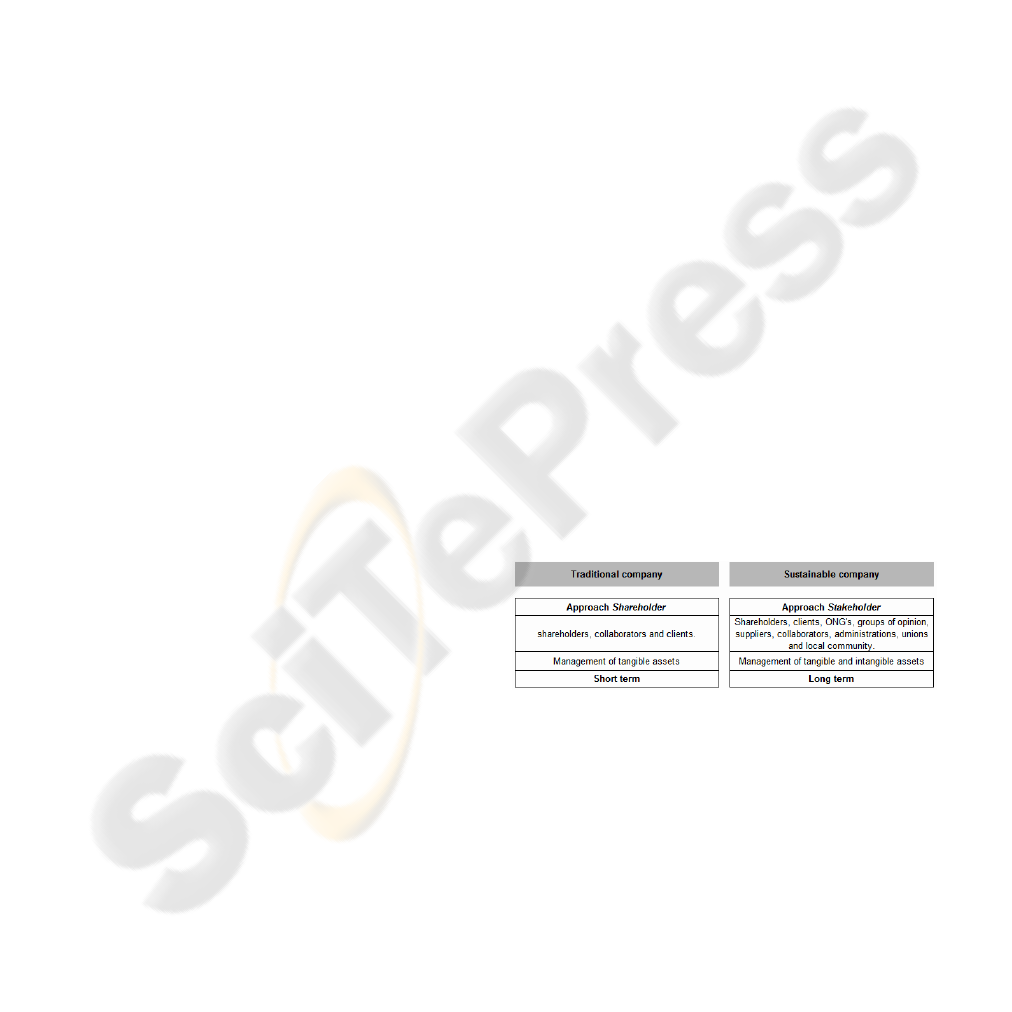

described in Figure 1.

Figure 1: Differences between traditional company and

sustainable company.

The traditional company has a shareholder-

oriented approach to three stakeholders

(shareholders, employees and customers). Its

orientation is based to enhance the physical assets of

the company and their expectations are short term.

The only aim of the company is to maximize profits

and respond to shareholders. Furthermore,

sustainable company has a stakeholder-oriented

approach towards all interest groups that take part in

the business (shareholders, employees, customers,

402

Gil-Lafuente A. and Barcellos Paula L. (2010).

THE EXPERTONS METHOD APPLIED IN THE DIALOGUE WITH STAKEHOLDERS.

In Proceedings of the 2nd International Conference on Computer Supported Education, pages 402-406

Copyright

c

SciTePress

NGOs, governments, unions, local community,

groups of opinion and suppliers). Its orientation is

based to enhance tangible and intangible assets of

the company as part of the value of the company and

its long-term expectations are. It's a new way of

managing the company (Carrión, J. 2009) in which it

must develop strategies and policies through internal

codes of conduct to ensure that the development of

its regular activities will be sustainable and not

impact against the social rights and environmental

interest groups involved, while, to be taken into

account in defining their business strategies.

According to the Sustainability Reporting

Guidelines, version 3.0, Global Reporting Initiative

(GRI, 2006) participatory processes of stakeholders

can serve as tools to understand the reasonable

expectations and interests of those. The GRI says

that “an organization may encounter conflicting

views or differing expectations among its

stakeholders, and will need to be able to explain how

it balanced these in reaching its reporting decisions.

Failure to identify and engage with stakeholders is

likely to result in reports that are not suitable, and

therefore not fully credible, to all stakeholders. In

contrast, systematic stakeholder engagement

enhances stakeholder receptivity and the usefulness

of the report. Executed properly, it is likely to result

in ongoing learning within the organization and by

external parties, as well as increase accountability to

a range of stakeholders. Accountability strengthens

trust between the reporting organization and its

stakeholders. Trust, in turn, fortifies report

credibility”.

Because of the complexity that is dialogue with

stakeholders, is crucial to address the analysis with

an approach based on complex systems and models

that help entrepreneurs in making decisions,

especially in an uncertain environment. For these

reasons, it is justified to analyze the dialogue with

stakeholders using algorithms such as "The

Expertons Method” (Kaufmann, A. and Gil Aluja, J.

(1993). This method represents an important

extension of fuzzy subsets whose idea and

development is due to A. Kaufmann (1987). To

authors (Gil Lafuente et al., 2007) “the advance that

the expertons method represent in relation with other

instruments of treatment of the uncertainty comes

given by the fact that it allows simultaneously a

good aggregation of the opinion of several experts

and that these express their opinions with the

freedom provided by the fuzzy numbers”. We stand

out some authors have used fuzzy logic applied to

the sustainability as (Gil Lafuente, A.M. et al., 2005,

2006) in the analysis of organic purchasing decisions

of consumers, (Barcellos Paula and Gil Lafuente,

2009a) in the selection of elements that contribute to

sustainable growth of the company, (LU LYY et al.,

2007) in the analysis of decision and evaluation of

"green" suppliers, and (Barcellos Paula; and Gil

Lafuente, 2009b) in algorithms applied in the

sustainable management of the human resources.

2 METHODOLOGY

Now, very briefly, how to build an Experton from

their properties. We know that everything has the

property Experton monotony Loose growing

horizontal, i.e., the characteristic function of

belonging of the function of positive slope is less

than or equal to the characteristic function of

belonging of the downward-sloping. And moreover

all vertical growing Experton has no strict

monotony, except in level 0 which always takes the

value 1. Therefore, we say:

21

:1,0 aa

in

21

,aa

(1)

´))()(´),()(´:1,0´,

2211

aaaa

(2)

1,1)()0(

21

aa

(3)

We consider the valuation of each expert

expresses a level of truth by scale of 11 values

between 0 and 1 both included that can be explained

generically as follows:

0:

false

0.1:

practically false

0.2:

almost false

0.3:

quite false

0.4:

more false than true

0.5:

neither true nor false

0.6:

more true tan false

0.7:

quite true

0.8:

almost true

0.9:

practically true

1:

true

From here will start a process of aggregation led

to the transformation of opinions in a representative

of the previous valuation. The first task will be to

obtain the statistics of the opinions to know the time

that experts have expressed the same opinion. From

the obtained cumulative frequency is the calculation

of the cumulative relative frequencies for the above

values by dividing the total number of views. The

result is called “Experton”. Its significance lies not

only in obtaining the relative frequencies assigned to

the characteristic function of belonging, but that the

information provided enables the distribution and

THE EXPERTONS METHOD APPLIED IN THE DIALOGUE WITH STAKEHOLDERS

403

the tendency of subjective opinions about whose

number can be very variable. The Experton is itself

an aggregate view representative of all that have

been considered in the sample. In order to give a

simplified representation of an Experton, can be

used to obtain the mathematical expectation. All

operators can be used with variable or confidence

intervals in [0,1] can also be used Experton, and

these operations are valid for any number of

Experton.

3 APPLICATION OF THE

EXPERTONS METHOD

Our study focuses on knowing the expectations of

stakeholders with respect to compliance with the

contents of the sustainability report prepared by a

company in accordance with the guidelines G3 -

Global Reporting Initiative. To achieve this

objective will try to analyze the sustainability of a

business catering sector through a survey conducted

in August 2009 by the Ideas and Solutions

Consulting in Brazil. At the request of the

contractor, the study data were treated with strict

confidentiality. Therefore, as suggested by the

Guidelines version 3.0, Global Reporting Initiative

(GRI), the company to develop its “Sustainability

Report” must be engaged in an extensive network of

experts from various interest groups among which

include business organizations, workers, NGOs,

investors and auditors, among others. The

consultancy contract was charged with gathering a

selection of interest groups, composed of 10 experts

on a panel to discuss Corporate Social

Responsibility issues that have been predefined. The

aim is to examine the basic content of the GRI,

which stands out among social performance, and

produce one or more outcomes, such as comments or

recommendations, which the company may or may

not establish specific commitments. Once submitted

to the 10 experts the contents of the Performance

Report on Social Sustainability, ask that you indicate

your view with the scale [0,1], whereby, as the

closer estimate 1, the better the meeting the

expectations of stakeholders in the following items:

1- Labor practices and decent work

2- Human rights

3- Society

4- Product responsibility

4 RESULTS

The approach that follows is based on the

consideration of elements and data emerging from a

real demand. The results may allow for deep

reflection and application to academic and

professional fields.

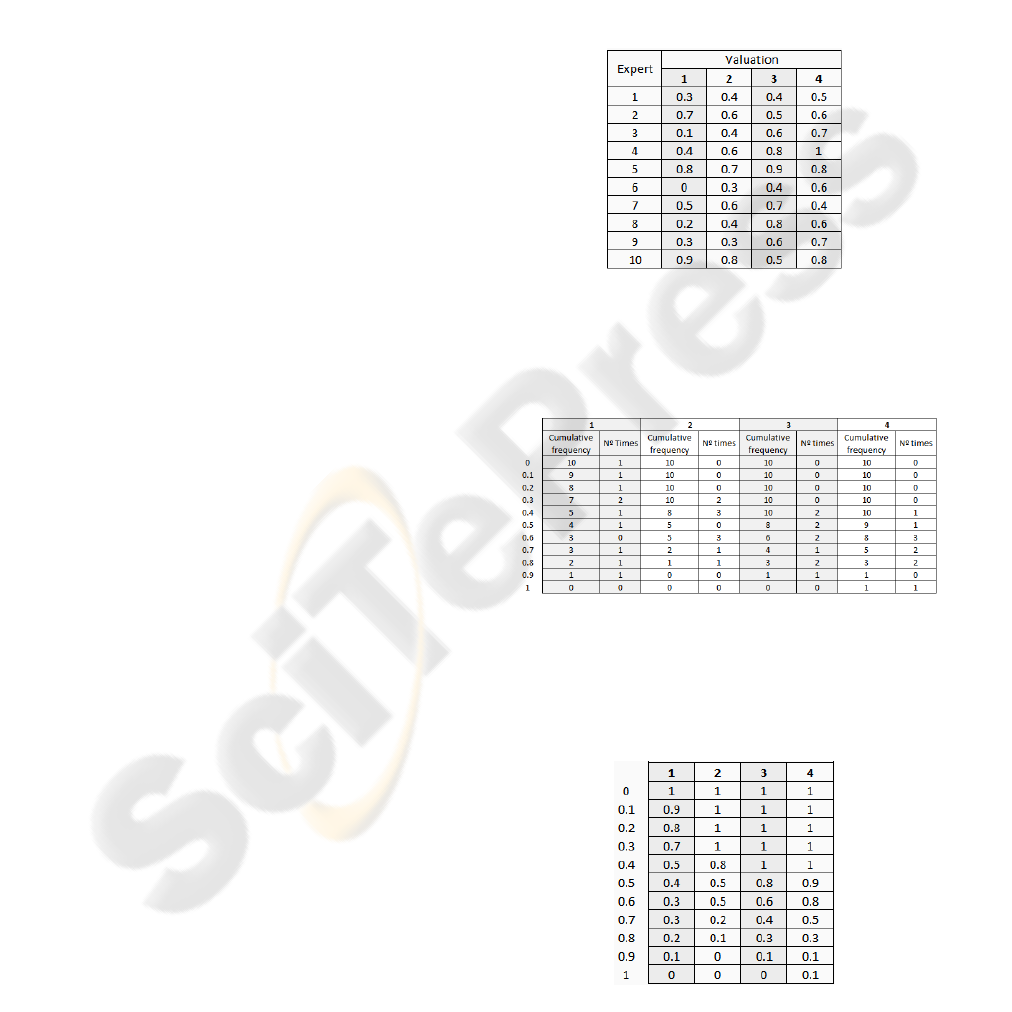

According to data collected by the consultant

would have the views of 10 experts, as shown in

Table 1.

Table 1: Views of 10 experts.

The first task will be to obtain the statistics of the

opinions to know the time that experts have

expressed the same valuation (Table 2).

Table 2: Cumulative Frequency.

From the obtained cumulative frequency is the

calculation of cumulative relative frequencies (Table

3) dividing the above values by the total number of

views, in our case 10.

Table 3: Cumulative relative frequencies.

CSEDU 2010 - 2nd International Conference on Computer Supported Education

404

The result is called "Experton. The Experton is

itself an aggregate view representative of all that

have been considered in the sample. In order to give

a simplified representation of an Experton, can be

used to obtain the expected value (Table 4).

Table 4: Expected value.

The result identifies the expectations of

stakeholders about the content of the sustainability

report related to corporate social performance

through the aggregation of views. In this case, we

observe a very large distance between the

expectations of stakeholders with the draft

sustainability report being prepared by the company.

Therefore, the company needs to devote special

attention to the contents related to “labor practices

and decent work” and “human rights" valuation

receiving 0.4 and 0.5 respectively. The items

"society" and "product responsibility" valuation

were 0.6 and 0.7 respectively. The proposed model

can be extended in accordance with the requirements

of questions and the number of participating experts

and business sectors.

5 CONCLUSIONS

The study on corporate sustainability shows that

compared with the changes we are living is essential

to find models that will help employers in making

decisions, especially in an uncertain environment.

Because of the complexity that is the search for

more sustainable development through dialogue with

stakeholders in our research we try to analyze these

complex systems using fuzzy logic. In implementing

the proposed model, we provide a tool based on the

use of “Method of Experton”. This methodology can

facilitate decision making by obtaining qualitative

data from a dialogue with various stakeholders. This

is an innovation and a useful tool to be used in the

processes of aggregation and unification of views or

differing expectations among its stakeholders. The

model also allows to know the distribution function

at levels characteristic of belonging to the aggregate

values. The result show that has provided us with the

expectations of stakeholders regarding the

implementation of the contents of the sustainability

report. Now the company must revise their

commitments and related management approach

social issues, such as “labor practices and decent

work” and “human rights".

The main contribution of this paper is to provide

a model that assist entrepreneurs in the aggregation

of opinions related to the stakeholders. At the same

time, as the GRI G3, the company serves as

documentation and explanation of how it has

evaluated such factors when drafting the report. We

believe that our contribution will serve to support

future research in the field of sustainability in

business and the application of the methodology in

dialogue with stakeholders.

ACKNOWLEDGEMENTS

Luciano Barcellos de Paula is as a scholar of

MAEC-AECI.

REFERENCES

Aguilera, R.V., Jackson, G., 2003. The Cross-National

Diversity of Corporate Governance: Dimensions and

Determinants. The Academy of Management Review,

28(3), 447-465.

Alkhafaji, A.F., 1989. A stakeholder approach to corporate

governance: Managing in a dynamic environment.

New York: Quorum Books.

Barcellos Paula, L., Gil Lafuente, A.M., 2009a. Proceso de

selección de elementos que contribuyen al crecimiento

sostenible de la empresa. Proceeding of International

Conference and Doctoral Consortium for ISEOR and

Academy of Management, held at Lyon, France, (1),

773-788.

Barcellos Paula, L., Gil Lafuente, A.M., 2009b.

Algoritmos aplicados en la gestión sostenible de los

recursos humanos. Economic and Financial

Crisis:”New challenges and Perspectives”. Proceeding

of XV Congress of International Association for

Fuzzy-Set Management and Economy (SIGEF), Lugo,

Spain.

Brummer, J.J., 1991. Corporate responsibility and

legitimacy: An interdisciplinary analysis. New York:

Greenwood Press.

Carrión, J., 2009. Responsabilidad Social Corporativa.

Observatory on Debt in Globalization. Sustainability

Portal. UNESCO Chair of Sustainability at UPC.

Barcelona.

Carroll, A.B., Buchholtz, A.K., 1989. Business and

Society: Ethics and Stakeholder Management.

Southwestern Publishing Co., Cincinnati.

Clarkson, M.B.E., 1991. Defining, evaluating, and

managing corporate social performance: A stakeholder

management model. In J. E. Post (Ed.), Research in

corporate social performance and policy (pp. 331-

358). Greenwich, CT: JAI Press.

THE EXPERTONS METHOD APPLIED IN THE DIALOGUE WITH STAKEHOLDERS

405

Donaldson, T., Preston, L. E., 1995. The Stakeholder

Theory of the Corporation: Concepts, Evidence and

Implications. Academy Management Review, 20(1),

65-91.

Elkington, J., 1998. Cannibals with forks: the triple

bottom line of 21st Century Business. Oxford, U.K.

Capstone Publishing Limited.

Freeman, R.E., 1984. Strategic Management: A

Stakeholder Approach. Pitman Series in Business and

Public Policy.

Gil Lafuente, A. M et al., 2007. Modelos y Algoritmos

para el tratamiento de la creatividad en la gestión

empresarial. Editorial Milladoiro (pp.47-91).

Gil Lafuente, A.M. et al., 2005. Models for analysing

purchase decision in consumers of ecologic products.

Fuzzy Economic Review, X, 47-62.

Gil Lafuente, A.M., Salgado Beltrán, L., Subirá Lobera,

E., Beltrán, L.F., 2006. Teoría de efectos olvidados en

el consumo sustentable de productos ecológicos. In

Desarrollo sustentable: ¿Mito o realidad? (pp. 223-

240). Ed. Centro de investigaciones biológicas del

noroeste, S.C. Mexico.

Global Reporting Initiative, 2006. Sustainability Reporting

Guidelines, version 3.0.

Goodpaster, K.E., 1991. Business ethics and stakeholder

analysis. Business Ethics Quarterly, 1(1), 53-73.

Hart, S.L., Sharma, S., 2004. Engaging Fringe

Stakeholders for Competitive Imagination. Academy

of Management Executive, 18(1).

Hill, C.W.L., Jones, T.M., 1992. Stakeholder-Agency

Theory. Journal of Management Studies, 29, 131-154.

Kaufmann, A., 1987. Les expertones. Ed. Hermés. París.

Kaufmann, A., Gil Aluja, J., 1993. Técnicas especiales

para la gestión de expertos. Milladoiro, Santiago de

Compostela (pp. 89-118).

Lu Lyy, Wu Ch, Kuo Tc., 2007. Environmental principles

applicable to green supplier evaluation by using multi-

objective decision analysis. International Journal of

Production Research, 45(18-19), 4317-4331.

Mitchell, R.K., Agle, B.R., Wood, D.J., 1997. Toward a

Theory of Stakeholder Identification and Salience:

Defining the Principle of who and what really Counts.

The Academy of Management Review, 22(4), 853-886.

Olcese Santoja, A., 2009. La Responsabilidad Social y el

Buen Gobierno en la empresa, desde la Perspectiva

del Consejo de Administración. Thesis Directors: Dr.

Prosper Lamothe and Dr. John Mascarenas.

Universidad Autonoma de Madrid and Universidad

Complutense de Madrid. Faculties of Economics and

Business.

Olcese, A., Rodríguez Ángel, M., Alfaro, J., 2008. Manual

de la empresa Responsable y Sostenible. Madrid:

McGraw-Hill.

Post, J.E., Preston, L.E., Sachs, S., 2002. Managing the

Extended Enterprise: The New Stakeholder View.

California Management Review, 45(1), 5-28.

Rodríguez, M.A., Ricart, J.E., Sánchez, P., 2002.

Sustainable Development and the Sustainability of

Competitive Advantage: A Dynamic and Sustainable

View of the firm. Creativity and Innovation

Management, 11.

Wood, D. J., 1991. Social issues in management: Theory

and research in corporate social performance. Journal

of Management, 17, 383-405.

CSEDU 2010 - 2nd International Conference on Computer Supported Education

406