EMPIRICAL STUDY OF ERP SYSTEMS IMPLEMENTATION

COSTS IN SWISS SMES

Catherine Equey

1

, Rob J. Kusters

2

, Sacha Varone

1

and Nicolas Montandon

1

1

Haute Ecole de Gestion, 1227 Carouge, Switzerland;

2

University of Technology and Open University, The Netherlands

Keywords: ERP implementation; cost drivers; Swiss SMEs.

Abstract: Based on the sparse literature investigating the cost of ERP systems implementation, our research uses data

from a survey of Swiss SMEs having implemented ERP in order to test cost drivers. The main innovation is

the proposition of an additional classification of cost drivers that focuses on the enterprise itself, rather than

on ERP. Particular attention is given to consulting fees as a major factor of implementation cost and a new

major cost driver has come to light. “Consultant experience”, not previously mentioned as such in literature,

appears as an important aspect of ERP implementation cost. Particular attention must be paid to this factor

by the ERP implementation project manager.

1 INTRODUCTION

One of the main questions asked by management in

charge of an Enterprise Resource Planning (ERP)

project is “How much does it cost”? It is very

difficult to provide a direct answer to this question

and academic literature prefers to investigate cost

drivers (Kusters, Heemstra and Jonker, 2007); while

remaining otherwise scarce on the matter of the level

of cost. The aim of this research is to examine

factors of implementation cost and specifically the

research question “which factors substantially

influence ERP implementation cost?”

The issue of factors that impact ERP

implementation cost is discussed explicitly by

Stensrud (2001). In his research, he wondered if the

existing body of knowledge developed for software

cost estimation was applicable to estimation of ERP

implementation effort.

Several software cost estimation approaches

exist, such as the constructive cost model

(COCOMO) developed by Boehm (1983). The

approach states that under normal circumstances

development costs are a function of project size.

Since the circumstances in which a project takes

place are rarely ‘normal’, the estimate must be

refined using additional cost drivers. As an example,

one of the models proposed by Boehm is as follows:

Development costs =(a *cd[size]

b

)

* cd

1

* cd

2

…* cd

14

(where cd means cost driver)

(1)

The cost driver ‘size’ (cd[size]) is viewed as the

most dominant cost driver, not only in COCOMO

but also in many other models (Kusters,

Van Genuchten and Heemstra, 1990).

Stensrud (2001) concluded that since most

software cost estimation (SCE) approaches are based

upon the use of the number of lines of source code

(Boehm, 1983) or some synthetic variable such as

function points (Albrecht and Gaffney, 1983) to

assess the size of the project, these approaches are

not immediately applicable. An ERP implementation

project may contain some software development, but

will also contain substantial modelling, installation

and reorganization efforts. It seems unlikely that a

one-dimensional measure of software size will

capture this complexity. He did however conclude,

that a measure of size for an ERP implementation

project would likely be multi-dimensional; using a

combination of measures such as the number of

users, the number of reports that have to be

designed, and the number of ERP modules.

Stensrud (2001) further concludes, based on a

screening of existing SCE tools, that the concepts

provided by parametric models such as COCOMO II

(“COCOMO II”, 1998) provide a good starting point

for the development of an estimation model. Crucial

elements in these models are the existence of a size

metric that can be used to estimate ‘normal’ costs, as

well as cost drivers that can adjust for project

specific issues. He also concluded that emergent

143

Equey C., J. Kusters R., Varone S. and Montandon N. (2008).

EMPIRICAL STUDY OF ERP SYSTEMS IMPLEMENTATION COSTS IN SWISS SMES.

In Proceedings of the Tenth International Conference on Enterprise Information Systems - DISI, pages 143-148

DOI: 10.5220/0001683601430148

Copyright

c

SciTePress

models for estimation of implementation effort of

standard software, in particular the COCOTS model

(“COCOTS”, 2001), may provide valuable support

in this area. Empirical works by Francalanci (2001),

Von Arb (2001), and Kusters et al. (2007) support

this line of reasoning.

The research by Francalanci (2001) is focused on

the identification of a usable measure of size. In

agreement with Stensrud (2001), she deduces that

such a measure should be multi-dimensional. Based

on data from 43 SAP R/3 implementation projects in

a number of European companies, she identifies

three constituting elements for such a size metric:

• Size of the organization: The size of an

organization reflects its inertia, its ability to resist

change. The assumption is that the larger and

more cumbersome an organization, and in

consequence the more inert it is, the more an

implementation effort will cost. As measures of

organizational size she tested the number of

employees and revenue. Both were found to be

useful.

• Size of the configuration: The size of the

configuration effort is expressed in the number

of modules or sub-modules that are to be

implemented. The assumption is that effort will

increase with the number of modules to be

implemented.

• Size of the implementation: Implementation

effort is expressed by the number of users

involved, since these indicate training and

reorganization effort.

Like Francalanci (2001), Von Arb (1997) focuses

solely on size. In his research, a multi-dimensional

measure based on number of users and number of

(sub-) modules is identified. These results are fairly

similar to Francalanci’s, but do not look at

organizational size.

Kusters et al. (2007) looked at both size and at

additional cost drivers in an in depth investigation

into two companies. The notion that size is

multidimensional was supported in both

organisations, but the composing metrics were

different. It appeared, as exposed in Table 1, that

size was perceived as a combination of:

a) A measure related to the amount of work that is

involved in configuring the ERP system. For this

measure, items such as the number and

complexity of transactions, interfaces, reports

and the amount of data and data conversion were

mentioned. In practice, people perceive “size”

related to the configuration effort at a more

detailed level (e.g. number of interfaces) than do

both Francalanci and Von Arb, who look at the

rather coarse measure number of modules.

b) A measure indicating system implementation and

business reorganisation costs. Francalanci (2001)

refers to this as implementation size. As this

“size” increases, more staff needs to be trained

and also more people are involved in

organisational change efforts. This measure

includes items such as number of users, number

of user groups.

c) Francalanci’s ‘size of the organisation’ was also

referred to explicitly, but notions of number of

user groups’ or number of departments could be

construed as such.

It is unclear how to consider the cost driver number

and complexity of business processes mentioned by

Organization II. Complex business processes almost

certainly have an impact on the configuration effort.

Process modelling is a standard part of ERP

implementation preparation and a large number of

process model metrics are already available (see for

example Netjes, Limam Mansar, Reijers, and Van

der Aalst, 2007).

Table 1: Results on size related cost drivers.

There seems to be consensus in available literature

on the usefulness of a multi-dimensional size related

cost driver. There is also some agreement as to the

dimensions involved, but definitely more research is

required into the metrics to be used for each

dimension.

The ‘configuration effort’ dimension is

mentioned by all three references. Francalanci

(2001) and Von Arb (1997) used number of (sub)

modules as a metric, but Kusters et al (2007)

rejected this notion and proposed more detailed

metrics.

Francalanci; Kusters et al:

Von Arb Organization I Organization II

- № of (sub)

modules

- size of

organization

- № of users

- № of

transactions,

- № of

interfaces,

- № of reports

- amount data

conversion

- № of user

groups

- № of users

- № and complexity

of transactions

- № and complexity

of interfaces

- № and complexity

of reports

- size and

complexity of data

- № of departments

- № of users

- № and complexity

of business

processes

ICEIS 2008 - International Conference on Enterprise Information Systems

144

‘Implementation effort’ is also an accepted

dimension. The metric most mentioned is number of

users. However, not just training and motivation

effort are important. The degree of reorganisation

required can be expected to play a role. This is

confirmed by Kusters et al (2007), where cost

drivers such as fit between organization and

product, process maturity and insight in the

processes were mentioned as additional cost drivers.

This leads to a test of an additional metric: degree of

BPR.

Organisational size or ‘planning effort’ is the

third dimension that was previously mentioned.

Apart from the size related factors discussed

above, people related factors are most likely to

impact ERP implementation costs (see Boehm,

1983, and Kusters et al, 1990, for general arguments

to this effect; and Kusters et al, 2007, for ERP

specific results).

Given the availability of data from a study of

Swiss SMEs in 2006 (Equey, 2006), it is interesting

to take a closer look at the dimensions involved. The

aim is to substantiate these three efforts on the basis

of this specific population. As far as we know, this is

the only existing empirical study based on a broad

based survey of Swiss SMEs.

This section focuses on existing literature. In

Section 2, we present the sampling strategy of our

survey of Swiss SMEs. Section 3 presents

descriptive statistics of our data followed by a

correlation analysis. In conclusion, we point out the

main findings, the limitations of this study as well as

directions for future research.

2 METHODOLOGY

The statistical evidence for this study was collected

on the basis of a written survey. The first phase of

the research consisted of in-depth interviews of

Swiss companies from the French speaking part of

the country. This multiple case study (Equey & Rey,

2004) revealed a number of research questions and

associated hypotheses that lead to the design of the

questionnaire. The questionnaire was conceived with

the participation of senior consultants from the four

major vendors of ERP solutions for SMEs on the

Swiss market (Abacus, Microsoft, Oracle and SAP).

The final version of the survey was broken down as

follows: contact details, activities and financial

information about the company, specificities of

implemented ERP, description of the

implementation process, project organization,

outcome and benefits derived from the use of the

ERP system, difficulties and problems encountered.

The main purpose of the survey was to determine

the extent to which Swiss SMEs were aware of or

have implemented ERP. The questionnaire covered a

wide range of topics including implementation and

organisational factors but also issues such as user

satisfaction, the tools used and the perceived value-

added. In the present paper we focus only on the

data pertaining to costs.

More than 4’000 Swiss SMEs were contacted

over a six-month period between November 2005

and April 2006 to take part in the nation-wide

survey. The questionnaire was written in French,

German, Italian and English and was distributed by

post. An electronic version was also made available.

The French version is included in (Equey, 2006).

Other versions are available from the authors.

Contact details for SMEs were obtained from the

Swiss federal office of statistics (OFS) and a sample

was constructed according to the following three

criteria: the size of the company in terms of the

number of employees, the sector of activity

(secondary/ tertiary) and the linguistic region.

In order to be demographically representative,

75% of the sample was chosen from the German-

speaking region of Switzerland, 20% from the

French-speaking region and the remaining 5% from

the Italian-speaking region. In addition, 84% of the

companies surveyed employed from 1 to 49 persons

and the remaining 16% employed between 50 and

249 persons.

To obtain the relatively high response rate of

17.2%, the mailing was followed up by a telephone

interview. A total of 687 Swiss SMEs responded to

the questionnaire. Of those, 18.2% indicated the use

of an ERP, whereas 81.5% or 560 declared not using

an ERP. These results show a relatively low level of

penetration in Swiss SMEs (less than 20%).

3 RESULTS AND DISCUSSION

3.1 Descriptive Statistics

This paper uses the data from the survey in Equey

(2006) and in particular, the sub set of 125

respondent ERP users who had completed the

detailed questionnaire. The inquiry revealed certain

trends that are summarized below.

The respondents indicated a project timeframe of

less than one year in 80% of cases and even less than

six months for 53%. These projects generally

involve less than 7% of the company’s internal staff

EMPIRICAL STUDY OF ERP SYSTEMS IMPLEMENTATION COSTS IN SWISS SMES

145

and financially represent no more than 1% of annual

revenue in 35% of cases (cf. Table 2). A further 38%

fall within 1% and 3% of annual revenue. On

average, 4 modules are implemented in these

projects. Unsurprisingly, the finance module is used

in over 80% of cases and the other most frequently

utilized modules: Purchasing, HR, Inventory

management and CRM appear in over 50% of

responses. On the other hand, the production

module is used by fewer than 40% of respondents,

highlighting the preponderance of tertiary sector

enterprises in our sample.

The data reveals in most cases a ratio of one

(external) consultant employed to each staff member

committed to the project. The cost of consulting was

under 20% of the total project cost in 57% of cases

with a further 20% falling within 50% of total cost

(cf. Table 4b). Consulting cost is clearly the main

individual factor of total cost of implementation in

ERP projects.

Software user licenses represent roughly 15% of

total project cost in 54% of cases (cf. Table 4c) and

the ongoing commitment to maintenance is on

average less than 0.5% of the company’s annual

turnover (cf. Table 3). Half of the companies

revealed that the number of end users of the system

was less than 10 and a further 44% had between 10

and 100 end users.

The overall costs of the projects covered by this

survey (Equey, 2006) are shown in Table 2. The

results are somewhat surprising since

implementation and maintenance costs were

expected to be higher. Table 3 lays out the average

ongoing costs of the systems implemented and

Tables 4a, 4b and 4c show a breakdown of the

implementation costs.

Table 2: Total cost of implementation of an ERP.

Total cost in % of revenue % of companies

Less than 1% 35%

Between 1 and 3% 38%

Between 3 and 5% 14 %

Between 5 and 7% 2%

Greater than 7% 2%

Did not respond 9%

Table 3: Ongoing costs of an ERP.

% of annual revenue Outsourcing

% in category

Maintenance

% in category

Less than 0.5% 67% 64%

Between 0.5 and 1% 7% 21%

Greater than 1% 5% 5%

Did not respond 21% 10%

Table 4a: Investment in IT during ERP implementation.

% of total cost % of respondents

Less than 5% 28%

Between 6 and 10% 20%

Between 10 and 20% 26%

Greater than 20% 17%

Did not respond 19%

Table 4b: Consulting costs as a percent of total costs.

% of total cost % in each category

Less than 20% 57%

Between 20 and 50% 20%

Between 50 and 70% 8%

Greater than 70% 6%

Did not respond 19%

Table 4c: User licenses as a percent of total cost.

% of total cost % in each category

Less than 10% 34%

Between 10 and 15% 20%

Between 15 and 20% 11%

Greater than 20% 24%

Did not respond 11%

These findings are interesting in their own right

but give no information about the cost drivers

involved.

3.2 Correlation Analysis

In this research, we mainly look at factors that

substantially influence ERP implementation costs.

Some of the variables poorly fit existing

classifications but are significant in terms of their

impact; one example is Consultant’s level of

experience. We therefore propose an additional

classification that seems more appropriate within the

context of our variables.

The variables are classified into three groups:

enterprise characteristics, people and

implementation. This classification focuses on the

enterprise, rather than on the ERP itself, as

previously proposed by Kusters et al (2007) and

Francalanci (2001), to assist in the decision making

process of enterprises for its cost calculations.

To ascertain if a relationship exists between the

cost of an ERP project and a variable, we use a

measure of correlation r, which indicates if a linear

relationship exists between variables. We also

calculate the probability (the p-value) that such

relationship exists by chance only. As a standard,

relationships having a p-value of less than 5% are

ICEIS 2008 - International Conference on Enterprise Information Systems

146

deemed to be present by chance only and are thus

rejected.

Enterprise Characteristics. The cost of an ERP

project has been found to be dependent upon annual

sales revenue r = -0.167, p (one-tailed) = 0.44 as

well as the fact that the enterprise is a subsidiary of a

foreign holding r = -0.244, p = 0.01. The negative

correlation indicates that the increase/decrease of

one variable corresponds to the opposite for the

other variable. This is normal since the cost has been

coded as a percentage of the annual sales and

therefore, once a limit has been reached in the

amount of money for an ERP system, the percentage

of annual sales for the cost decreases. There is also

a strong correlation between annual sales and the

fact that the enterprise is a subsidiary of a foreign

holding r = -0.321, p = 0.01. Therefore, the cost of

ERP is found to be lower for these subsidiaries.

Those two variables can be considered as a (single)

factor for which a relationship exists with the cost.

No evidence of a relationship has been detected

between the cost of an ERP project and the number

of ERP users, the number of employees or the sector

of activity. Prevailing assumptions about “ERP

users” cannot be validated with our data.

People. The cost of an ERP project has been found

to be dependent upon the management's involvement

r = 0.182, p = 0.029; the ERP consultant's level of

experience r = -0.241 p = 0.006; the employee's

involvement r = 0.171 p = 0.033; the ratio of

external consultant by internal employee r = 0.172,

p = 0.038. It is interesting to note that even if the

cost of an experienced consultant is high; his

experience will probably decrease the duration of

ERP implementation and subsequently the total cost

of the project. The involvement of employees in the

ERP project increases the cost, but this involvement

may probably be considered as a way to facilitate the

adoption of a new system.

No evidence of a relationship has been detected

between the cost of an ERP project and the

employees' qualifications or field of expertise, nor

with the project manager's position.

Implementation. The cost of an ERP project is

found to be dependent upon the number of modules

to be implemented r = 0.186, p = 0.022; Pearson’s

correlation coefficient indicates a positive

relationship between those variables. This justifies,

in support of literature, the a priori intuition that as

the number of implemented modules increases, so

does the cost of an ERP project. There is a less than

3 percent chance that a correlation coefficient this

large would exist by chance only.

The cost of an ERP project is also dependent

upon the type of module(s) implemented. Indeed,

some of the modules are found to be positively

correlated to the cost of an ERP project, since their

significance values are no more than 0.05. There is a

medium intensity of the relation between those

modules and the cost of an ERP project

(cf. Table 5).

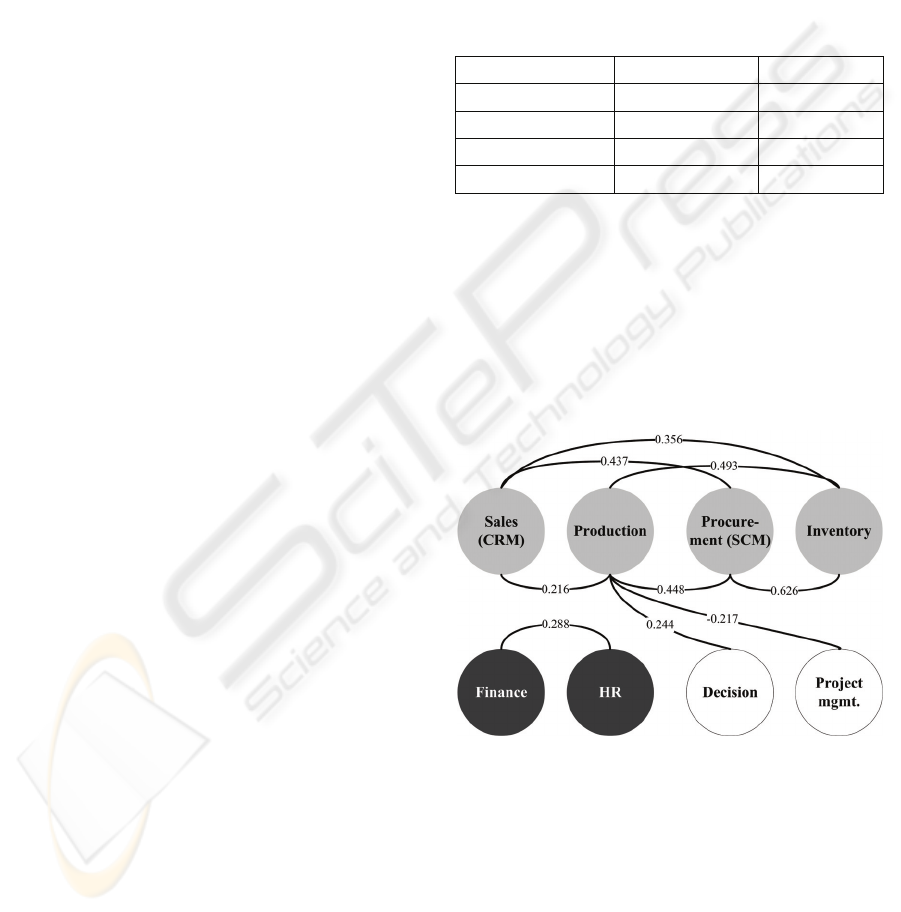

Table 5: Correlation to cost of ERP project.

ERP modules are shown to be related with a factor

analysis. Two main factors have been detected: a

first one includes the procurement (SCM) module,

the production module, the sales /CRM module and

the inventory module; a second one includes the

finance module and the human resource module.

The relationship between modules can be

summarized as follows, where only significant

correlations are shown.

Figure 1: Correlation between modules.

On the other hand, the results show no strong

evidence of a relationship between the cost of an

ERP project and the other types of modules

individually (i.e. finance, human resources, decision

making, project management...). Moreover, no

evidence of a relationship has been found with

organization tool used or the ERP architecture (web

server or client).

Module r p

Procurement (SCM) 0.260 0.005

Production 0.220 0.017

Sales / CRM 0.274 0.003

Inventory 0.186 0.045

EMPIRICAL STUDY OF ERP SYSTEMS IMPLEMENTATION COSTS IN SWISS SMES

147

4 CONCLUSIONS

This research paper points to some of the factors that

may influence the cost of an ERP project. An

additional classification of these cost drivers has

been introduced that is focused on the enterprise,

rather than on ERP.

An important cost driver mentioned in the

literature is clearly validated by our analysis: the

cost of on ERP project is dependent on the number

of modules to be implemented. On the other hand,

the interdependence of the number of ERP users and

the ERP project cost could not be established with

enough reliability through our data. A usual belief is

that the cost of the user licenses is a central factor of

cost. Nevertheless, our analysis has not revealed

evidence of such a relationship. Project managers

often, counter productively, “over focus” here to try

to generate savings.

The importance of the factor consulting cost

clearly stands out in the data and our analysis reveals

a new major cost driver, not discussed as such in

literature, relating to consultant experience. That

people characteristics would impact project costs is

not a surprise in itself. However, that this impact is

so important, that it ranks with size and can be

identified by such a correlation analysis is certainly

surprising. Consulting is implicit to other cost

drivers such as the number of interfaces or reports

and thus deserves investigation. It is interesting to

point out the negative correlation found between

consultants’ experience in ERP and total cost. This

result implies managerial and practical consequences

concerning the choice of consultants.

As empirical research attempts to measure

business perceptions, some limitations or biases are

unavoidable. Consequently, as is always the case in

empirical research, results should be interpreted with

some caution. The extrapolation of these results to

large companies is not appropriate, and future

research should, therefore, be conducted for them.

Further research to construct a multiple regression

model will be a next step, in order that managers

may evaluate ERP implementation project cost

based on enterprise characteristics.

REFERENCES

Albrecht, A.J., & Gaffney, J.E. (1983). Software Function,

Source Lines of Code, and Development Effort

Prediction, IEEE Tr. on Software Engineering, SE-

9(6).

Arb, R. von (1997). Vorgehensweisen und Erfahrungen

bei der Einführung von Enterprise-Management-

Systemen, PhD. Dissertation Universität Bern,

Switzerland.

Boehm, B.W. (1983). Software Engineering Economics,

Prentice Hall.

COCOMO II, Model Definition Manual (1998).

http://sunset.usc.edu/csse/research/COCOMOII/cocom

o_main.html (Retrieved 20.11.2007).

COCOTS Model Description, (2001).

http://sunset.usc.edu/research/COCOTS/index.html

(Retrieved 21.11.2007).

Equey, C., & Rey, A. (2004). La mise en place d’une

solution de gestion moderne (ERP/PGI), quels enjeux

pour une PME/PMI ? 1ère partie : étude de cas

détaillés, Working paper N°HES-SO/HEG-GE/C--

06/1/4--CH

Equey, C. (2006). Étude du comportement des PME/PMI

suisses en matière d’adoption de système de gestion

intégré, Working paper N°HES-SO/HEG-GE/C--

06/12/1--CH

Francalanci, C. (2001). Predicting the Implementation

Effort on ERP projects, Journal of Information

Technology, 16(1), 33-48.

Kusters, R.J., HeemstraF.J., & Jonker, A. (2007).

Determining the costs of ERP implementation,

Proceedings of the 9

th

International Conference on

Enterprise Information Systems, Vol. Database and

Information Systems Integration, 102-110.

Kusters, R.J., Van Genuchten, M., & Heemstra, F.J.

(1990). Are software cost estimation models accurate?

Information and Software technology, 32 (3), 187-190.

Netjes, M., Limam Mansar, S., Reijers, H.A., & Aalst,

W.M.P. van der (2007). An evolutionary approach for

business process design: towards an intelligent system,

Proceedings of the 9

th

International Conference on

Enterprise Information Systems, Vol. Information

Systems Analysis and Specification, 47-54.

Stensrud, E. (2001). Alternative Approaches to Effort

Prediction of ERP Projects, Information and Software

Technology, 43, 413-423.

ICEIS 2008 - International Conference on Enterprise Information Systems

148