CHANGE-POINT DETECTION WITH SUPERVISED LEARNING

AND FEATURE SELECTION

Victor Eruhimov, Vladimir Martyanov, Eugene Tuv

Intel, Analysis and Control Technology, Chandler, AZ, U.S.A.

George C. Runger

Industrial Engineering, Arizona State University, Tempe, AZ, U.S.A.

Keywords:

Data streams, ensembles, variable importance, multivariate control.

Abstract:

Data streams with high dimensions are more and more common as data sets become wider. Time segments

of stable system performance are often interrupted with change events. The change-point problem is to detect

such changes and identify attributes that contribute to the change. Existing methods focus on detecting a

single (or few) change-point in a univariate (or low-dimensional) process. We consider the important high-

dimensional multivariate case with multiple change-points and without an assumed distribution. The problem

is transformed to a supervised learning problem with time as the output response and the process variables as

inputs. This opens the problem to a wide set of supervised learning tools. Feature selection methods are used

to identify the subset of variables that change. An illustrative example illustrates the method in an important

type of application.

1 INTRODUCTION

Data streams with high dimensions are more and

more common as data sets become wider (with more

measured attributes). A canonical example are nu-

merous sensors (dozens to hundreds) with measure-

ments generated from each over time. Many charac-

teristics can be of interest from a system that gener-

ates such data, but one systemic question is whether

the system has been stable over a time period, or

whether one of more changes occurred. In a change-

point problem, historical data from streams is re-

viewed retrospectively over a specified time period to

identify a potential change, as well as the time of the

change. This historical analysis differs from real-time

monitoring where the goal is to detect a change as

soon as it occurs.

Change points are of interest in areas as diverse

as marketing, economics, medicine, biology, mete-

orology, and even geology (where the data streams

represent data over depths rather than over time). In

medicine, a change-point model can be used to detect

whether the application of a stimulus affects the re-

action of individual neurons (Belisle et al., 1998). In

the study of earthquakes, it is of interest to distinguish

one seismicity from another (Pievatolo and Rotondi,

2000).

Modern data streams often must handle high di-

mensions. A common approach is to use a multi-

variate control chart for process monitoring such as

Hotelling’s T

2

control chart (Hotelling, 1947). This

is a widely-used multivariate control chart to moni-

tor the mean vector of a process based on the Ma-

halanobis distance of the current data vector from a

historical mean data vector. The distance measure

used in T

2

incorporates the correlations among the

attributes that are measured. However, because this

distance measure is fundamentally based on a sum of

squared deviations of the elements of the current vec-

tor, it loses sensitivity to change points that occur in

only one or a few attributes among many (and result

in small changes in Mahalanobis distance). More sen-

sitive extensions were developed for real-time moni-

toring such as a multivariate exponentially weighted

moving average control charts (MEWMA) (Lowry et

al. 1992), and a multivariate cumulative sum control

charts (MCUSUM) (Runger and Testik 2004). These

extensions are still based on sums of squares with the

previously mentioned, intrinsic limitations as the di-

mension increases.

359

Eruhimov V., Martyanov V., Tuv E. and C. Runger G. (2007).

CHANGE-POINT DETECTION WITH SUPERVISED LEARNING AND FEATURE SELECTION.

In Proceedings of the Fourth International Conference on Informatics in Control, Automation and Robotics, pages 359-363

DOI: 10.5220/0001631303590363

Copyright

c

SciTePress

The objective here is to handle the high-

dimensional, complex data that is common in mod-

ern sensed systems, and still detect change point that

might occur in only one (or a few) variable among

hundreds. Consequently, we present a two-phased ap-

proach. In the first phase we identify the attributes re-

sponsible for the change point. With a much smaller

subset of attributes to work with in the second phase,

simpler methods can be used to identify the time(s)

at which the change(s) occur. The first phase uses a

novel transformation of the problem to one of super-

vised learning. Such a transformation was explored

by (Li et al., 2006). The work here adds a second

phase, uses a much more powerful feature selection

algorithm, and provides a more challenging example.

In Section 2 the change-point problem is transformed

to a supervised learning problem. Section 3 discusses

feature selection. Section 4 provides a realistic exam-

ple.

2 CHANGE POINTS WITH

SUPERVISED LEARNING

A supervised learning model requires a response or

target variable for the learning. However, no ob-

vious target is present in a change-point problem.

Still, a key element of a data stream is the time at-

tribute that provides an ordering for the measured vec-

tors. In a stationary data stream without any change

points, no relationship is expected between time and

the measured attributes. Conversely, if the distribu-

tion changes over time, such change should allow for

a relationship to be detected between the measured at-

tributes and time (Li et al., 2006). Consequently, our

approach is to attempt to learn a model to predict time

from the measurements in the data stream

t = g(x

1

, ..., x

p

) (1)

where t is the time of an observation vector and g()

is our learned model. If the time attribute can be pre-

dicted, a change in the measurement vectors is avail-

able to predict. Attributes that are scored to be im-

portant to this model are the subset of important vari-

ables. Consequently, phase one of our analysis can be

completed from this model and its interrogation. Any

number of change points can occur in this framework.

A more direct approach might attempt to model

each attribute as a function of time such as x

j

= g(t)

for j = 1, 2, . . . , p. However, separate models do

not use the relationships among the variables. A

change might break the relationships between vari-

ables within a significance difference in each variable

individually. Common examples in data streams de-

pict points that are not unusual for any attribute indi-

vidually, but jointly depict an important change.

Any monotonic function of time can be used as

the target attribute for the learner. The identify func-

tion used here is a simple choice and other functions

can be used to highlight or degrade the detection of

change points in different time periods. Also, any one

of many supervised learners can be applied. Our goal

is to detect a subset of important variables and this is

the primary purpose for our following selection.

Because we are most interested in an abrupt

change in the mean of one or more attributes in the

data stream it is sensible to use a supervised learner

that can take advantage of such an event in the sys-

tem. Furthermore, the phase one objective is to iden-

tify the important variables. Consequently, decision

trees are used as the base learners because they can

effectively use a mean change in only one or few pre-

dictor attributes. They also have intrinsic measures of

variable importance. Ensembles of decision trees are

used to improve the measure of variable importance

for the phase one objective.

3 FEATURE SELECTION

If an attribute changes over time, it should be more

useful to predict time than an attribute that is sta-

tistically stable. Consequently, the phase to iden-

tify changed attributes is based on a feature selection

method for a supervised learner. There are several ap-

proaches such as filter, wrapper, and embedded meth-

ods. An overview of feature selection was provided

by (Guyon and Elisseeff, 2003) and other other pub-

lications in the same issue. Also see (Liu and Yu,

2005). The feature selection phase needs to process

hundreds of attributes and potentially detect a contri-

bution of a few to the model to predict time. Fur-

thermore, in the type of applications of interest here,

the attributes are often related (redundant). Conse-

quently, the effect of one attribute on the model can

be masked by another. Moderate to strong interactive

effects are also expected among the attributes. Conse-

quently, a feature selection methods need high sensi-

tivity and the ability to handle masking and interactive

effects. We use a feature selection methods based on

ensembles of decision trees.

Tree learner are fast, scalable, and able to handle

complex interactive effects and dirty data. However,

the greedy algorithm in a single tree generates an un-

stable model. A modest change to the input data can

make a large change to the model. Supervised ensem-

ble methods construct a set of simple models (called

ICINCO 2007 - International Conference on Informatics in Control, Automation and Robotics

360

base learners) and use their vote to predict new data.

Numerous empirical studies confirm that ensemble

methods often outperform any single base learner

(Freund and Schapire, 1996), (Dietterich, 2000). En-

sembles can be constructed as parallel or serial collec-

tions of base learners. A parallel ensemble combines

independently constructed base learners. Because dif-

ferent errors can cancel each other, an ensemble of

such base learners can outperform any single one of

its components (Hansen and Salamon, 1990), (Amit

and Geman, 1997). Parallel ensembles are often ap-

plied to high-variance base learners (such as trees).

(Valentini and Dietterich, 2003) showed that ensem-

bles of low-bias support vector machines (SVMs) of-

ten outperformed a single, best-tuned, canonical SVM

(Boser et al., 1992).

A well-known example of a parallel ensemble is

a random forest (RF) (Breiman, 2001). It uses sub-

sampling and to build a collection of trees and injects

additional randomness through a random selection of

variable candidates of each node of each tree. The

forest can be considered a more sophisticated bag-

ging method (Breiman, 1996). It is related to random

subspace method of (Ho, 1998). A forest of random

decision trees are grown on bagged samples with per-

oformance comparable to the best known classifiers.

Given M predictors a RF can be summarized as fol-

lows: (1) Grow each tree on a bootstrap sample of the

training set to maximum depth, (2) Select at random

m < M predictors at each node, and (3) Use the best

split selected from the possible splits on these m vari-

ables. Note that for every tree grown in RF, about one-

third of the cases are out-of-bag (out of the bootstrap

sample). The out-of-bag (OOB) samples can serve as

a test set for the tree grown on the non-OOB data.

In serial ensembles, every new learner is based

on the prediction errors from previously built learners

so that the weighted combination forms an accurate

model. A serial ensemble results in an additive model

built by a forward-stagewise algorithm and Adaboost

introduced by (Freund and Schapire, 1996) is the best-

known example.

Neither parallel nor serial ensembles alone are

sufficient to generate an adequate best subset model

that accounts for masking, and detects more subtle

effects. A simple example by (Tuv, 2006) illustrated

this. In some cases, weak but independent predictors

are incorrectly promoted in the presence of strong, but

related predictors. In other cases the weak predictors

are not detected. An integrated solution is expected

to provide advantages and several concepts described

previously were integrated into a best subset selection

algorithm by (Tuv et al., 2007). Only a brief summary

is provided here. The best-subset algorithm contains

the following steps:

1. Variable importance scores are computed from a

parallel RF ensemble. Each tree uses a fixed depth

of 3-6 levels. There are some modified calcula-

tions based on OOB sample that are described in

more detail by (Tuv et al., 2007).

2. Noise variables are created through a random per-

mutation of each column of the actual data. Be-

cause of this random permutation, the noise vari-

ables are known to not be associated with the tar-

get. The noise variables are used to set a thresh-

old for statistically significant variable importance

scores to select important (relevant) variables

3. Within decision trees, surrogate scores can be cal-

culated from the association between the primary

splitter at a node and other potential splitters. The

details were originally provided by (?). These sur-

rogate scores describe how closely an alternative

splitter can mach the primary. This is turn pro-

vides a measure of masking between these vari-

ables. When such scores are combined from all

nodes in a tree and all trees in an ensemble, a ro-

bust metric for variable masking can be obtained.

A masking matrix is computed and noise variables

are again used to determine significance thresh-

olds. A set of short serial ensemble is used.

4. Masked variables are removed from the list of im-

portant variables

5. The target is adjusted for the currently identi-

fied important variables, and the algorithm is re-

peated. The adjustment calculates generalized

residuals that apply to either regression of classifi-

cation problems. Less important variables can be

more clearly identified once the dominant contrib-

utors are eliminated. Trees-based models are not

well-suited for additive models and the iteration

substantially improves the performance in these

cases.

4 ILLUSTRATIVE EXAMPLE

Because change-point detection is an unsupervised

learning task, simulated data is used with known

change points inserted. A data set to mimic a real

manufacturing environment includes 10 sensors that

each generate time series (with 100 time data points)

from given distributions. Each time series could be

represented as a trapezoid with added curvatures, an

oscillation with random phase in the center, and Gaus-

sian noise on the order of 10% of the signal. Cur-

vatures and the center oscillation phase are sampled

CHANGE-POINT DETECTION WITH SUPERVISED LEARNING AND FEATURE SELECTION

361

from fixed uniform distributions. This set of time se-

ries provides the results for one batch and the objec-

tive is to detect changes in a series of batches. The

dataset consists of 10000 batches and each 1000 sam-

ples there is a change induced by a shift in one of

internal parameters used to generate time series by its

standard deviation.

Such high-dimensional data can be analyzed di-

rectly, or a different representation can be used to ex-

tract features that might be of interest. For example,

Fourier transforms, discrete wavelet transforms, and

orthogonal polynomials are only a few of the methods

to represent high-dimensional data. Without a priori

information of features affected by a change point, the

set of features is extracted from these methods is still

often quite large.

Chebyshev polynomials are used here to repre-

sent this high-dimensional data. The representation

is y(x) = T

n

(x) where T

n

(x) by definition is a poly-

nomial solution of degree n of the equation

(1 − x

2

)

d

2

y

dx

2

− x

dy

dx

+ n

2

y = 0, (2)

where |x| ≤ 1 and n is a non-negative integer.

For n = 0 T

0

(x) = 1. Chebyshev polynomials

can also be calculated using one of useful proper-

ties: T

n+1

(x) = 2xT

n

(x) − T

n−1

(x) and T

n

(x) =

cos(n · cos

−1

(x)).

A set of Chebyshev polynomials {T

n

(x)}

n=0,1,...

is orthogonal with respect to the weighting function

(1 − x

2

)

−1/2

:

1

Z

−1

T

m

(x)T

n

(x)dx

√

1 − x

2

=

1

2

π δ

nm

,n>0,m>0

π ,n =0,m =0

, (3)

where δ

mn

is the Kronecker delta.

Using the last property we can represent any

piecewise continuous function f(x) in the interval

−1 ≤ x ≤ 1 as a linear combination of Chebyshev

polynomials:

∞

X

0

C

n

T

n

(x) =

f(x),where f (x) is continuous

f (x−0)+f(x+0)

2

in discontinuity points

(4)

Here

C

n

=

A

π

1

R

−1

f(x)T

n

(x)dx

√

1−x

2

,

A =

1, n = 0

2, n > 0

.

(5)

For a function {f

i

}

i=1,...,P

defined on a discrete

domain we calculate the coefficients of the Chebyshev

decomposition using a straightforward formula:

C

n

=

A

π

T

X

i=1

f

i

T

n

(x

i

)

p

1 − x

2

i

, (6)

where x

i

= −1 +

2

P

(i −

1

2

). Therefore, the coeffi-

cients {C

n

} become the features for the change-point

detection. We use first 25 coefficients for each time

series resulting in 250 features for each sample.

In the first phase of the analysis the feature selec-

tion algorithm simply uses a sequential batch index as

the target. The polynomial coefficients provide the in-

puts. The feature selection module identifies the dis-

tribution change and a set of features responsible for

the change.

In the second phase, moving T

2

statistics are

calculated using only the selected features between

n

1

/n

2

-samples prior/after the current data point, cor-

respondingly, to detect the change points:

T

2

=

n

1

n

2

(n

1

+ n

2

− 2)

n

1

+ n

2

(

y

1

− y

2

)

′

W

−1

(y

1

− y

2

) ,

(7)

where

W =

n

1

X

j=1

(y

1j

−

y

1

) (y

1j

− y

1

)

′

(8)

+

n

2

X

j=1

(y

2j

−

y

2

) (y

2j

− y

2

)

′

.

In the second phase, moving T

2

statistics are

calculated using only the selected features between

n

1

/n

2

-samples prior/after the current data point, cor-

respondingly, to detect the change points:

T

2

=

n

1

n

2

(n

1

+ n

2

− 2)

n

1

+ n

2

(

y

1

− y

2

)

′

W

−1

(y

1

− y

2

) ,

(9)

where

W =

n

1

X

j=1

(y

1j

−

y

1

) (y

1j

− y

1

)

′

(10)

+

n

2

X

j=1

(y

2j

−

y

2

) (y

2j

− y

2

)

′

.

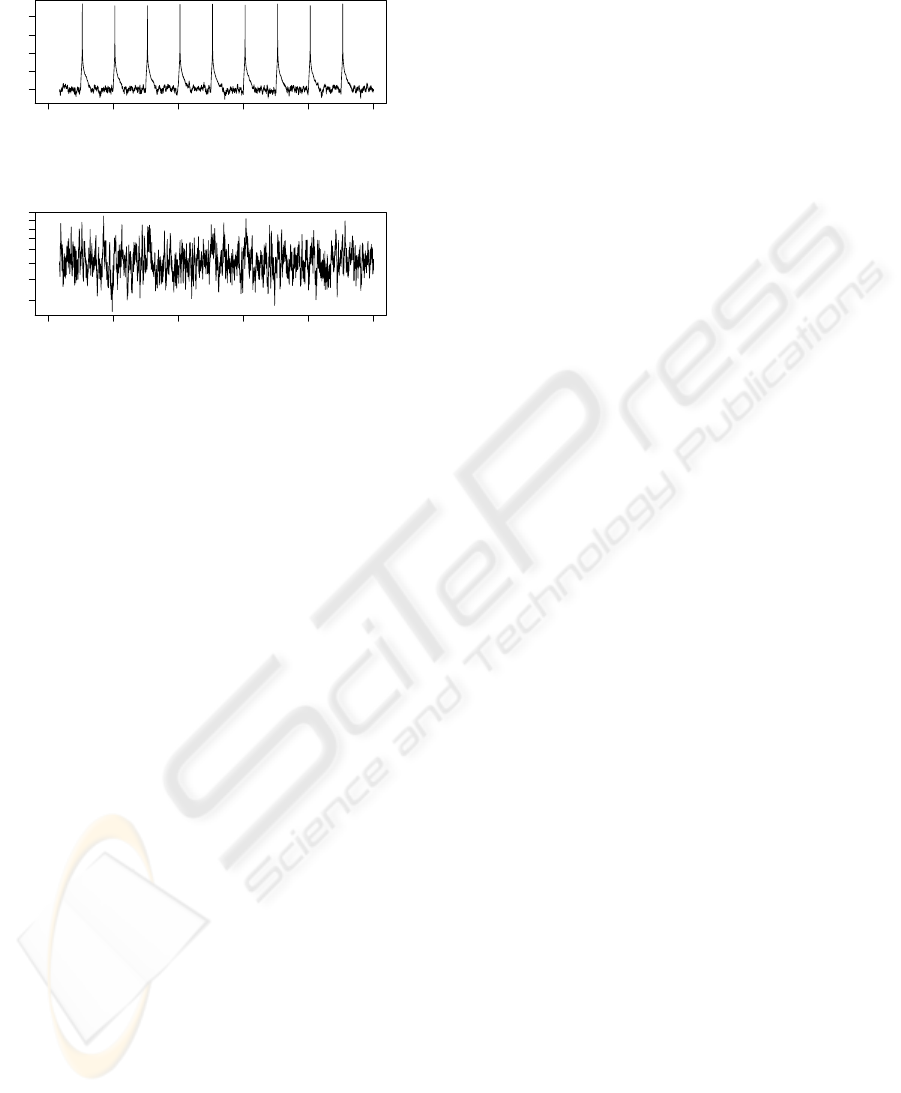

We retrain a model with each 200 samples using

all samples from the previous detected change point

until the current sample. We do not make predictions

on the first 100 samples in the beginning and after

a change point. The results are shown in Figure 1.

Here T

2

is shown with feature selection in the top fig-

ure and without feature selection in the bottom figure.

Notice that changes are not detected before feature

selection improves the sensitivity of the control chart.

After feature selection the changes are apparent.

5 CONCLUSIONS

As sensors continue to flourish in numerous disci-

plines, high-dimensional data becomes more com-

mon. Furthermore, the ability to detect changes in

ICINCO 2007 - International Conference on Informatics in Control, Automation and Robotics

362

0 2000 4000 6000 8000 10000

1 10 1000

sample index

T2, selected variables

0 2000 4000 6000 8000 10000

0.6 1.0 1.4 2.0

sample index

T2, all variables

Figure 1: Time series plot of T

2

with (top) and without

(bottom) feature selection.

a system or process over time remains an important

need in many applications. The results here illustrate

the success of a solution that integrates several impor-

tant elements. The transform of the inherently unsu-

pervised learning problem of change-point detection

to one of supervised learning with a time index as the

response, opens the analysis to a wide collection o

tools. A sophisticated feature selection algorithm can

then be applied to detect attributes that contribute to

a change. In the lower-dimensional space of these at-

tributes, the change point detection is a much sim-

pler problem and a number of simpler tools can be

applied. We uses a multivariate T

2

control chart, but

other control charts, or methodologies can be consid-

ered after the important dimensional reduction. The

illustrative example presents an simulation of an im-

portant practical case. One needs to summarize the

information from multiple time series. Consequently,

the dimensional space equals the number of series

times the length of each series and the feature selec-

tion becomes critical, and the example illustrates an

effective solution method for this problem.

ACKNOWLEDGEMENTS

This material is based upon work supported by

the National Science Foundation under Grant No.

0355575.

REFERENCES

Amit, Y. and Geman, D. (1997). Shape quantization and

recognition with randomized trees. Neural Computa-

tion, 9(7):1545–1588.

Belisle, P., Joseph, L., Macgibbon, B., Wolfson, D. B., and

Berger, R. D. (1998). Change-point analysis of neuron

spike train data. Biometrics, 54:113–123.

Boser, B., Guyon, I., and Vapnik, V. (1992). A training

algorithm for optimal margin classifiers. In Haussler,

D., editor, 5th Annual ACM Workshop on COLT, Pitts-

burgh, PA, pages 144–152. ACM Press.

Breiman, L. (1996). Bagging predictors. Machine Learn-

ing, 24(2):123–140.

Breiman, L. (2001). Statistical modeling: The two cultures.

Statistical Science, 16(3):199–231.

Dietterich, T. G. (2000). An experimental comparison of

three methods for constructing ensembles of decision

trees: Bagging, boosting, and randomization. Ma-

chine Learning, 40(2):139–157.

Freund, Y. and Schapire, R. E. (1996). Experiments with

a new boosting algorithm. In the 13th International

Conference on Machine Learning, pages 148–156.

Morgan Kaufman.

Guyon, I. and Elisseeff, A. (2003). An introduction to vari-

able and feature selection. Journal of Machine Learn-

ing Research, 3:1157–1182.

Hansen, L. K. and Salamon, P. (1990). Neural network en-

sembles. IEEE Trans. on Pattern Analysis and Ma-

chine Intelligence, 12(10):993–1001.

Ho, T. K. (1998). The random subspace method for con-

structing decision forests. IEEE Trans. on Pattern

Analysis and Machine Intelligence, 20(8):832–844.

Hotelling, H. (1947). Multivariate quality control-

illustrated by the air testing of sample bombsights.

Techniques of Statistical Analysis, pages 111–184.

Li, F., Runger, G. C., and Tuv, E. (2006). Supervised

learning for change-point detection. IIE Transactions,

44(14-15):2853–2868.

Liu, H. and Yu, L. (2005). Toward integrating feature selec-

tion algorithms for classification and clustering. IEEE

Trans. Knowledge and Data Eng., 17(4):491–502.

Pievatolo, A. and Rotondi, R. (2000). Analysing the

interevent time distribution to identify seismicity

phases: a bayesian nonparametric approach to the

multiple change-points problem. Applied Statistics,

49(4):543–562.

Tuv, E. (2006). Ensemble learning and feature selection.

In Guyon, I., Gunn, S., Nikravesh, M., and Zadeh, L.,

editors, Feature Extraction, Foundations and Applica-

tions. Springer.

Tuv, E., Borisov, A., Runger, G., and Torkkola, K. (2007).

Best subset feature selection with ensembles, artificial

variables, and redundancy elimination. Journal of Ma-

chine Learning Research. submitted.

Valentini, G. and Dietterich, T. (2003). Low bias bagged

support vector machines. In ICML 2003, pages 752–

759.

CHANGE-POINT DETECTION WITH SUPERVISED LEARNING AND FEATURE SELECTION

363