SET: A QUESTIONABLE SECURITY PROTOCOL

Charles A. Shoniregun and Songhe Zhao

School of Computing & Technology, University of East London

4-6 University Way Docklands, London

United Kingdom, E6 5NJ

Keywords: Secure Electronic Transaction (SET), Dual Signature, Elliptic Curve Cryptography (ECC).

Abstract: The Secure Electronic Transaction (SET) was developed by Visa and MasterCard in 1997. The SET is a

protocol that is theoretically perfect with very high expectation to provide secured electronic financial

transactions. It also provides a ‘dual signature’ as it hides credit card numbers from the merchants, and

purchase details from the bank. This paper exploits the weaknesses that led to SET’s failure and proposed

SET’s encryption process with elliptic curve cryptography (ECC).

1 INTRODUCTION

The SET is a standard protocol for ensuring the

security of electronic financial transactions on the

Internet, which has been endorsed by virtually all the

major players in the electronic commerce arena,

including IBM, MasterCard International, Visa

International, Microsoft, Netscape, GTE, ViriSign,

SAIC and Terisa. The SET defines a detailed secure

transaction process among all participants. It mainly

replies on the sciences of cryptography to implement

its functions for securing electronic transactions on

the Internet. The cryptography provides two different

encryption mechanisms and an authentication

mechanism. SET employs DES symmetric

encryption and RSA asymmetric encryption to

provide functions of data encryption, digital signature

and digital envelope, which can provide guarantee for

the security of information transmitted over the

Internet. To enable merchants to verify transactions,

SET put the public key into an electronic document

(i.e. digital certificate). The certificate is then signed

by a trusted third-party, such as certificate authority

(CA), which can then be verified from their

certificate and so on in a hierarchy of trust. And it will

also protect buyers by providing a mechanism for

their credit card number to be transferred directly to

the credit card issuer for verification and billing

without the merchant being able to see the number.

With SET, a user is given an electronic wallet (digital

certificate) and a transaction is conducted and

verified using a combination of digital certificates

and digital signatures among the purchaser, a

merchant and the purchaser's bank in a way that

ensures authenticity and privacy.

2 RELATED WORK

The SET handles processes for once-off merchant

and card holder registration, for making a purchase

and getting the payment authorized through a bank’s

network gateway and for subsequent payment to the

merchants. SET pilots have been conducted around

the world, but very few have yet been implemented.

The SET protocol provides four main advantages for

securing data/information transfer:

Confidentiality: using two forms of

cryptography---DES and RSA to protect transmitted

messages from intercepting.

Integrity: using one-way cryptographic hashing

algorithms and digital signatures to make sure that

the messages transmitted have not been modified in

transit.

Authentication: using X.509v3 digital certificates

which assure that

the parties involved in the

transaction are who they claim to be, and prevent

them from denying that they sent a message (i.e.

non-repudiation).

¾ Privacy: using cryptography to make sure the

information is only available to parties in a

transaction when and where necessary.

313

A. Shoniregun C. and Zhao S. (2007).

SET: A QUESTIONABLE SECURITY PROTOCOL.

In Proceedings of the Third International Conference on Web Information Systems and Technologies - Internet Technology, pages 313-319

DOI: 10.5220/0001291903130319

Copyright

c

SciTePress

There have been remarkable efforts aimed at the

SET’s weaknesses. These efforts are effective in

overcoming the weaknesses and reducing

redundancies. Abbott (1999) presented that although

SET offers a complete card payment system that

manages financial risk and defines interoperability, it

requires that software be installed in the banking

network, at merchants’ locations, and on consumers’

PCs. This deployment obstacle has slowed and

complicated the adoption. Weishaupl et al. (2006)

developed gSET as a solution for the unsolved

problems in the field of dynamic trust management

and secure accounting in commercial virtual

organizations. The gSET establishes trust and

privacy between entities in a Grid environment by

adapting the concept of SET used for electronic

credit card transfers in e-Commerce. However, this

solution is known as an enabling step to make Grids

a platform for commercial workflows but it is not a

solution to address problems of SET’s adoption and

deployment. Bella et al. (2005) produced an accurate

formal model to identify the SET protocol goals and

then to prove them. In their study, they were

troubled by the complexity of SET protocol so that

they are not clear whether model checking could

cope with this SET’s complexity. it is very clear that

the complexity of SET is the crucial problem for its

adoption. This rather serious time lag issue could

come to be resolved by another more efficient

method called elliptic curve security. Although RSA

employed by SET is the most popular public-key

cryptosystem today, the long-term trends such as the

proliferation of smaller, simpler devices and

increasing security needs will make continued

reliance on RSA more challenging over time.

3 DIGITAL SIGNATURE

The SET uses digital signatures and certificates

stored in an electronic “wallet” on the users’

personal computers and on the merchants’ websites.

The dual signature which is employed as the SET’s

digital signature is issued by a trusted third party

certificate authority and the user's certificate

contains card details. It is encrypted in such a way

that it can only be read by the card issuer, not the

merchant.

The dual signature is generated by creating the

message digest of both messages sent by a sender,

concatenating the two digests together, computing

the message digest of the result and encrypting this

digest with the sender’s private signature key. A

recipient of either message can check its authenticity

by generating the message digest on its copy of the

message, concatenating it with the message digest of

the other message (as provided by the sender) and

computing the message digest of the result. If the

newly generated digest matches the decrypted dual

signature, the recipient can trust the authenticity of

the message (Secure Electronic Transaction LLC,

1997). Privacy and Authentication are achieved

through the use of digital signatures. Digital

signatures are aimed at achieving the same level of

trust as a written signature has in real life. This helps

achieve non-repudiation, as the consumer cannot

later establish that the message wasn't sent using his

private key (IBM Corporation, 1998).

3.1 Construction of Dual Signature

In SET, when a customer has place an order from a

merchant’s website and is going to make a payment

for the order, he/she needs to send the order

information (OI) to the merchant and payment

information (PI) to the merchant’s acquirer through

the merchant. In the progress of sending OI and PI to

destinations, the customer needs to use hash

algorithm (SHA-1) to produce message digest (MD)

respectively for OI and PI. These two MDs are then

concatenated and then computed to payment and

order message digest (POMD) by using the hash

algorithm again. Finally, the customer encrypts the

POMD with the customer’s private signature key

(KRc) in order to create the dual signature (DS). The

operation formula is:

When the merchant is in the possession of OI,

PIMD and DS, and PI, the merchant can use the

customer’s public key (KUc), which is taken from

the customer's certificate to compute two quantities.

The operation formula is:

If these two quantities are equal, the merchant

has verified the signature. Similarly, when the

acquirer is in the possession of PI, OIMD and DS,

the acquirer can use KUc to compute other two

quantities. The operation formula is:

WEBIST 2007 - International Conference on Web Information Systems and Technologies

314

Again, if these two quantities are equal, the

acquirer has verified the signature. In summary:

¾ The merchant has received OI and verified

the signature.

¾ The acquirer has received PI and verified

the signature.

¾ The customer has linked the OI and PI and

can prove the linkage.

Within SET, dual signatures are used to link an

order message sent to the merchant with the

payment instructions containing account information

sent to the Acquirer. When the merchant sends an

authorization request to the Acquirer, it includes the

payment instructions sent to it by the cardholder and

the message digest of the order information. The

Acquirer uses the message digest from the merchant

and computes the message digest of the payment

instructions to check the dual signature.

4 CRICISM OF SET AND

ECC-BASED IMPROVEMENT

Although the advantages of SET had ever attracted

our sight, this focus quickly moved to its weaknesses

and the relevant researches were carried out soon

after the failure of SET happened.

4.1 Weaknesses of SET

The SET protocol has the potential of securing the

electronic financial transactions over the Internet so

as to enable e-Commerce to be safe and attractive to

consumers, but unresolved problems and issues

which caused the failure of employing SET as a

dominate protocol in e-Commerce as follows:

i Complex and slow processing:

The SET models all of the players involved in

electronic financial transactions. It is a complex

protocol because it so totally simulates these

existing real world processes. The ultimate

high level of security that SET provides is

implemented by a very complex system which

causes the processing transactions to be quite

slow. Generally, the access operations to the

merchant’s server can approach 6 times (Zhao,

2005); moreover, SET also implements a deal

of computing for public key encryption. The

workload of the merchant’s server hereby is

quite heavy so that overload is most likely to

happen. Lag times of up to 50 seconds have

been reported for the processing of a typical

cardholder initiated purchase request to the

approval response from the acquirer and the

finalization of the transaction by the merchant’s

server (Keenan, Disenso and Green, 1998).

This matter is critical for average SET’s

consumers because the key advantage of

e-Commerce is to provide ease-of-use

applications for its participants. Nobody would

like to wait for a response around 50 seconds

after sending a purchase request. A common

download time for a Webpage should be around

15 seconds and if it above 30 seconds then the

customer will stop waiting and move over to

another Website (Shoniregun, 2005), not even

for a very attractive Webpage. As a result, it’s

not recommended that that any response over

15 seconds is proper, especially since there is

little or no feedback to reassure and update the

cardholder about the progress of the transaction

processing (Wolrath, 1998).

ii Inconvenient and expensive deployment and

implementation:

To implement SET, merchants are required to

invest in new software and build their

businesses around a complex transaction

infrastructure, but it doesn’t make them jump

with joy (Friedman, 1998). Merchants who

want to benefit from SET have to install

SET-enabled applications in their systems. It

doesn’t look inconvenient and expensive to the

installation in a single merchant’s system.

However, e-Commerce is a global electronic

transaction over the Internet. It may create

considerable profit only if a great number of

people step into this virtual business world to

play this game. Therefore, it’s necessary for

absolute majority of merchants to install

SET-enabled applications in their systems. This

needs a huge investment and long time to

deploy far and wide, but most people don’t

want to be at risk before making an investment

and seeing other’s implementation. The latter

slows down the deployment of SET’s, not only

to merchants, but also to the installation of

SET-enabled applications in client end is also

obstacle for SET’s implementation. Ease-of-use

SET: A QUESTIONABLE SECURITY PROTOCOL

315

is the key to e-Commerce as well as SET. But

the serious question remains about just how

intuitive it will be for users to install the

necessary applications to do SET-based

transactions. Neither Microsoft nor Netscape

are in any rush to build SET into their browsers

until there is a demand for it. But merchants

won’t support it until their customers ask for it,

and their customers won’t ask for it until it’s

built into their browsers. Although Vendors like

VeriFone and IBM have developed SET wallet

plug-ins for the popular Web browsers, Internet

users are not keen on using external plug-ins.

Because they have to install SET from the

external plug-ins that adds payment

functionality to a browser, and also register

with a financial institution or trusted third party,

which then issues digital certificates that

identify the cardholder to the merchant and

vice versa. Although in the long run SET

backers expect certificates to be included in

wallets -- which in turn will be built into

browsers.

Generally speaking, different versions of

SET software are currently available in the

market but it is critical that these packages

interoperate. Without interoperability, any

protocol is dead. SET defines interoperability

between all parts of the card-payment process.

A system can be built with parts from multiple

vendors. To offer these benefits, SET requires

that software be installed in the banking

network, in merchants’ systems, and on

consumers’ PCs. This “deployment obstacle”

has slowed the adoption of SET, which also

requires that certificates be issued to all parties.

These requirements make SET quite

inconvenient and expensive to deploy all over

the world.

iii Lack key and certificate management:

Today’s popular operating systems are

unreliable and insecure, so they are highly

vulnerable to attack, particularly when

connected to the Internet. For this reason,

non-repudiation really exists only when private

signing keys are kept out of untrusty PCs

(Abbott, 1999). But SET refers nothing about

how to securely keep keys and certificates out

of attacks after finishing an electronic

transaction. It appears that these will need to be

stored on participants' workstations and servers,

or additional peripherals installed on

workstations and servers to handle a secure

token (Clark, 1996). A secure token, such as a

smart card, is a good tool to store and exercise

private signing keys and certificates for its

holder. It can also provide an easy way for

signing keys and certificates to be issued and

carried around. The SET was designed

specifically for smart cards, and all SET wallets

support tokens. This beneficially ties token

directly to e-Commerce, because the certificate

authenticates the customer as a cardholder and

directly signifies that transaction is taking place.

However, smart cards are distributed very

slowly, because no one has solved the problem

of how to get card readers attached to

everyone’s PC. But other form-factor tokens

are appearing, including small

universal-serialbus tokens (key fobs, for

example) that can do the same job. Some SET

pilots also are being conducted without tokens,

with the expense of the added complexity of

distributing and managing certificates as

software files. In fact, the smart card’s set-up is

beyond the average cardholder. Actually it's a

very troublesome procedure.

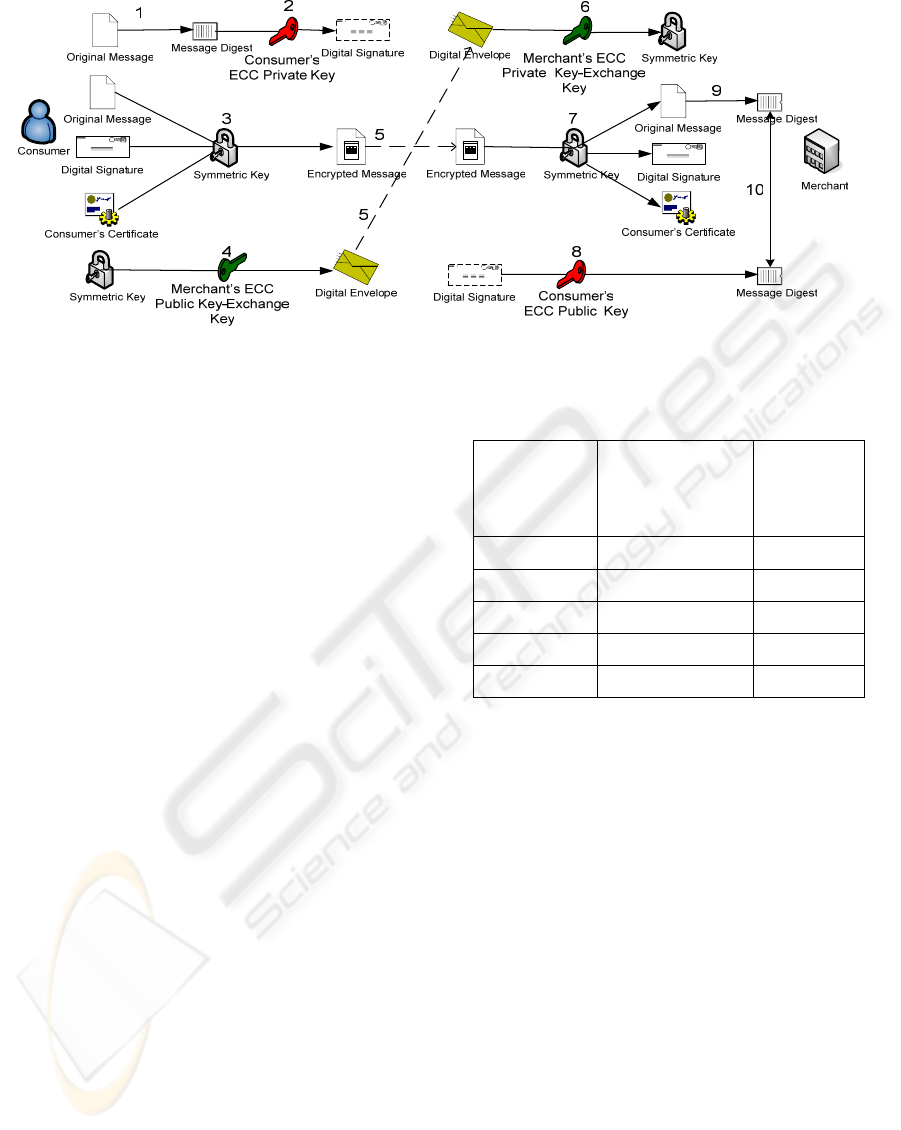

4.2 ECC-based Improvement of SET

Our proposition is based on substituting RSA

algorithm by using ECC to provide SET’s

cryptography (See Figure 1). Our laboratory

experiments have proved that ECC provides greater

security and more efficient performance than the

first generation public key techniques.

i ECC from the consumer:

The consumer use the ECC hash algorithm

(SHA-1) to produce message digest for the

original message and encrypt the message

digest with ECC private key to produce the

digital signature. This generates a random

symmetric key that encrypt the original

message, digital signature and a copy of the

consumer’s certificate, which contains public

signature key. The symmetric key is encrypted

by using the merchant’s ECC public

key-exchange key and the encrypted key

(digital envelope) will be sent to the merchant

along with the encrypted message. Sending a

set of message to the merchant consists of the

symmetric encrypted original message, as well

as the asymmetrically encrypted symmetric key

(the digital envelope).

WEBIST 2007 - International Conference on Web Information Systems and Technologies

316

Figure 1: SET’s encryption process with ECC.

ii ECC from the merchant:

Receiving the set of message from the

consumer and decrypting the digital envelope

with the ECC private key-exchange key to

retrieve the symmetric key. The consumer’s

digital signature and certificate would be

required in other to decrypt the original

message. Decrypting the consumer’s digital

signature with the ECC public key would

enabled the original message digest to produce

a new message digest of the decrypted original

message and compare the message digest

with the one obtained from the consumer’s

digital signature.

The ECC enhance the process in the SET’s

digital signature and inverse the process to provide

the message digest by decrypting the digital

signature. Moreover, the process related to the digital

envelope is also served by this solution. As a result

of this ECC-based solution, the duration of SET’s

encryption process can be reduced much more than

RSA-enabled process. The discussion section

focuses on how the security level of the encryption

will advance according to the features of ECC.

5 DISSCUSSION

In comparison with RSA, ECC offers the same level

of security using much smaller keys but faster

computations and less resourceful on memory.

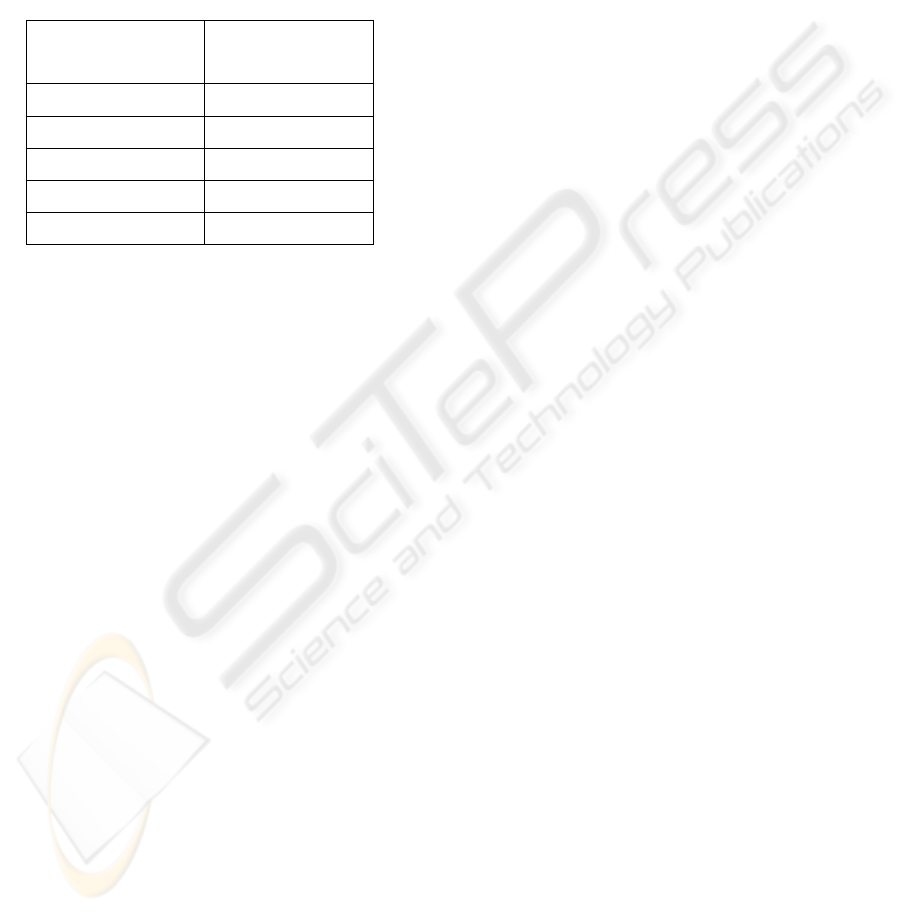

Table 1: Comparison of key sizes.

Symmetric

Key Size

(bits)

RSA and

Diffie-Hellman

Key Size (bits)

Elliptic

Curve Key

Size (bits)

80 1024 160

112 2048 224

128 3072 256

192 7680 384

256 15360 521

The Table1 shows the key sizes that protected the

keys used in conventional encryption algorithms like

the (DES) and (AES) together with the key sizes for

RSA, Diffie-Hellman and elliptic curves that are

needed to provide equivalent security.

Notably, the use of 1024-bit RSA does not match

the 128-bit or even 112-bit security level now used

for symmetric ciphers in SET. This indicates the

need to migrate to larger RSA key sizes in order to

deliver the full security of symmetric algorithms

with more than 80-bit keys. However, RSA

Laboratories stated that 1024-bit RSA to be unsafe

for data that must be protected beyond 2010 and

recommends larger keys for longer term protection

(Kaliski, 2003). In the case of providing higher key

sizes, RSA will increase much more the time cost of

the encryption process in SET. For example,

employing RSA or Diffie-Hellman to protect 128-bit

AES keys should use 3072-bit parameters, which is

three times longer than the size of 1024-bit in use

throughout the Internet today. However, the

SET: A QUESTIONABLE SECURITY PROTOCOL

317

equivalent key size for elliptic curves is only 256

bits. It’s obvious that as symmetric key sizes

increase the required key sizes for RSA and

Diffie-Hellman increase at a much faster rate than

the required key sizes for ECC. Hence, ECC offer

more security per bit increase in key size than either

RSA or Diffie-Hellman public key systems.

Table 2: Relative computation costs of Diffie-Hellman and

elliptic curves.

Security Level (bits)

Ratio of DH Cost:

EC Cost

80 3:1

112 6:1

128 10:1

192 32:1

256 64:1

Besides providing better security, ECC also are

more computationally efficient than the first

generation public key systems, RSA and

Diffie-Hellman. Although elliptic curve arithmetic is

slightly more complex per bit than either RSA or DH

arithmetic, the added strength per bit more than

makes up for any extra compute time (See Table 2).

The following table shows the ratio of DH

computation versus EC computation for each of the

key sizes listed in Table 1.

Closely related to the key size of different public

key systems is the channel overhead required to

perform key exchanges and digital signatures on a

communications link. The key sizes for public key in

Table 1 (above) is also roughly the number of bits

that need to be transmitted each way over a

communications channel for a key exchange. In

channel-constrained environments, elliptic curves

offer a much better solution than first generation

public key systems like Diffie-Hellman.

In choosing an elliptic curve as the foundation of

a public key system there are a variety of different

choices. The National Institute of Standards and

Technology (NIST) has standardized on a list of 15

elliptic curves of varying sizes. Ten of these curves

are for what are known as binary fields and 5 are for

prime fields. Those curves listed provide

cryptography equivalent to symmetric encryption

algorithms with keys of length 80, 112, 128, 192,

and 256 bits and beyond. In our solution, it

recommends that SET employs the ECC with 256,

384, and 521 bits. It is expected to show enhanced

speed on the SET payment gateway and potential

cost savings. It also promises to lower the capability

threshold for small devices to perform strong

cryptography, and increase a server’s capacity to

handle secure connections (Lenstra and Verheul,

2001).

6 CONCLUSION

The SET security guarantee is achieved by using the

cryptography but is a very costly technology. The

three main weaknesses of SET have been discussed

and we have also proposed the ECC model to

enhance not only the higher level security but also to

perform more efficient than RSA. Our future work

will focus on the SET key and certificate

management.

REFERENCE

Abbott, S., (1999). ‘The debate for secure E-commerce’,

UNIX Review's Performance Computing, Vol 17, Iss 2,

pp. 37

Bella, G., Massacci, F. and Paulson, L.C., (2005). ‘An

overview of the verification of SET’, International

Journal of Information Security, Heidelberg

(1615-5270), Vol.4, Iss.1-2, pp.17

Clark, R., (1996). ‘The SET Approach to Net-based

Payments’ [online], Available from:

http://www.anu.edu.au/people/Roger.Clarke/EC/SETO

view.html [Accessed 16 September 2006]

Kaliski. B., (2003). ‘TWIRL and RSA Key Size’ [online],

RSA Laboratories Technical Note. Available from:

http://www.rsasecurity.com/rsalabs/technotes/twirl.ht

ml [Accessed 25 September 2006]

Keenan, V., Disenso and Green, (1998). ‘PROMISES:

What ever happened to SET?’ [online], Available from:

http://www.herring.com/mag/issue51/promises.html

[Accessed 28 September 2006]

Friedman, M., (1998). ‘SET standard not exactly hitting

the fast lane’, Computing Canada, Vol 24, Iss 23, pp

26

IBM Corporation, (1998). ‘An overview of the IBM SET

and the IBM CommercePoint Products’ [online],

Available from:

http://www.software.ibm.com/commerce/set/Over--vie

w.html [Accessed 11th September 2006]

Lenstra, A. and Verheul, E., (2001). ‘Selecting

Cryptographic Key Sizes’, Journal of Cryptology, Vol.

14, pp. 255-293.

WEBIST 2007 - International Conference on Web Information Systems and Technologies

318

National Security Agency, (unknown). ‘The Case for

Elliptic Curve Cryptography’ [online], Available from:

http://www.nsa.gov/ia/industry/crypto_elliptic_curve.c

fm [Accessed 03 October 2006]

Shoniregun, C.A., (2005). ‘Impacts and Risk Assessment

of Technology for Internet Security: Enabled

Information Small-Medium Enterprises (TEISMES)’,

USA: Springer, pp. 14-30

Weishaupl, T., Witzany, C. and Schikuta, E., (2006).

‘gSET: Trust Management and Secure Accounting for

Business in the Grid’, Proceedings of the Sixth IEEE

International Symposium on Cluster Computing and

the Grid (CCGRID'06) - Volume 00, pp. 349-356

Secure Electronic Transaction LLC, (1997). ‘SET Secure

Electronic Transaction Specification: Book 1 Business

Description – Version 1’, pp. 12-29

Stallings, W., (2002). Introduction to Secure Electronic

Transaction, USA: Prentice Hall.

Wolrath., E., (1998). ‘Secure Electronic Transaction: a

market survey and a test implementation of SET

technology’, Master thesis, Uppsala University.

Zhao, Q., (2005). ‘Network Security and Electronic

Commerce’, China: Tsinghua University Publications,

pp. 171-225

SET: A QUESTIONABLE SECURITY PROTOCOL

319