Impact of Non-financial Information on Digitalization of Business on

the Sustainable Development of Russian Companies

Natalia N. Khakhonova

1a

, Yulia N. Kirkach

1b

and Irina N. Yemelyanova

2c

1

Rostov State University of Economics (RINH), 69 Bolshaya Sadovaya St., Rostov-on-Don, Russian Federation

2

Russian Economic University named after G.V. Plekhanov branch in Pyatigorsk, 8 Kuchura St., Pyatigorsk, Russian

Federation

Keywords: Non-Financial Information, Non-Financial Reporting, Covid-19 Pandemic, Company Digitalization.

Abstract: The article reveals the role of non-financial data for sustainable development purposes. In the era of the digital

economy, along with traditional non-financial information, which includes data on financial, production,

intellectual and human resources capacity, as well as environmental and social policies, we consider it

necessary to disclose information on the digitalization of the company, which will contribute to increasing

confidence in the company's activities on the part of interested users. This area is particularly relevant for

companies in the post-transition economy, as Russian business is currently in particular need to improve

Russian business's investment attractiveness to maintain its sustainable development.

1 INTRODUCTION

In today's global economy, non-financial and social

information about a company is a critical business

reporting component. The development of the ideas

of sustainable development of companies and the

need to follow corporate social responsibility

principles has led to the fact that standard financial

reporting is no longer sufficient. Most global and

domestic companies already pay great attention to

non-financial information about themselves and

publish annual non-financial statements.

The purpose of public non-financial reporting is

to provide organizations with meaningful, accurate,

as well as timely, reliable, and objective information

about their environmental, economic, social, and

governance performance to meet the information

needs and requests of stakeholders.

Given that most non-financial reporting

companies are digitizing their business, we consider

it appropriate to disclose non-financial information

describing the level of digitalization of the company

and the degree of reliability of its digital environment.

a

https://orcid.org/0000-0003-3327-4561

b

https://orcid.org/0000-0002-6655-102X

c

https://orcid.org/0000-0001-7038-8467

2 MATERIALS AND METHODS

With the digitalization of the economy, data from

various types of accounting, such as financial, tax,

management, social, environmental, as well as

promising methods and technologies, such as Big

Data, machine learning, artificial intelligence, etc.,

are used to disclose non-financial information.

This will expand the range of non-financial

indicators of investment attractiveness with

additional diagnostic or predictive value, particularly

evaluation indicators as peculiar indicators of

investment attractiveness.

In the course of the study, general scientific

methods were used, including analysis of the practice

of reflecting non-financial information on companies'

digitalization in the energy industry. The application

of these methods made it possible to achieve the set

objectives and to obtain the following results.

272

Khakhonova, N., Kirkach, Y. and Yemelyanova, I.

Impact of Non-financial Information on Digitalization of Business on the Sustainable Development of Russian Companies.

DOI: 10.5220/0010589302720277

In Proceedings of the International Scientific and Practical Conference on Sustainable Development of Regional Infrastructure (ISSDRI 2021), pages 272-277

ISBN: 978-989-758-519-7

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

3 RESULTS

Russian companies need investment to cope with the

COVID-19 pandemic successfully. In this regard, we

believe that to improve investment attractiveness in

the pursuit of sustainable development, Russian

companies need to disclose non-financial information

about the digitalization of their activities in the

context of the following aspects:

Company's IT strategy: defines areas of

digitalization of processes and implementation

of information technology projects;

IT strategy implementation areas: for each area

it is necessary to define the implementation

timeframe, budgets and internal business

customers;

Types of digital technologies used in the

company's operations: discloses information

on digital technologies used to optimize and

automate business processes and reduce costs;

Cybersecurity: demonstrates information on

measures and actions aimed at maintaining

information security (maintaining data

integrity, availability, confidentiality),

identification of cyber threats (malware, social

engineering, phishing, ransomware).

Regardless of the size of the company, the

implementation of digitalization processes in Russian

companies will help:

optimization and automation of business

processes;

operational management and execution of

various business tasks;

reducing costs and labor costs;

stable development of the company;

improving the investment attractiveness of the

business and the inflow of investments.

4 DISCUSSION OF THE

RESULTS

Sustainable development is becoming a macro-trend

in modern society. In an effort to improve their

investment attractiveness, companies try to

demonstrate their competitive advantages, stable

performance, and concern for society through non-

financial information. Non-financial information

means any data obtained from sources other than the

organization's financial statements or accounting

systems and disclosed in non-financial reports. The

use of non-financial reports in the global practice is

associated with the development of the concept of

corporate responsibility or sustainable development.

Emerging and evolving as a PR tool, or

communication system, non-financial reporting in the

21st century has increasingly been used as a means of

stakeholder feedback aimed at improving investment

attractiveness.

According to the Sustainable Development

Concept, sustainable development indicators include:

1) "indicators of social aspects (poverty reduction;

dynamics of demographic processes and

sustainability of development; development of

education, literacy, training programs; protection and

improvement of human health; ensuring sustainable

development of places of mass habitation);

2) economic dimension indicators (international

cooperation to enhance sustainable development and

related domestic policies; changing consumption

patterns; financial resources and mechanisms for their

rational use; transfer of environmentally friendly

technologies, cooperation, and capacity

development);

3) environmental indicators (protection of water

quality and drinking water supply; protection of

oceans, all types of seas and coastal areas; an

integrated approach to land use planning and

management; management of fragile ecosystems:

deserts and arid zones, mountain areas; ensuring

sustainable agricultural and rural development; air

protection; solid waste management and sewage

issues, toxic chemicals, hazardous waste; radioactive

waste processing and neutralization; combating

desertification and degradation of coastal lands; and

water pollution;

4) indicators of institutional aspects (integration

of environmental interests and development

principles into decision-making; science and

sustainable development; international legislative

instruments and mechanisms; provision and

exchange of information for strategic decision-

making; strengthening of key population groups)".

The above information is reflected in

sustainability reporting in terms of the three aspects

presented in Table 1.

Impact of Non-financial Information on Digitalization of Business on the Sustainable Development of Russian Companies

273

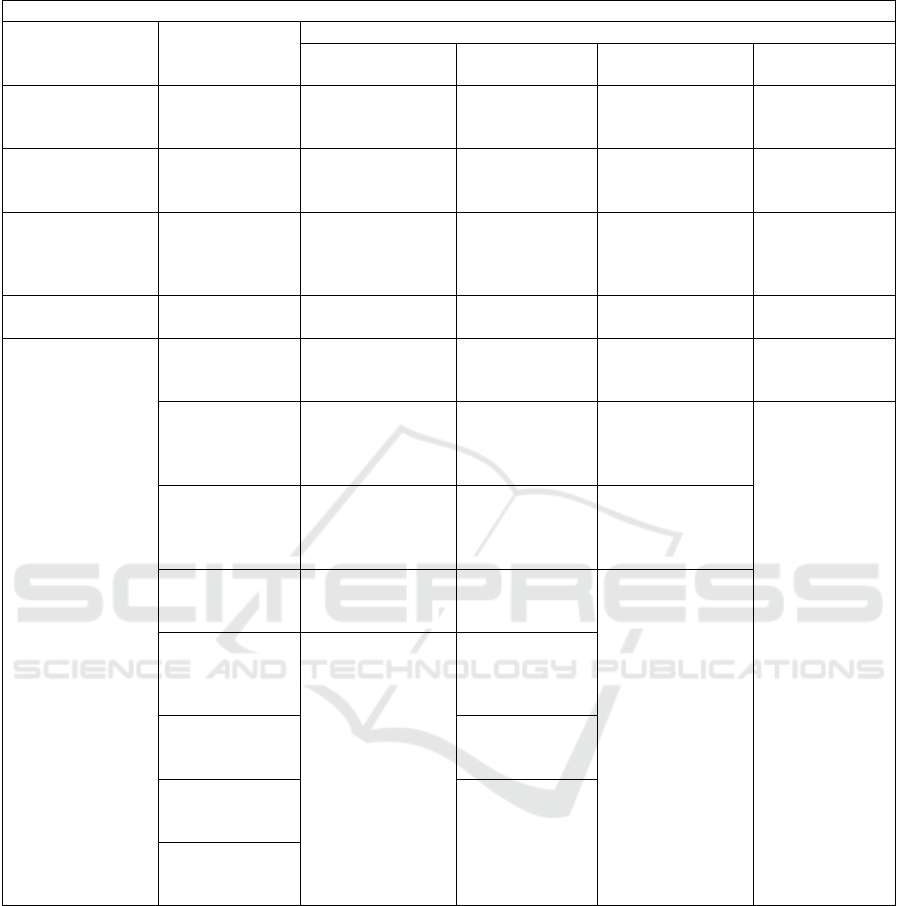

Table 1: Elements of corporate reporting in accordance with the GRI "Global Reporting Initiative" G4 standard.

Elements of cor

p

orate re

p

ortin

g

Economic

dimension

Environmental

aspect

Social as

p

ect

Labour practices

and decent wor

k

Human rights Society

Product

responsibility

Economic

performance

Materials Employment Investments

Local

communities

Consumer

health and

safet

y

Market presence Energy

Employee-

management

relations

Non-

discrimination

Anti-corruption

efforts

Product and

service labeling

Indirect economic

impacts

Water

Health and safety

in the workplace

Freedom of

association and

collective

b

ar

g

ainin

g

Government

policy

Marketing

communications

Procurement

p

ractices

Biodiversity

Training and

education

Child labour

Barrier to

competition

Consumer

p

rivac

y

Emissions

Diversity and

equal opportunity

Forced or

compulsory

labou

r

Compliance Compliance

Discharges and

waste

Equal

remuneration for

women and men

Security

practices

Assessing the

impact of

suppliers on

societ

y

Products and

services

Assessment of

supplier labour

practices

Rights of

indigenous and

minority

p

eo

p

les

Community

Impact Grievance

Mechanisms

Compliance

Grievance

mechanisms for

labour practices

Evaluation

Transport

Assessment of

suppliers'

compliance with

human ri

g

hts

General

information

Human rights

complaint

mechanisms

Environmental

assessment of

suppliers

Environmental

grievance

mechanisms

As shown in Table 1, in sustainability reporting,

the main block of information falls on the social

aspect, which details human rights, decent work

organization, legitimacy of labor relations, etc.

Sustainability reporting is internationally

widespread and trusted, but despite this, the volume

of other types of reports is increasing every year. In

practice, non-financial reports such as risk reports,

marketing policy reports, intellectual potential reports

are generated. Integrated reporting, which is

governed by the International Integrated Reporting

Standard published in 2010, is currently the most

popular. This type of reporting expands the

information base provided to interested users - it

contains information on six types of company capital:

financial, production, social and reputation, human,

intellectual and natural. According to the definition

proposed by the International Integrated Reporting

Council, integrated reporting refers to "a new model

of corporate reporting based on the concept of

integrated thinking, involving the interlinking of

financial and management reporting, corporate

governance and remuneration reports, and

sustainability reports". Integrated reporting aims to

provide information that enables interested users to

assess an organization's ability to create value over

ISSDRI 2021 - International Scientific and Practical Conference on Sustainable Development of Regional Infrastructure

274

time. Integrated reporting is designed to support a

more sustainable business environment and better

decision-making by financial capital providers.

"Integrated reporting is characterized by an overall

focus on conciseness, strategic focus and future

prospects, the interconnectedness of information,

capitals, business model, ability to create value over

the short, medium and long term, and financial capital

providers as the primary target audience". In general,

integrated reporting is designed to provide the user

with relevant information that is material to form a

conclusion about the advisability of expanding a

corporate business or investing in it.

Thus, non-financial reports, regardless of the

concept of its preparation, traditionally disclose

information on the resource potential of the company

in the context of the following directions:

financial capacity;

productive capacity;

intellectual capacity;

human capacity;

environmental policy;

social policy.

The presented volume of non-financial

information reflected in non-financial reports is

informative and demanded by interested users.

However, the current crisis caused by the coronavirus

pandemic has served to drive the demand for

information that characterizes a company's level of

digitalization. The point is that the COVID-19

pandemic can be seen as a kind of test for the

resilience of exactly those systems, tools, and

mechanisms that were relevant to the "pre-

coronavirus" world and could trigger something new.

Observations during the COVID-19 pandemic show

that those businesses that were able to promptly move

to remote work by applying modern information and

communication technologies, especially in their

advanced technical standard - digitalization - were

able to advance and strengthen the logistical

capabilities of post-industrial economy development.

Digitalization processes were in demand even

before the COVID-19 pandemic, and attempts to

introduce them into Russian practice were made not

only by the business community, but also by the

government. The introduction of digital technologies

in the economy and social sphere became one of the

state's national development goals back in 2018. To

implement it, Decree No. 204 of the President of the

Russian Federation of May 7, 2018, "On National

Goals and Strategic Development Objectives of the

Russian Federation for the period until 2024", the

following tasks were defined:

increase in domestic spending on the

development of the digital economy from all

sources (by share in the gross domestic

product);

creation of a sustainable and secure

information and telecommunication

infrastructure for high-speed transmission,

processing and storage of large volumes of

data, accessible to all organizations and

households;

use of predominantly domestic software by

state and local authorities.

Representatives of big business have begun to

actively implement digital technologies in their

companies' operations. Thus, in their 2018 integrated

reports, energy companies disclosed digitalization of

the business. For example, Atomenergomash JSC

started using digital technologies in industrial

production aimed at improving production efficiency,

developing remote servicing of manufactured

equipment, and carried out work on creating digital

products based on information systems for supporting

production processes, managing delivery times,

equipment quality control, personnel optimization

and equipment monitoring, technical documentation

management and several others. In the practical

activities of JSC Atomenergomash "a universal bar-

coding system is used, which allows automating the

process of entering information by users and

minimizing the influence of the human factor on the

correctness of the entered data. It is also possible to

fix in the information system the list of documents

required to form the technological passport

concerning the operation for pipeline valves. A

mechanism has been developed for the timely

submission of scanned copies of technological

passport documents. Control over the completeness

of the entered documents is set up. The process of

full-fledged electronic approval of technological

documentation at all stages - from development to

approval by the customer's representatives was

implemented".

In the State Research Centre Scientific Research

Institute of Atomic Reactors, to improve the

efficiency of the internal control and audit

department, an IT system was implemented, into

which information on the results of control activities

and audits conducted in the reporting period was

entered, based on which final reports were generated.

Enel Russi PJSC started using Big Data, applying

Agile approaches, which allowed responding faster to

the changes taking place. Unipro PJSC started using

Process Mining Technology, which made it possible

to identify and analyze actual business processes by

Impact of Non-financial Information on Digitalization of Business on the Sustainable Development of Russian Companies

275

extracting knowledge from event logs available in

modern information systems.

IDGC of Centre began to use the following types

of digital technologies in its operations:

Business Ontology (Ontological models of

activity): gradual digitalization (optimization)

of activities by core business processes of the

Company contributes to the reduction of the

cost of all business processes of the Company;

Digital Shadows: as part of the development of

online and offline decision support systems the

creation of mathematical models of networks,

objects, processes, etc. Contributes to reducing

operating costs and developing new business

for the company;

IoT (Industrial Internet of Things): significant

CAPEX and OPEX reductions for collecting

data from remote objects and devices on the

network, including a qualitative increase in this

data volume. Reducing operating costs and

developing new business for the Company;

Big Data: significant increase in transparency

of operations, qualitative saturation of online

and offline decision support systems with data.

Optimality of decision-making in the

operational and prospective environment.

Additional effects through common processing

of technological and corporate data;

Machine Learning: automated processing of

data sets within online and offline decision

support systems with appropriate mathematical

algorithms. Optimality of operational and

forward-looking decision-making;

Blockchain (Distributed registers): elimination

of intermediaries in the chain of electricity

sales to the end consumer, transition to

automated smart contracts, service

development for active consumers and

distributed energy. Development of new types

of services (business) of network companies

for market subjects.

Based on the above, we can conclude that large

Russian companies began to disclose data on the

digitalization of their operations in integrated

reporting even before the COVID-19 pandemic and,

accordingly, had a practice of working with them,

which cannot be said about medium and small

businesses, which felt the difficulties and challenges

of doing business particularly acutely during the

pandemic. They had to quickly and in an extremely

short period of time master and implement digital

technology into their operations to keep their business

running.

It can be said that it was the COVID-19 pandemic

that gave a powerful impetus to the digitalization of

small and medium-sized businesses and the rapid

adoption of digital technology in everyday life. This

has had a particular impact on the transformation of

the relationship between sellers and buyers, which

has become exclusively remote during the pandemic.

The digital transformation of market relations is

facilitating trade facilitation through digitalization as

well as the active use of e-commerce. During the

pandemic, new forms of market demand emerged: the

subscription model, the sharing economy, and

personalization. Thus, on the supply side of the

market, the Internet has enabled sellers to offer a

fairly wide range of goods and services at lower

prices, while increasing the space and time for which

a product is considered viable. Modern information

and communication technologies make it possible to

work out common managerial decisions, to transmit

meaningful visual information, which is necessary,

for example, in issues of operative managerial

decisions without direct contact. Almost everywhere

where there is no need for contact communication

with different customers, or buyers to carry out direct

and feedback, digital technologies are used to

produce a product or service and thereby continue to

operate businesses in the harsh environment of the

COVID-19 pandemic.

Based on the above, we can state that in the post-

virus economy, companies began to return to the

usual real interaction, but the public trust in digital

technology has remained and even increased. This is

why companies need to disclose digital data alongside

traditional non-financial information, which acts as a

competitive advantage to improve their investment

attractiveness in pursuit of sustainability.

5 CONCLUSIONS

In order to assess investment attractiveness,

companies need to generate structured information

that targets potential investors and can influence the

investment decision. In a post-virtual economy, in our

view, information about a company's digitalization is

key when making investment decisions. By

showcasing company digitalization information to

interested users in terms of the proposed areas,

companies will be able to disclose data not only about

the digital technologies available, the areas of

automation and digitalization of the company, but

also about how to manage and preserve them. As

digitalization promotes automation and the formation

of information bases containing confidential

ISSDRI 2021 - International Scientific and Practical Conference on Sustainable Development of Regional Infrastructure

276

information, to achieve maximum effect in improving

investment attractiveness, we recommend that

companies take decisive measures to enhance the

company's information security by keeping its

confidential information containing competitive

advantages. If confidential information is leaked, the

company may suffer irreparable damage, which can

lead to losses and sometimes bankruptcy, and,

consequently, to investors' losses. Therefore, by

disclosing information to interested users about a

company's digitalization and how to ensure its

cybersecurity, companies inspire users with greater

confidence in information about the company's

business continuity and continue the path and

direction of sustainable development.

REFERENCES

International Standard for Integrated Reporting. Electronic

resource, Rezhim dostupa

https://integratedreporting.org/wp-

content/uploads/2014/04/13-12-08-THE-

INTERNATIONAL-IR-FRAMEWORK.docx_en-

US_ru-RU.pdf

Integrirovannyy otchet AO Atomenergomash za 2018 god.

Electronic resource, Rezhim dostupa https://xn--

o1aabe.xn--p1ai/activity/social/registr/

Integrirovannyy otchet Gosudarstvennogo nauchnogo

tsentra Nauchno-issledovatel'skogo instituta atomnykh

reaktorov za 2018 god. Electronic resource, Rezhim

dostupa https://xn--o1aabe.xn--

p1ai/activity/social/registr/

Integrirovannyy otchet PAO Enel Rossiya za 2018 god.

Electronic resource, Rezhim dostupa https://xn--

o1aabe.xn--p1ai/activity/social/registr/

Integrirovannyy otchet PAO Yunipro za 2018 god.

Electronic resource, Rezhim dostupa https://xn--

o1aabe.xn--p1ai/activity/social/registr/

Integrirovannyy otchet PAO MRSK Tsentra za 2018 god.

Electronic resource, Rezhim dostupa https://xn--

o1aabe.xn--p1ai/activity/social/registr/

Konsul'tatsionnyy proyekt Mezhdunarodnykh osnov

integrirovannoy otchetnosti. Electronic resource,

Rezhim dostupa

https://integratedreporting.org/resource/consultationdr

aft2013/

Khakhonova, N. N., Kirkach, Yu. N., Koroleva, N. Yu.,

Agabekyan, S. G. (2020). Use of Evaluation Indicators

in the Composition of the Consolidated Financial

Statements in Digital Format of Economic Space. III

International Scientific and Practical Conference

"Digital Economy and Finances" (ISPC-DEF 2020),

vol.137.

Programma raboty po pokazatelyam (indikatoram)

ustoychivogo razvitiya. Electronic resource, Rezhim

dostupa

https://w.histrf.ru/articles/article/show/kontsieptsiia_us

toichivogo_razvitiia

Rukovodstvo po otchetnosti v oblasti ustoychivogo

razvitiya G4. Electronic resource, Rezhim dostupa

https://www.globalreporting.org/resourcelibrary/Russi

an-G4-Part-One.pdf

Impact of Non-financial Information on Digitalization of Business on the Sustainable Development of Russian Companies

277