On the Evaluation of Classification Methods Applied to Requests for

Revision of Registered Debts

Helton Souza Lima

1

, Damires Yluska de Souza Fernandes

1

, Thiago José Marques Moura

1

and Daniel Sabóia

2

1

Instituto Federal da Paraíba, 720 Avenida Primeiro de Maio, João Pessoa, Brazil

2

Procuradoria-Geral da Fazenda Nacional, Esplanada dos Ministérios Bloco P, Brasília, Brazil

Keywords: Government Data, Tax, Supervised Learning, Imbalanced Data.

Abstract: Tax management is a complex problem faced by governments around the world. In Brazil, in order to help

solving problems in this area, data analytics has been increasingly used to support and enhance tax

management processes. In this light, this work proposes an approach which uses supervised learning in order

to classify requests of an administrative service. The requests at hand are named as Requests for Revision of

Registered Debt (R3Ds). The service underlying such requests is offered by the Brazil’s National Treasury

Attorney-General's Office and usually deals with a high volume of registrations. The experimental evaluation

accomplished in this work presents some promising results. The obtained classification models present good

levels of accuracy, area under ROC curve and recall. Four evaluation scenarios have been experimented,

including imbalanced and balanced data. The Random Forest model achieves the best results in all the

evaluated scenarios.

1 INTRODUCTION

Failure to comply with tax obligations may have a

negative impact on the quality of life of citizens. This

is due to the fact that without tax revenue it is not

possible to maintain essential public services, such as

health services, sanitation, mobility, security,

education, among others (Mathews et al., 2018). Once

the legal deadline for paying a tax has expired, the

debt can be claimed by the government through the

Judiciary, i.e., by the system of courts of justice in a

country. Particularly in Brazil, according to the

country’s National Treasury Attorney-General's

Office (hereafter called as PGFN abbreviated from

“Procuradoria-Geral da Fazenda Nacional”), the

Federal Active Debt

1

(FAD), in early 2019,

accumulated 2.4 trillion reals (Brazilian currency),

from 4.9 million debtors

2

.

Brazilian tax enforcement processes take too long

and may have a low resolution rate. According to the

1

https://www.gov.br/pgfn/pt-br/assuntos/divida-ativa-

da-uniao

2

https://www.gov.br/pgfn/pt-br/acesso-a-informacao/

institucional/pgfn-em-numeros-2014/pgfn-em-

numeros-2020/view

Brazil’s National Council of Justice

3

, the average

processing time for a tax enforcement process is

usually about 8 years. These processes represent 39%

of total pending cases, and 70% of pending

executions, with a congestion rate of 87%. This

means, for instance that, in 2019, for every hundred

tax enforcement proceedings, only 13 of them were

closed. Thereby, debts usually reach the Judiciary

after the administrative means of collection are

exhausted, what implies in a hard task to recover their

tax.

In this context, Artificial Intelligence (AI)

techniques have been progressively used to support

and improve some Brazilian tax enforcement

processes (Souza and Siqueira, 2020). Specifically in

the area of tax justice, there is an initiative of the

National Council of Justice on using AI that aims to

reduce the time for the outcome of tax enforcement

processes

4

.

3

https://www.cnj.jus.br/wp-content/uploads/2020/

08/WEB-V3-Justi%C3%A7a-em-N%C3%Bame

ros-2020-atualizado-em-25-08-2020.pdf

4

https://www.cnj.jus.br/cnj-usara-automacao-e-inteli

gencia-artificial-para-destravar-execucao-fiscal/

Lima, H., Fernandes, D., Moura, T. and Sabóia, D.

On the Evaluation of Classification Methods Applied to Requests for Revision of Registered Debts.

DOI: 10.5220/0010498403350342

In Proceedings of the 23rd International Conference on Enterprise Information Systems (ICEIS 2021) - Volume 1, pages 335-342

ISBN: 978-989-758-509-8

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

335

The PGFN currently offers the Request for

Revision of Registered Debt

5

(hereafter called as

R3D), which is a service available since 2018. It is an

administrative claim, that allows taxpayers to request

a reanalysis of the situation of their debts registered

at FAD. It is an important way for reducing the rate

of new tax enforcement processes, aiming to avoid

the judicialization of erroneous processes. According

to the Federal Services Monitoring Panel

6

, R3D is the

most requested service in the light of the PGFN,

which highlights the high volume of requests to be

analyzed by the institution: approximately 44

thousands were registered in 2019, involving nearly

44 billions reals. Enhancing activities related to

administrative tax processes may lead to an increase

of tax recovery.

There is a dataset prepared by the PGFN that

includes a lot of information about R3Ds.

Understanding this dataset and analyzing it can

indeed generate important insights for the PGFN.

Particularly, classifying the likelihood of an R3D

being approved or rejected can help PGFN to improve

its processes and streamline results. Considering this,

the dataset is labeled with two possible classes:

approved R3D or rejected R3D. Nevertheless,it has

been realized that the two classes have a level of

imbalance that must be addressed.

With this scenario in mind, we define three main

problems that have guided this work, as follows: (i)

the need to indicate the likelihood for an R3D to be

approved or rejected based on the use of supervised

classification models; (ii) to evaluate some

supervised classification models regarding important

measures with respect to the context of this scenario

and (iii) to analyze strategies and apply some of them

to deal with the imbalance of existing classes.

Thus, historical data of the R3Ds are used to train

some supervised classification models. The five

generated models are evaluated with respect to the

measures Accuracy (ACC), Recall (REC) and area

under the ROC curve (AUC). To this end,

experimental scenarios have been defined taking into

account hold out and cross-validation strategies as

well as imbalanced versus balanced data. The results

obtained are promising and demonstrate good scores

for the evaluated metrics. In particular, the model

produced with the Random Forest method has

obtained the best measure scores. Regarding the use

of class balancing strategies, there has been no change

in relation to the results of the obtained models.

5

https://www.gov.br/pt-br/servicos/solicitar-revisao-

de-divida-inscrita

This paper is organized as follows: Section 2

provides some theoretical background; Section 3

describes some related works; Section 4 presents the

applied methodology; Section 5 discusses the results

which have been obtained, and Section 6 concludes

the paper and suggests some future work.

2 THEORETICAL

BACKGROUND

In this section, we provide some concepts regarding

the tax management business domain in our country

and also some principles with respect to Supervised

Learning.

2.1 Request for Revision of Registered

Debt

The Request for Revision of Registered Debt (R3D)

is an administrative claim that allows taxpayers to ask

for a reanalysis of the situation of their debts. It can

be used in cases of payment, instalment, suspension

of request under judicial decision, administrative

decision, judicial deposit, offset, correction of

statement, filling the statement inaccurately, formal

defect in the credit constitution, decay or prescription,

issues related to situations where the active debt

enrolment is prohibited and any extinction or

suspension cause of tax or non-tax debt.

Once the request for revision is granted, its

registration may be cancelled or rectified. The

demand for the debt may also be suspended. The task

of analysing and answering R3Ds is actually a time-

consuming task. Nowadays it is accomplished in

about 30 days. And it is completely human-

dependent.

2.2 Cross Industry Standard Process

for Data Mining

The Cross Industry Standard Process (CRISP-DM) is

a methodology which is usually used by data

scientists in order to ensure quality on knowledge

discovery project results (Chapman et al., 1999). The

process is tool-independent and can be used across

various business domains. It is based on iterative and

incremental principles.

In this light, in order to extract knowledge from

data of a given domain, the CRISP-DM guides data

6

http://painelservicos.servicos.gov.br/

ICEIS 2021 - 23rd International Conference on Enterprise Information Systems

336

scientists to (i) identify and give a solution to a

problem with the use of data mining techniques, (ii)

understand the underlying data and their

relationships, (iii) extract a suitable dataset, (iv)

create machine learning models in order to solve the

identified problem, (v) evaluate the performance of

the obtained new models, and (vi) demonstrate how

these models can be used and, eventually, be

deployed in the given business context. We use this

process in the light of our problem domain, i.e., with

respect to the R3D classification problem.

2.3 Supervised Learning

Machine Learning is an area of the Artificial

Intelligence (AI) whose objective is the construction

of systems capable of acquiring knowledge

automatically (Rezende, 2005). A subarea of

Machine Learning (ML), named Supervised

Learning, is composed of systems able to provide

predictions based on previous specific situations

stored on a dataset (Mitchell, 1997).

In supervised learning, one predictive task is

classification. Classification algorithms predicts

qualitative values, which will be assigned in

predefined categories (Mohri et al., 2018). In this

work, we deal with a two-class classification

problem, thus we aim to learn a class from its positive

and negative examples.

In the light of this work, an example (instance) is

positive in case of a rejected R3D (request). On the

other hand, negative examples regard accepted

requests. For two-class problems a variety of

performance measures has been proposed. For a

positive example, if the prediction is also positive,

this is a true positive (TP); if a prediction is negative

for a positive example, this represents a false negative

(FN). For a negative example, if the prediction is also

negative, we have a true negative (TN), and we have

a false positive (FP) if we predict a negative example

as positive (Alpaydin, 2010).

The measures used in this work are Accuracy

(ACC), Recall (REC) and Area Under Receiver

Operating Characteristic Curve (AUC). They are

defined in accordance with the following formulas

(Hossin and Sulaiman, 2015):

ACC = (TP + TN) / (TP + TN + FP + FN) (1)

REC = TP / (TP + FN) (2)

AUC is calculated through the plot of the

ROC curve, where the TPR is in y-axis and

the FPR is in x-axis

(3)

Some reasons for choosing such measures are

described as follows.

The Accuracy (ACC) measures the ratio of correct

predictions over the total number of instances

evaluated. Accuracy is the most used evaluation

measure in practice either for binary or multi-class

classification problems. It is easy to compute and easy

to understand by human (Hossin and Sulaiman,

2015).

In addition to accuracy, the AUC measure may be

used to present an overall view of a binary

classification model performance. It describes the

relationship between sensitivity (recall)

and specificity measures. The AUC has been proven

theoretically and empirically better than the accuracy

metric for evaluating some classifiers performance

(Huang and Ling, 2005; Alpaydin 2010).

One point that deserves attention is the cost

involved in making incorrect predictions: it is less

costly to predict a rejection when the request should

be accepted than to predict an approval when the

request should be rejected. In the dataset used in this

work, the positive value (1) indicates a rejected

request, and the negative value (0) indicates an

accepted one. This is the reason why the recall

measure (REC) is the most important (not

exclusively) one in the evaluation accomplished in

this work. Classifiers with a large recall don’t have a

high index of false negatives (Harrington, 2012).

The supervised classification methods used in this

work are Artificial Neural Networks (ANN), Naive

Bayes (NB), Random Forest (RF) and Support Vector

Machines (SVM). They are briefly described as

follows.

The Naive Bayes classifier is inspired by

Thomas Bayes Theorem. It estimates the

classification of new examples through a

probabilistic algorithm (Rish, 2001). It is called

“naïve” for making no assumption among the

classes.

Support Vector Machines classify data by

building a separating hyperplane to distinguish

and identify two types of different classes. To

this end, they determine points between two

domain universes, usually drawing a line (or

vector) and differentiating the data on both

sides (Gonzalez et al., 2005).

Artificial Neural Networks are models inspired

by the human brain. They are composed by a

net of interconnected units called Perceptrons

(Mitchell, 1997), which are organized in layers.

The network receives the training examples

and uses error functions to calculate weights in

order to maximize the correct prediction.

On the Evaluation of Classification Methods Applied to Requests for Revision of Registered Debts

337

Random Forests are a combination of decision

trees. Each tree has a different behaviour by the

effect of a randomly function applied in all

trees in the forest (Breiman, 2001). For every

classification, the majority vote of all trees

determines the models’ classification.

These methods have been chosen due to some

characteristics.

Regarding a NB classifier, one of the major

advantages is its short computational time for

training. NB provides the probability of an instance

to belong to a class, rather than simply providing a

classification (Kotsiantis et al., 2007). This is an

information that must add value to the prosecutor’s

decision. Thus, it is desirable to be achieved in our

approach.

The SVM method has been considered interesting

since it usually fits the available data well without

overfitting (Bhavsar and Panchal, 2012).

With respect to ANNs, they outperform other

methods in many different business domains (Paliwal

and Kumar, 2009). One of the important advantages

of this method is that it can automatically

approximate any nonlinear mathematical function.

This aspect is useful when the relationship among the

variables is not known.

Random forests are fast and easy to implement.

They produce highly accurate predictions and can

handle a very large number of input variables without

overfitting (Biau, 2012). They can also provide the

most important variables of the dataset considered for

the model. They can be useful on a future

dimensionality reduction task.

Another usual issue in classification tasks regards

imbalanced classes. A two-class dataset is said to be

imbalanced when one minority class is under-

represented with regard to the majority class

(Japkowicz and Stephen, 2002). The application of

re-sampling techniques to obtain a more balanced

data distribution is an effective solution to the

imbalanced class problem (He and Ma, 2013).

Among a diverse set of re-sampling methods, we

briefly describe the two ones used in this work:

Random Undersampling and SMOTE. The former

removes a random set of majority class examples. It

is one of the simplest re-sampling approaches.

Although it can eliminate useful examples, it requires

less computational effort (Branco et al., 2016). The

latter, which means Synthetic Minority Oversampling

TEchnique, over-samples the minority class by

generating new artificial data. The synthetic data are

created using an interpolation strategy that introduces

a new example along the line segment joining a seed

example and a user-defined number of nearest

neighbours (Chawla et al., 2002);

These methods have been used and evaluated in

several related works (Branco et al., 2016).

3 RELATED WORKS

In this section, we briefly resume some relevant and

related work which applies machine learning in the

data domain of tax management.

One of the works regards classifying companies

as contumacious tax debtors or not (Soares and

Cunha, 2020). In this work, the dataset used was built

from a data warehouse system of a brazilian city. The

work aimed to help tax auditors on prioritizing the

taxpayers that have higher risks of service tax default.

They evaluated LightGBM, Logistic Regression and

Random Forest models with respect to accuracy and

AUC measures. Results were considered better than

their previous work.

The work of Dias and Becker (2017) conducted a

study to classify invoices as potential audit candidates

or not. It used data extracted from the electronic

invoice system of Porto Alegre city finance secretary,

in Brazil. Results were considered as promising since

they presented a high precision rate using the SVM

method.

Another related work aimed to help decision-

making in government taxes audit plans by using

historical data from previous audits (Ippolito and

Lozano, 2020). It tried to predict service tax crimes

against the tax system of the city of São Paulo, Brazil.

The target variable contained the information whether

the taxpayer committed a crime against tax system or

not, in previous tax audits. Six algorithms were

applied: Neural Networks, Naive Bayes, Decision

Trees, Logistic Regression, Random Forest and

Ensemble Learning. Random Forest yielded the

highest scores in the majority of the performance

metrics utilized.

López et al., (2019) used data from the Spanish

Revenue Office, with the goal of identifying

taxpayers who evade tax. Their study applied Neural

Networks and reached a good level of correct

predictions.

Another recent work proposed a customized loss

function, assigned to a social cost, to evaluate the

performance of some models (Battiston et al., 2020).

The proposition was validated through the use of a

dataset provided by the Italian Revenue Agency, with

information of income tax of more than 600 thousand

individuals over 5 years. The Random Forest model

ICEIS 2021 - 23rd International Conference on Enterprise Information Systems

338

was considered the best classifier, achieving the

lowest value for the defined loss function.

Silva et al., (2015) worked on building predictive

models on the results of specific claims in a tax

administration process in the Brazilian Federal

Revenue (BFR). This is the most similar work to ours.

It classified credit compensation requests as

“granted” or “rejected”. The dataset included

information built from several transactional and

analytical BFR’s systems. Random Forest was

identified as the algorithm selected for the

deployment phase with the argument that it was more

accurate in the most important class: it is less costly

to predict a rejection when the request should be

granted than to predict a grant when the request

should be dismissed.

Comparing these works with ours, some different

aspects are identified as follows. One aspect is that,

differently from the works of López et al., (2019) and

Battiston et al., (2020), this work does not deal with

fraud detection. Another aspect is that our work deals

with historical data filled with manual analysis in

order to label the target variable. It is not set by

specific automatic business rules like the ones of two

brazilian cities (Soares and Cunha, 2020; Dias and

Becker, 2017). The third aspect is that this is the first

work that deals with this PGFN’s specific dataset,

with its own characteristics and business rules. For

example, the size of the dataset, with 70.780 cases is

significantly bigger than the 151 cases of tax crime

detection presented in Ippolito and Lozano (2020).

Other example regards the fact that the dataset used

in this work represents all regions of Brazil and not

only one specific jurisdiction such as the work of

Silva et al., (2015). Futhermore this work observes

the effects of class balancing methods on the

performance of the models, and none of the related

works registered this observation.

4 METHODOLOGY

In the following subsections we present details on

how the steps of the CRISP-DM methodology is

applied in this work. The steps applied are: Business

Understanding, Data understanding, Data

preparation, Modelling and Evaluation.

4.1 Business Understanding and

Research Questions Definitions

This initial phase focuses on understanding the

business objectives and is used to define some

research questions. The PGFN’s business main

objectives are to improve taxpayer assistance and also

to increase tax recovery. In order to help achieving

these objectives, our approach has been specified to

assist decision-making of analysts of the Requests for

Revision of Registered Debts. Thereby, there should

be an increase of the assertiveness of the requests’

results as well as a decrease of the response time of

the requests answering.

With this scenario in mind, besides que questions

presented in Section 1, some additional ones are

included as follows:

Q1 - In order to allow a better understanding of

the factors that influence decisions, what are

the main statistics, relationships, and

correlations between the variables?

Q2 - Are there any anomalies or unexpected

behaviours that require attention from the

central administration?

4.2 Data Understanding

We have collected the dataset from the PGFN. The

dataset has been created by a team composed of

domain experts and systems analysts, that gathered

data from several PGFN data sources, including

transactional and analytical systems. The available

historical data of the R3Ds have been included, by

considering the period of November 2018 and June

2020.

The dataset has 23 independent variables and a

total amount of 70.780 R3Ds instances, containing a

nationwide representation. Personal or business

identification information and any other variable

considered as sensitive were disregarded.

The independent variables regard the following

information: (i) the request itself; (ii) the taxpayer;

(iii) some of the taxpayer’s relationship in the real

world; (iv) information describing the debt (e.g.,

value, age, type, and situation); and (iv) some history

of actions and situations associated with PGFN

processes. The dataset also contains the analysis

result of the request, i.e., the dependent variable

indicating approval or rejection. For the sake of

security and confidentiality, details regarding the

variables are not mentioned in this work.

Each variable was analysed with respect to its

main statistics, in order to observe the data

distribution, maximum and minimum values,

existence of outliers, temporal distribution and

correlation with other variables. Tasks concerned

with cleaning or transformation were verified and

executed to assure a better model creation. Despite

these issues, no missing values were detected, and no

outliers were removed.

On the Evaluation of Classification Methods Applied to Requests for Revision of Registered Debts

339

With respect to the target variable, the dataset has

a 70/30% proportion between the two classes. Even

though it’s not a strong imbalance problem, we

decided to apply some re-sampling techniques in

order to observe the behaviour of the classification

methods.

4.3 Data Preparation

The data preparation phase usually covers all

activities to construct the final dataset from the

collected data. The transformations made to the data

involved the following actions:

A normalization of all data in a standard scale

between 0 and 1.

Two pairs of variables presented a correlation

coefficient equals to 1, i.e., they presented the

same values for every dataset example. Since

this situation was not expected, one variable of

each pair was removed.

4.4 Modelling and Evaluation

In the modelling step, the classification models are

created according to four experimental scenarios. For

each scenario, the measures evaluated are Accuracy

(ACC), AUC and Recall (REC).

The classification methods which have been

applied are: Neural Networks, Naive Bayes, Random

Forest and Support Vector Machines. All the models

are trained using the default parameters from SciKit-

Learn library. These parameters are as follows::

Multilayer Perceptron: activation=’relu’,

hidden_layer_sizes=(100,100),

learning_rate=’constant’, max_iter=4000,

solver=’adam’, and tol=0.0001.

GaussianNB: priors=’None’, and

var_smoothing=’1e-09’.

Random Forest: bootstrap=True,

criterion=’gini’, min_samples_leaf=1,

min_samples_split=2, and n_estimators=100.

SVC: C=1.0, cache_size=200,

decision_function shape=’ovr’, degree=3,

kernel=’rbf’, shrinking=True, and tol=0.001.

The first scenario of the modelling step is a

random stratified hold-out, using 80% of the available

data for the training set and 20% for the test set.

The second scenario is built considering a 10-fold

cross-validation, using the stratified shuffle split

method. It is defined, for every iteration, the same

80% of the available data for the training set and 20%

for the test set.

In the third scenario, we include balancing

methods. Thus, at this one, a 10-fold cross-validation

is executed applying a Random Undersampling class

balancing method at each iteration. In the fourth

scenario, a 10-fold cross-validation is executed

applying the SMOTE technique at each iteration.

5 RESULTS AND DISCUSSION

The Data Understanding step brings some results, by

means of answering the questions defined at the

Business Understanding step (Section 4.1). Thus, in

order to answer Q1, the correlation matrix has been

plotted. It shows low correlation among most of the

variables, except for two pairs of variables that

presented a correlation coefficient equals to 1. One

variable of each pair has been removed due to such

high correlation.

In order to answer Q2, through some statistical

analysis, it is possible to identify some anomalies.

One of them regards 110 registered debts in a peculiar

situation: each one of them is composed by more than

20 requests. This situation shows a possibility of

using a R3D service just to postpone the debt’s

payment. Therefore, it requires attention from the

central administration to better evaluate cases like

that.

In the Modelling and Evaluation steps, the results

obtained in the first scenario (random hold-out) are

presented in Table 1. The highest scores for each

measure are presented in bold. The first scenario

brings these results: The Random Forest model

showed the highest ACC and AUC among the

evaluated models, followed by Neural Networks,

SVM and Naive Bayes. Regarding REC, the SVM

achieved a slightly (only 1%) higher rate than the

Random Forest.

Table 1: Random stratified hold-out results.

Classifier ACC AUC REC

Neural Networks 81% 88% 84%

Naive Bayes 60% 72% 49%

Random Forest

88% 94%

92%

SVM 69% 72%

93%

The results obtained in the second, third and

fourth scenarios are presented in Table 2, including

the mean and standard deviation obtained for each

metric. The results after applying the class balancing

techniques are presented with an arrow up when the

measure has more than one percent of variation.

ICEIS 2021 - 23rd International Conference on Enterprise Information Systems

340

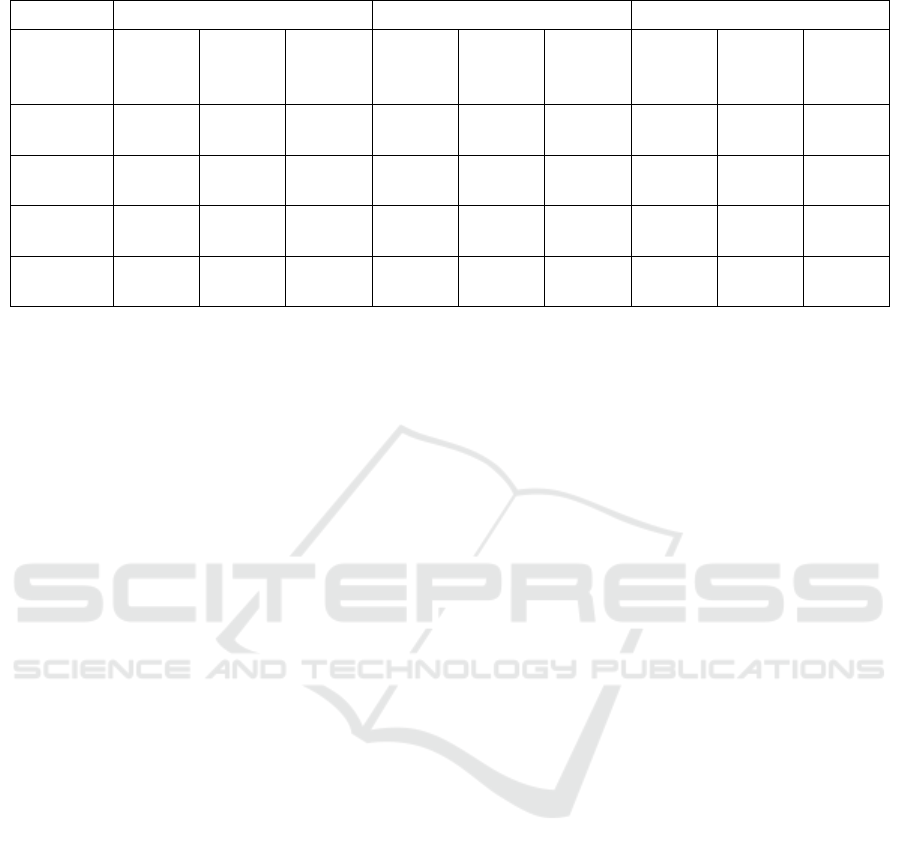

Table 2: Results before and after applying class balancing methods in 10-fold cross-validation scenarios.

Unbalanced Scenario After Under Sampling After SMOTE

Classifier

Mean

(Std Dev)

ACC

Mean

(Std Dev)

AUC

Mean

(Std Dev)

REC

Mean

(Std Dev)

ACC

Mean

(Std Dev)

AUC

Mean

(Std Dev)

REC

Mean

(Std Dev)

ACC

Mean

(Std Dev)

AUC

Mean

(Std Dev)

REC

Neural

Networks

82%

(±0,4%)

89%

(±0,4%)

87%

(±2,5%)

79% ↓

(±0,9%)

88%

(±0,3%)

78% ↓

(±4,4%)

81%

(±0,7%)

89%

(±0,4%)

82% ↓

(±2,3%)

Naive Bayes

58%

(±1,4%)

71%

(±0,3%)

45%

(±3,6%)

55% ↓

(±2,6%)

71%

(±0,3%)

38% ↓

(±5,8%)

53%

(±1,3%)

71%

(±0,3%)

33% ↓

(±2,8%)

Random

Forest

88%

(±0,3%)

95%

(±0,2%)

92%

(±0,2%)

87%

(±0,4%)

94%

(±0,2%)

87% ↓

(±0,5%)

88%

(±0,3%)

94%

(±0,2%)

91%

(±0,3%)

SVM

70%

(±0,6%)

71%

(±0,4%)

92%

(±2,3%)

66% ↓

(±2,6%)

72%

(±0,5%)

65% ↓

(±8,5%)

64% ↓

(±1,8%)

72%

(±0,4%)

60% ↓

(±6,3%)

The second scenario (cross-validation with

unbalanced data) confirms Random Forest with

higher scores of ACC, AUC and REC, followed by

the same order of models presented in the first

scenario. Although SVM presented a lower ACC

comparing to Neural Networks, it has a higher REC,

and can be considered a better estimator to this study.

The third and fourth scenarios show that the

application of Random Under Sampling and SMOTE

techniques decreased the ACC and REC. It can be

explained that, in both techniques, there is an increase

on the representation of the negative class. The

negative class is the minority class in this work. Then,

the models tend to increase the predictions on this

class, and the number of False Negatives and True

Negatives also increase. Consequently, it may

decrease ACC and REC. Weiss and Provost (2003)

concluded that, when ACC is the priority

performance measure, the best class distribution for

learning tends to be near the natural class distribution,

and when AUC is the priority performance metric, the

best class distribution for learning tends to be near the

balanced class distribution. With respect to standard

deviations, the application of class balancing

techniques did not cause significant changes.

6 CONCLUSIONS AND FUTURE

WORK

This work has presented an approach to predict if

R3Ds should be accepted or rejected. The evaluation

of the created classification models indicates

promising results mainly with regards to the Random

Forest model. It achieves the best performance in

terms of the most important measures considered in

this work (ACC, AUC and REC). Cross-validation

strategies have been used and show that the Random

Forest model performs a good generalization. The

class balancing techniques employed in this work do

not improve the models’ performance. This is due to

the kinds of data we deal with, i.e., increasing the

number of false negatives cases is costly than

increasing the number of false positives cases.

The solution provided by this work may be useful

to support decisions of the prosecutor who registers

the result of a request application. It may not only

increase the decision assertiveness but also decrease

the response time.

As future work we point out some tasks to be

done: (i) to experiment different hyper-parameters for

the algorithms with the best performances (Random

Forest and Neural Networks); (ii) to apply XGBoost

method or other one evaluated with good

performance on financial data (Pugliese et al., 2020);

(iii) to reduce the number of variables used in training

models, and then checking the impact of them on the

observed created models; and (iv) to deploy the

classification model which best fits the real PGFN

scenario.

REFERENCES

Alpaydin, E. (2010). Introduction to machine learning.

MIT press.

Battiston, P., Gamba, S., and Santoro, A. (2020).

Optimizing Tax Administration Policies with Machine

Learning. University of Milan Bicocca Department of

Economics, Management and Statistics Working Paper,

(436).

Bhavsar, H., and Panchal, M. H. (2012). A review on

support vector machine for data classification.

International Journal of Advanced Research in

Computer Engineering & Technology (IJARCET),

1(10), 185-189.

On the Evaluation of Classification Methods Applied to Requests for Revision of Registered Debts

341

Biau, G. (2012). Analysis of a random forests model. The

Journal of Machine Learning Research, 13(1), 1063-

1095.

Branco, P., Torgo, L., and Ribeiro, R. P. (2016). A survey

of predictive modeling on imbalanced domains. ACM

Computing Surveys (CSUR), 49(2), 1-50.

Breiman, L. (2001). Random forests. Machine learning,

45(1), 5-32.

Chapman, P., Clinton, J., Kerber, R., Khabaza, T., Reinartz,

T., Shearer, C., and Wirth, R. (1999). The CRISP-DM

user guide. In 4th CRISP-DM SIG Workshop in

Brussels in March (Vol. 1999).

Chawla, N. V., Bowyer, K. W., Hall, L. O., and

Kegelmeyer, W. P. (2002). SMOTE: synthetic minority

over-sampling technique. Journal of artificial

intelligence research, 16, 321-357.

Dias, M., and Becker, K. (2017). Identificação de

Candidatos à Fiscalização por Evasão do Tributo ISS.

In Proceeding of the 5

th

Symposium on Knowledge

Discovery, Mining and Learning.

Gonzalez, L., Angulo, C., Velasco, F., and Catala, A.

(2005). Unified dual for bi-class SVM approaches.

Pattern Recognition, 38(10), 1772-1774.

Harrington, P. (2012). Machine learning in action.

Manning Publications.

He, H., and Ma, Y. (2013). Imbalanced learning:

foundations, algorithms, and applications. John Wiley

& Sons.

Hossin, M. and Sulaiman, M. N. (2015). A review on

evaluation metrics for data classification evaluations. In

International Journal of Data Mining and Knowledge

Management Process.

Huang, J., and Ling, C. X. (2005). Using AUC and accuracy

in evaluating learning algorithms. IEEE Transactions

on knowledge and Data Engineering, 17(3), 299-310.

Ippolito, A., and Lozano, A. C. G. (2020). Tax Crime

Prediction with Machine Learning: A Case Study in the

Municipality of São Paulo. In 22

nd

International

Conference on Enterprise Information Systems (pp.

452-459).

Japkowicz, N., and Stephen, S. (2002). The class imbalance

problem: A systematic study. Intelligent data analysis,

6(5), 429-449.

Kotsiantis, S. B., Zaharakis, I., and Pintelas, P. (2007).

Supervised machine learning: A review of

classification techniques. Emerging artificial

intelligence applications in computer engineering,

160(1), 3-24.

López, C. P., Rodríguez, M. J. R., and Santos, S. L. (2019).

Tax fraud detection through neural networks: an

application using a sample of personal income

taxpayers. Future Internet, 11(4), 86.

Mathews, J., Mehta, P., Kuchibhotla, S., Bisht, D.,

Chintapalli, S. B., and Rao, S. K. V. (2018). Regression

analysis towards estimating tax evasion in Goods and

Services Tax. In 2018 IEEE/WIC/ACM International

Conference on Web Intelligence (WI) (pp. 758-761).

IEEE.

Mitchell, T. M. (1997). Machine Learning. McGraw-Hill,

1st edition.

Mohri, M., Rostamizadeh, A., and Talwalkar, A. (2018).

Foundations of machine learning. MIT press.

Paliwal, M., and Kumar, U. A. (2009). Neural networks and

statistical techniques: A review of applications. Expert

systems with applications, 36(1), 2-17.

Pugliese, V. U., Hirata, C. M., and Costa, R. D. (2020).

Comparing Supervised Classification Methods for

Financial Domain Problems. In 22nd International

Conference on Enterprise Information Systems (pp.

440-451).

Rish, I. (2001). An empirical study of the naive Bayes

classifier. In IJCAI 2001 workshop on empirical

methods in artificial intelligence (Vol. 3, No. 22, pp.

41-46).

Rezende, S. O. (2005). Sistemas inteligentes: fundamentos

e aplicações. 1. ed. Editora Manole.

Russel, S., and Norvig, P. (2013). Artificial intelligence: a

modern approach. Pearson Education Limited.

Silva, L. S., Carvalho, R. N., and Souza, J. C. F. (2015).

Predictive models on tax refund claims-essays of data

mining in brazilian tax administration. In International

Conference on Electronic Government and the

Information Systems Perspective (pp. 220-228).

Springer, Cham.

Soares, G. V.; Cunha, R. C. L. V. (2020). Predição de

Irregularidade Fiscal dos Contribuintes do Tributo ISS.

In: Anais do Simpósio Brasileiro de Banco de Dados.

Souza, K. L. C. M. and Siqueira, M. (2020). A inteligência

artificial na execução fiscal brasileira: limites e

possibilidades. In Revista de Direitos Fundamentais e

Tributação, Volume 1, n. 3, p. 17-44, 2020.

Weiss, G. M., and Provost, F. (2003). Learning when

training data are costly: The effect of class distribution

on tree induction. In Journal of artificial intelligence

research, 19, 315-354.

Wirth, R., and Hipp, J. (2000). CRISP-DM: Towards a

standard process model for data mining. In Proceedings

of the 4th international conference on the practical

applications of knowledge discovery and data mining

(pp. 29-39). London, UK: Springer-Verlag.

ICEIS 2021 - 23rd International Conference on Enterprise Information Systems

342