Swiss Francs Seem to Make Insured Move: Comparing Daily and

Monthly Financial Incentives of a Scalable Digital Health

Intervention

Gisbert W. Teepe

1a

and Tobias Kowatsch

1,2 b

1

Center for Digital Health Interventions, ETH Zürich, Zürich, Switzerland

2

Institute of Technology Management, University of St. Gallen, St. Gallen, Switzerland

Keywords: Observational Field Study, Physical Activity, Digital Health Intervention, Financial Incentives.

Abstract: Despite the widely known necessity to counteract the increase in physical inactivity, only small strides have

been achieved so far. Digital health interventions (DHIs) are proposed to reach both healthy and at-risk

populations on a large scale. However, designing scalable DHIs that are engaging in the long term remains a

challenge. Small financial incentives may help to achieve such long-lasting behaviour changes. This work

thusly investigates the effects of daily or monthly paid small financial incentives on step counts and goal

achievements in physical activity. Six-month observational field data of a physical activity DHI (PADHI),

offered by a Swiss health insurer, was used for this investigation. From 1623 contacted customers, 742

(45.7%) joined the PADHI. Step counts and times the challenging goal was reached were significantly higher

in the condition of daily paid incentives. The findings from objectively measure daily step counts and goal

achievements indicate better outcomes when incentives are paid daily. Further findings indicate the

importance of recording various physical activities and not only step counts.

1 INTRODUCTION

Despite various attempts and approaches, physical

inactivity remains an immense problem as a health

risk factor. At least 20% of the world’s population is

insufficiently active and doesn’t meet the

recommended 150 minutes of moderate-intensity or

75 minutes of vigorous-intensity aerobic physical

activity (PA) per week (Sallis et al., 2016). Findings

from further studies underline the necessity to

promote PA. These findings show that PA decreases

the risk of mortality (Lear et al., 2017), the risk of

noncommunicable diseases such as diabetes, cancer

or coronary heart diseases (Kyu et al., 2016; Lee et

al., 2012,), and the cox hazard ratio of cardiovascular

events and fractures (Harris et al., 2019). Western

societies are increasingly becoming older. One

problem of this demographic change is that older

people tend to suffer longer and more frequently from

sicknesses and chronic diseases. Therefore, a cost

a

https://orcid.org/0000-0002-2264-9797

b

https://orcid.org/0000-0001-5939-4145

increase in healthcare is imminent making affordable

and scalable changes in healthcare inevitable.

One frequently discussed solution is the use of

digital health interventions (DHI) delivered via

smartphones, wearable devices, or websites

(Kowatsch, Otto, Harperink, Cotti, & Schlieter,

2019). They inform individuals about their current

health condition and are capable of delivering

personalized interventions to the masses at low costs

(Steinhubl, Muse, & Topol, 2015; Troiano et al.,

2008).

However, reaching vulnerable individuals that

would most benefit from DHIs remains a key

challenge. This selection bias is even higher when

participation is voluntary and not "prescribed" by a

doctor (Chinn, White, Howel, Harland, &

Drinkwater, 2006). Furthermore, the maintenance of

these behaviour adjustments for a substantial amount

of time poses a difficult challenge (Finkelstein et al.,

2016).

A promising approach to attract and maintain

participation in DHIs is the use of financial

Teepe, G. and Kowatsch, T.

Swiss Francs Seem to Make Insured Move: Comparing Daily and Monthly Financial Incentives of a Scalable Digital Health Intervention.

DOI: 10.5220/0009396308270833

In Proceedings of the 13th International Joint Conference on Biomedical Engineering Systems and Technologies (BIOSTEC 2020) - Volume 5: HEALTHINF, pages 827-833

ISBN: 978-989-758-398-8; ISSN: 2184-4305

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

827

incentives. Studies using relatively large incentive

values of an average maximum amount of $ 20.75 per

week seem to effectively change the amount of PA

(Strohacker, Galarraga, & Williams, 2014). These

relatively high incentives improved different

objective measures of PA (Barte & Wendel-Vos,

2017), the number of times PA exercises attended

(Barte & Wendel-Vos, 2017; Mitchell et al., 2013;

Strohacker et al., 2014), and exercise behaviour

(Mitchell et al., 2013).

Unfortunately, different studies show that after

withdrawing incentives, the PA changes typically do

not sustain and therefore need to be paid over a long

time (Finkelstein et al., 2016; Harkins, Kullgren,

Bellamy, Karlawish, & Glanz, 2017; Patel, Asch,

Rosin, Small, Bellamy, Eberbach, et al., 2016; Patel,

Asch, Rosin, Small, Bellamy, Heuer, et al., 2016;

Patel et al., 2018). To provide these necessary

financial incentives on a large scale and for a long

time, a crucial feature would be to keep them

relatively small (Kramer, Tinschert, Scholz, Fleisch,

& Kowatsch, 2019). Relatively small financial

incentives having a significant impact on PA were

around $1 per day (Patel, Asch, Rosin, Small,

Bellamy, Heuer, et al., 2016; Shin et al., 2017;

Strohacker et al., 2015). In a cluster-randomized trial

study, small personal or charity financial incentives

(monthly payment between CHF 5.00 to 10.00) led to

an increase of PA (Kramer et al., 2019). Surprisingly,

participation and reached step goals declined even

while the study was running and incentives not yet

withdrawn. The authors argue that incentives may

need to be modified to counter this decline in

participation and achieve lasting changes in

behaviour. Accordingly, prior studies (Barte &

Wendel-Vos, 2017; Strohacker et al., 2014) showed

relatively stable effects as long as the participants

received financial incentives.

Against this background, this study aims to

propose and discuss different incentives schemes for

physical activity digital health interventions

(PADHIs). The research question of this study is

whether a small daily paid incentive or a small

monthly paid incentive leads to an improvement in

daily steps, daily step goal achievements, and a

attrition rate reduction.

The next section describes the characteristics of

the study population and the evaluated PADHI. We

then describe the methods of data analysis to answer

the research question. Afterwards, results of the six-

month observational field study are presented and

discussed. A summary concludes this paper.

2 METHOD

We cooperated with a large Swiss health insurer to

answer the research question. The insurer started to

offer a PADHI to their customers in 2015 (Kramer et

al., 2019). In the last quarter of 2018, an average of

10.530 (SD = 5547) daily steps were achieved by

13799 customers. Compared to all other self-service

health promotion interventions of the insurance this

PADHI has the most continuous users. Data for the 6-

month study of the current paper was collected from

a subset of these customers between April 1

st

and

September 30

th

2016.

Participants, that already participated in a

previous study by Kramer et al. (2019) were invited

by e-mail. Participants were required to be at least 18

years old, enrolled in the complimentary insurance

program (see Section 2.2 below), and had to accept

the terms of participation and privacy policy.

Furthermore, they had to confirm that they were not

under any medical treatment that forbid PA. Although

no eligibility criteria were defined on the canton

(federal state of Switzerland) state-level, all

participants that provided demographic information

resided in a German-speaking canton. In the

invitation text, a brief description of the initiative and

a link to the insurer’s platform with more detailed

information was provided. On the linked platform the

participants signed up and were asked to complete a

survey to collect demographic data such as gender,

age, and level of activity. In total 1632 individuals

that already participated in a previous study by

Kramer et al. (2019) were contacted for recruitment.

The institutional review board of the University of

St. Gallen, Switzerland, approved the study (HSG-

EC-2016-06-13-A).

2.1 Incentive Schemes

Participants received financial incentives if they

reached specific daily step goals. For the first three

months, participants received a monthly payment if

they reached the daily step goal averaged over the

entire month. They received CHF 10.00 if the average

daily step of the month was above 10000 steps or

received CHF 5.00 if they achieved at least 7500 steps

per day but didn’t reach the goal of 10000 steps per

day. Participants with an average daily step count

below 7500 didn’t receive any financial incentive.

After three months the incentive scheme was

changed. The participants received daily payments

for three months if they reached the same goals as

defined above. Participants reaching at least 10000

steps per day received a payment of CHF 0.40 on that

Scale-IT-up 2020 - Workshop on Best Practices for Scaling-Up Digital Innovations in Healthcare

828

day. Participants reaching 7500 steps per day but not

10000 steps per day received CHF 0.20 on that day.

Table 1 shows the paid financial incentives by the

goal that was achieved and the incentive scheme. Due

to these different financial schemes for the first and

last three months, all participants could earn a total

amount between CHF 33.00 and CHF 66.00

depending on their performance within each of the

parts.

Table 1: Incentive mechanisms of the evaluated PADHI.

Averaged

Daily Steps

Monthly Payment

(Apr-Jun)

Daily Payment

(Jul-Sep)

< 7500 CHF 0.00 CHF 0.00

7500 – 10000 CHF 5.00 CHF 0.20

> 10000 CHF 10.00

CHF 0.40

For two weeks after the first three months, no

financial incentive was paid. This break arose due to

a technical problem by switching from monthly to

daily payments, leading to no steps being recorded

within those two weeks. Unfortunately, this break

resulted in different amounts of data points for further

analysis. To address this, only the first 76 days within

every three months of the study were used for further

analysis.

2.2 Study Sample

Due to legal reasons, the PADHI could not be part of

the statutory health insurance program. It could only

be offered to insureds with a complimentary

insurance plan. It is important to take into

consideration, that 75% of the Swiss population is

enrolled in such an insurance plan (Eisler & Lüber,

2016).

2.3 Measures and Statistical Analysis

Participants recorded their daily steps via commercial

pedometers offered by Garmin, Jawbone, or Fitbit, or

a specific smartphone app by Fitbit. The app option

was offered because buying a compatible pedometer,

although at a reimbursed price, was the most cited

reason for non-participation (41%) of participants

that did not want to participate in a prior study by

Kramer et al. (2019). Demographic data were in

addition to the data from the pedometer measured via

a self-report questionnaire.

From the provided data the average daily step

count, the number of days the app was used, the last

day the app was used, and the dropout rate were

calculated. Depended two-tailed t-tests with and α-

level of 0.05 to compare the average daily step count,

and the number of days the 10000 or 7500 goal was

reached within each of the different financial

incentive scheme were used for statistical analysis.

For the initial description and some analyses, all

participants, that used the app at least once and had an

average step count that did not exceed four standard

deviations from the mean, were included. Average

step counts exceeding four standard deviations from

the mean were considered a technical fault or

personal manipulation. For further analyses,

participants not providing data for at least 150 days of

the study were excluded. This is corresponding to

non-participation of more than one month.

Participants were marked as a dropout if they

provided no data for at least one week and did not

provide any further data afterwards at any point until

the end of the study. These dropouts were still

included in the analysis as they provided at least 150

days of data, which can be considered to be sufficient

in the remaining window of time (Guertler,

Vandelanotte, Kirwan, & Duncan, 2015).

The effect of the two different incentive schemes

on the number of goals achieved was calculated by a

four-field Chi-Square Test, with an α-level of 0.05.

3 RESULTS

From initially 1632 contacted insurance members 742

(45.5%) signed up and provided at least one day of

data. Of these only one participant exceeded the mean

number of steps by four standard deviations, leaving

741 (45.4%) participants that met this criterion. Data

for at least 150 days was provided by 392 (24.0%)

participants. Table 2 compares the number of

participants and the dropout rate for all participants

and those providing at least 150 days of data. Except

the initial attrition considering the number of people

that were contacted, the dropout rate within the study

was 174 (23.5%) for the participants that used the app

at least once and 10 (2.6%) for the participants that

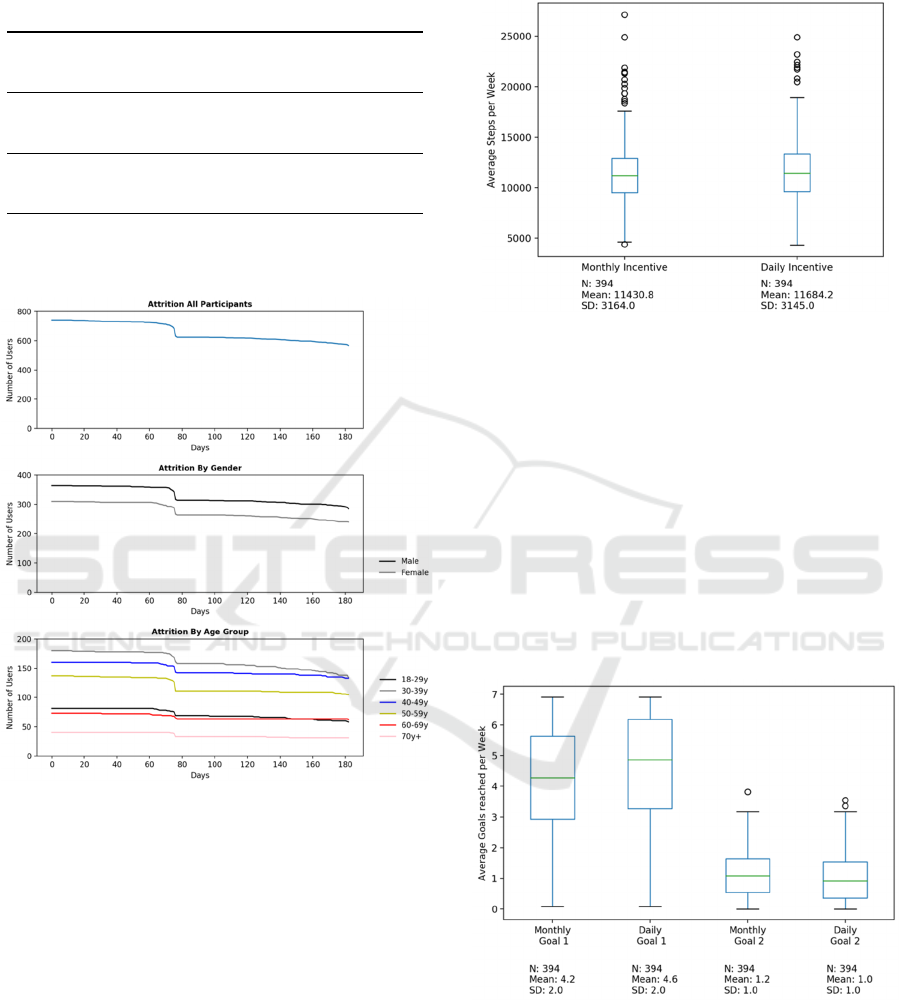

provided at least 150 days of data. Figure 1 shows the

attrition rate for all participants of the study and the

attrition rate for all participants of the study by gender

and age groups.

The following descriptions are for the 392

participants included in the analysis. Demographic

data was provided by 371 (94.6%) participants, 207

(55.8%) being males. The mean age was 46.4 (SD =

13.8) ranging from 21 to 92 years. An overview of the

analysed measures and their distribution are reported

in Figures 2 for averaged daily steps and Figure 3 for

reached goals within each financial incentive scheme.

Swiss Francs Seem to Make Insured Move: Comparing Daily and Monthly Financial Incentives of a Scalable Digital Health Intervention

829

Table 2: Number (#) and attrition of participants.

Used DHI at

least once

Used DHI at

least 150 days

# participants at start

741

(54.5%)

392

(76%)

# participants after three

months

631

(14.8%)

392

(0%)

# participants after

incentive change

623

(15.9%)

392

(0%)

# participants after six

months (end of study)

567

(23.5%)

382

(2.6%)

Figure 1: Attrition for all participants that used the PADHI

and attrition for all participants that used the DHI by gender

or age.

There was a highly significant increase of average

daily step data from the monthly incentive payments

(M = 11552.8, SD = 2962.6) to the daily incentive

payments (M = 11971.9, SD = 3047.1), t(391) = 4.85,

p < .001. A significant increase from the average days

per week the 10000-step goals reached from the

monthly incentive payment (M = 4.1, SD = 1.8) to the

daily incentive payments (M = 4.6, SD = 1.8) was

observed, t(391) = 7.48, p < .001. The average

number of days per week the 7500-step goal was

reached significantly decreased from the monthly

incentive payments (M = 1.2, SD = 0.8) to the daily

incentive payments (M = 1.0, SD = 0.8), t(391) =

5.27, p < .001.

Figure 2: Distribution of weekly averaged steps counts by

financial incentive scheme.

The number of days the 10000 daily step goal was

reached significantly differed by which incentive

scheme was used, X

2

(1, N = 50270) = 167.9, p < .01.

The daily incentive scheme displays more days the

more challenging goal was reached (19739 number of

days for daily incentives vs 17973 for monthly

incentives). The number of days the 7500 daily step

goal was reached did not significantly differ by which

incentive scheme was used, X

2

(1, N = 21863) = 0.8,

p = .39. Figure 4 illustrates the number of days the

different goals were reached and the days the goals

were not reached.

Figure 3: Distribution of Weekly Averaged Reached Goals

by the financial incentive scheme (Goal 1 = 10000 daily

steps reached, Goal 2 = 7500 daily steps reached).

Scale-IT-up 2020 - Workshop on Best Practices for Scaling-Up Digital Innovations in Healthcare

830

Figure 4: Times the 10000 daily step goal, the 7500 daily

step goal, or no goal was reached by the incentive scheme.

4 DISCUSSION

This study investigates the effect of different financial

incentive schemes (monthly vs. daily payments) on

attrition, PA (measured by the number of steps), and

goal achievements of a large scale PADHI.

The percentage of people responding to the initial

recruitment was fairly good (45.5%). It is important

to take into consideration that participants were

recruited from a previous study investigating the effect

of DHIs. The number of participants that provided

sufficient data (at least 150 days of data) to be analysed

is in contrast low. Only 14% of the initially contacted

1623 participants met this criterion.

In contrast, within the 6-months of the study, the

attrition rate was very low compared to the prior work

by Kramer et al. (2019). Interestingly the two weeks

of no financial activity had almost no drop-out effect.

The attrition rate of the group that provided at least

150 days of data was only 2.6%. This finding could

be important for future work as it shows that frequent

users once engaged seem to consistently interact with

the DHI regardless of a break in the payment of the

financial incentive.

The results from analysing the average daily steps

made, the average number of times the more

challenging 10000 steps goal was reached per week,

and the total number of days the more challenging

10000 steps goal was reached seem to favour the daily

paid incentive. Only the average number of days per

week the less challenging 7500 steps goal was

reached seems to favour the monthly paid incentives.

The analysis revealed no significant difference for the

total amount of days the less challenging 7500 steps

goal was achieved. Due to the fact, that the number of

days the 10000 daily step goal was reached, was

higher over both financial incentive schemes it seems

that participants either aim high and in turn achieve

the higher goal or do not try to reach a goal and in turn

do not achieve any goal at all. For further research, it

could be interesting to investigate whether providing

only one goal has a positive effect due to the reduction

of the complexity or if more but very challenging

goals have a positive influence on PA and continuous

participation. Both approaches could be supported by

the theory of implementation intentions (Gollwitzer,

1999) stating that goals should be specific and

challenging. Taken this tendency to reach the higher

goal and the average steps made per week into

account the results suggest that a daily financial

incentive seems to have a positive effect on the

number of steps for every day.

The findings of the current work are limited in

several ways. First, it can be assumed that the

contacted individuals are already relatively active due

to the fact, that they participated in an earlier study

that investigated the use of DHI as well and that

voluntary PA initiatives, in general, tend to attract

people that are already sufficiently active and show

health-supportive behaviour.

Second, the findings of the current work may be

country or at least region-specific. It is, therefore,

possible that other countries are less or more open to

the use of tracking devices and digital coaching

applications.

Finally, causal inferences cannot be drawn from the

current study due to the nature of the observational

study design. Therefore, the results are limited in their

generalizability. They rather give interesting insights

into possible future studies investigating the differen-

ces between monthly and daily financial incentive

schemes that have the goal to increase physical.

5 SUMMARY

Relatively small daily paid financial incentives (CH

0.20 – 0.40) seem to lead to higher daily steps counts

compared to relatively small monthly paid financial

incentives (CH 5.00 – 10.00). Participants seemed to

aim for the higher goal or not bother to reach any goal

at all on that specific day. Future work should investi-

gate the importance of setting clear but ambitious

goals and financial incentives to further promote PA.

ACKNOWLEDGEMENTS

The authors would like to thank Jan-Niklas Kramer

and the two anonymous reviewers for their valuable

support and comments.

Swiss Francs Seem to Make Insured Move: Comparing Daily and Monthly Financial Incentives of a Scalable Digital Health Intervention

831

REFERENCES

Barte, J. C. M., & Wendel-Vos, G. C. W. (2017). A

Systematic Review of Financial Incentives for Physical

Activity: The Effects on Physical Activity and Related

Outcomes. Behavioral Medicine, 43(2), 79-90.

doi:10.1080/08964289.2015.1074880

Chinn, D. J., White, M., Howel, D., Harland, J. O. E., &

Drinkwater, C. K. (2006). Factors associated with non-

participation in a physical activity promotion trial.

Public Health, 120(4), 309-319. doi:10.1016/j.puhe.

2005.11.003

Eisler, R., & Lüber, A. (2016). Wie wichtig ist den

schweizern eine spitalzusatz- versicherung? . Retrieved

from www.comparis.ch/»/media/files/medien-corner/

studies/2006/krankenkassen/spitalzusatzversicherunge

n_studie.pdf.

Finkelstein, E. A., Haaland, B. A., Bilger, M.,

Sahasranaman, A., Sloan, R. A., Nang, E. E. K., &

Evenson, K. R. (2016). Effectiveness of activity

trackers with and without incentives to increase

physical activity (TRIPPA): a randomised controlled

trial. The Lancet Diabetes & Endocrinology, 4(12),

983-995. doi:10.1016/S2213-8587(16)30284-4

Gollwitzer, P. M. (1999). Implementation intentions: strong

effects of simple plans. American psychologist, 54(7),

493.

Guertler, D., Vandelanotte, C., Kirwan, M., & Duncan, M.

J. (2015). Engagement and Nonusage Attrition With a

Free Physical Activity Promotion Program: The Case

of 10,000 Steps Australia. Journal of Medical Internet

Research, 17(7), e176. doi:10.2196/jmir.4339

Harkins, K. A., Kullgren, J. T., Bellamy, S. L., Karlawish,

J., & Glanz, K. (2017). A Trial of Financial and Social

Incentives to Increase Older Adults’ Walking.

American Journal of Preventive Medicine, 52(5), e123-

e130. doi:10.1016/j.amepre.2016.11.011

Harris, T., Limb, E. S., Hosking, F., Carey, I., Dewilde, S.,

Furness, C., Cook, D. G. (2019). Effect of pedometer-

based walking interventions on long-term health

outcomes: Prospective 4-year follow-up of two

randomised controlled trials using routine primary care

data. PLOS Medicine, 16(6), e1002836.

doi:10.1371/journal.pmed.1002836

Kowatsch, T., Otto, L., Harperink, S., Cotti, A., & Schlieter,

H. (2019). A design and evaluation framework for digital

health interventions. it - Information Technology, 61(5-

6), 253-263. doi:10.1515/itit-2019-0019

Kramer, J. N., Tinschert, P., Scholz, U., Fleisch, E., &

Kowatsch, T. (2019). A Cluster-Randomized Trial on

Small Incentives to Promote Physical Activity. Am J

Prev Med, 56(2), e45-e54. doi:10.1016/j.amepre.

2018.09.018

Kyu, H. H., Bachman, V. F., Alexander, L. T., Mumford, J.

E., Afshin, A., Estep, K., Forouzanfar, M. H. (2016).

Physical activity and risk of breast cancer, colon cancer,

diabetes, ischemic heart disease, and ischemic stroke

events: systematic review and dose-response meta-

analysis for the Global Burden of Disease Study 2013.

BMJ, i3857. doi:10.1136/bmj.i3857

Lear, S. A., Hu, W., Rangarajan, S., Gasevic, D., Leong, D.,

Iqbal, R., Yusuf, S. (2017). The effect of physical

activity on mortality and cardiovascular disease in

130 000 people from 17 high-income, middle-income,

and low-income countries: the PURE study. The

Lancet, 390(10113), 2643-2654. doi:10.1016/s0140-

6736(17)31634-3

Lee, I. M., Shiroma, E. J., Lobelo, F., Puska, P., Blair, S.

N., & Katzmarzyk, P. T. (2012). Effect of physical

inactivity on major non-communicable diseases

worldwide: an analysis of burden of disease and life

expectancy. The Lancet, 380(9838), 219-229.

doi:10.1016/s0140-6736(12)61031-9

Mitchell, M. S., Goodman, J. M., Alter, D. A., John, L. K.,

Oh, P. I., Pakosh, M. T., & Faulkner, G. E. (2013).

Financial Incentives for Exercise Adherence in Adults.

American Journal of Preventive Medicine, 45(5), 658-

667. doi:10.1016/j.amepre.2013.06.017

Patel, M. S., Asch, D. A., Rosin, R., Small, D. S., Bellamy,

S. L., Eberbach, K., Volpp, K. G. (2016). Individual

Versus Team-Based Financial Incentives to Increase

Physical Activity: A Randomized, Controlled Trial.

Journal of General Internal Medicine, 31(7), 746-754.

doi:10.1007/s11606-016-3627-0

Patel, M. S., Asch, D. A., Rosin, R., Small, D. S., Bellamy,

S. L., Heuer, J., Volpp, K. G. (2016). Framing Financial

Incentives to Increase Physical Activity Among

Overweight and Obese Adults: A Randomized,

Controlled Trial. Annals of Internal Medicine, 164(6),

385-394. doi:10.7326/m15-1635

Patel, M. S., Volpp, K. G., Rosin, R., Bellamy, S. L., Small,

D. S., Heuer, J., Asch, D. A. (2018). A Randomized,

Controlled Trial of Lottery-Based Financial Incentives

to Increase Physical Activity Among Overweight and

Obese Adults. American Journal of Health Promotion,

32(7), 1568-1575. doi:10.1177/0890117118758932

Sallis, J. F., Bull, F., Guthold, R., Heath, G. W., Inoue, S.,

Kelly, P., Hallal, P. C. (2016). Progress in physical

activity over the Olympic quadrennium. The Lancet,

388(10051), 1325-1336. doi:10.1016/s0140-6736(16)

30581-5

Shin, D. W., Yun, J. M., Shin, J.-H., Kwon, H., Min, H. Y.,

Joh, H.-K., Cho, B. (2017). Enhancing physical activity

and reducing obesity through smartcare and financial

incentives: A pilot randomized trial. Obesity, 25(2),

302-310. doi:10.1002/oby.21731

Steinhubl, S. R., Muse, E. D., & Topol, E. J. (2015). The

emerging field of mobile health. Science Translational

Medicine, 7(283), 283rv283-283rv283. doi:10.1126/

scitranslmed.aaa3487

Strohacker, K., Galárraga, O., Emerson, J., Fricchione, S.,

Lohse, M., & Williams, D. (2015). Impact of Small

Monetary Incentives on Exercise in University

Students. American Journal of Health Behavior, 39.

doi:10.5993/AJHB.39.6.5

Strohacker, K., Galarraga, O., & Williams, D. M. (2014).

The Impact of Incentives on Exercise Behavior: A

Systematic Review of Randomized Controlled Trials.

Annals of Behavioral Medicine, 48(1), 92-99.

doi:10.1007/s12160-013-9577-4

Scale-IT-up 2020 - Workshop on Best Practices for Scaling-Up Digital Innovations in Healthcare

832

Troiano, R. P., Berrigan, D., Dodd, K. W., Masse, L. C.,

Tilert, T., & McDowell, M. (2008). Physical activity in

the United States measured by accelerometer. Med Sci

Sports Exerc, 40(1), 181-188. doi:10.1249/mss.0b013e

31815a51b3

Swiss Francs Seem to Make Insured Move: Comparing Daily and Monthly Financial Incentives of a Scalable Digital Health Intervention

833