Model-centered Ensemble for Anomaly Detection in Time Series

Erick L. Trentini, Ticiana L. Coelho da Silva, Leopoldo Melo Junior and Jose F. de Macêdo

Insight Data Science Lab, Fortaleza, Brazil

Keywords:

Time Series, Anomaly Detection, Ensemble.

Abstract:

Time-series anomalies detection is a fast-growing area of study, due to the exponential growth of new data

produced by sensors in many different contexts as the Internet of Things (IOT). Many predictive models have

been proposed, and they provide promising results in differentiating normal and anomalous points in a time-

series. In this paper, we aim to find and combine the best models on detecting anomalous time series, so

that their different strategies or parameters can contribute to the time series analysis. We propose TSPME-AD

(stands for Time Series Prediction Model Ensemble for Anomaly Detection). TSPME-AD is a model-centered

based ensemble that trains some of the state-of-the-art predictive models with different hyper-parameters and

combines their anomaly scores with a weighted function. The efficacy of our proposal was demonstrated in

two real-world time-series datasets, power demand, and electrocardiogram.

1 INTRODUCTION

Stock market prices, sleep monitoring, trajectories of

moving objects are real-world data commonly regis-

tered taking into account some notion of time. When

collected together, the measurements compose what

is known as a time series.

Collecting vast volumes of time series data opens

up new opportunities to discover hidden patterns. As

an example, doctors can be interested in searching for

anomalies in the sleep patterns of a patient. In the mo-

bility data domain, for instance, a new interest in tra-

jectory anomaly research has occurred, which can be

integrated with navigation to provide dynamic routes

for drivers or travelers. Besides, this research can pro-

vide accurate real-time advisor routes compared with

navigation based on static traffic information. An-

other application is for taxi companies that may ob-

serve drivers with traveling trajectories that are dif-

ferent from the popular choices of other drivers and

detect fraudulent behavior.

There is a range of different approaches that ad-

dress the problem of anomaly detection on time se-

ries. Several techniques can be applied to per-

form such tasks using predictive models, clustering-

based methods, distance-based methods, among oth-

ers (Meng et al., 2018). However, detecting anoma-

lies in sequence learning tasks become challeng-

ing using standard approaches based on mathemati-

cal models that rely on stationarity (Malhotra et al.,

2016). The state-of-the-art has been investigating

LSTM neural networks (Hochreiter and Schmidhu-

ber, 1997) to overcome these limitations and to model

the normal behavior of a time series, then accurately

detect deviations from normal behaviour without any

pre-specified threshold or preprocessing phase (Mal-

hotra et al., 2015; Malhotra et al., 2016).

In this paper, we follow a similar idea. We use

some predictors, based on LSTM neural network to

model normal behavior, and subsequently, use the

prediction errors to identify anomalies. These net-

work models are data-hungry techniques and require

a massive amount of training data. We profit from the

fact that there are a plethora of instances of normal

behavior than anomalous to employ these techniques.

The intuition behind is that the network model would

only have seen instances of normal behavior during

training and the model can reconstruct them. When

given an anomalous time series, it may not be able

to rebuild it properly, and it would end up with higher

reconstruction errors than for non-anomalous time se-

ries.

We propose TSPME-AD (stands for Time Series

Prediction Model Ensemble for Anomaly Detection).

TSPME-AD combines two state-of-the-art detection

models (Malhotra et al., 2016; Malhotra et al., 2015)

to derive a combined decision. Various classifier com-

bination schemes have been devised and it has been

experimentally demonstrated that some of them con-

sistently outperform a single best classifier (Kittler

700

Trentini, E., Coelho da Silva, T., Melo Junior, L. and F. de MacÃłdo, J.

Model-centered Ensemble for Anomaly Detection in Time Series.

DOI: 10.5220/0008985507000707

In Proceedings of the 12th International Conference on Agents and Artificial Intelligence (ICAART 2020) - Volume 2, pages 700-707

ISBN: 978-989-758-395-7; ISSN: 2184-433X

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

et al., 1996). In the experimental section, we prove

that by using an ensemble of such classifiers, the final

model improves in terms of F-measure on detecting

anomalous behavior.

This paper investigates a challenging problem

since the anomaly detection is performed on multi-

variate time series data. As discussed in (Wang et al.,

2018), anomalies may occur in only a subset of di-

mensions (variables). Another drawback is the loca-

tions and lengths of anomalous sub-sequences may be

different in different dimensions. Third, the anoma-

lous time series may look normal in each dimension

individually, but their combinations may be anoma-

lous.

The remainder of the paper is structured as fol-

lows: Section 2 introduces formally the problem

statement. Section 3 presents the preliminary con-

cepts to understand our approach. Section 4 presents

our proposal. Section 5 presents the related works.

Section 6 discusses the experimental evaluation, and

finally Section 7 draws the final conclusions.

2 PROBLEM STATEMENT

Consider a multivariate time series X =

[x

(1)

, x

(2)

, . . . , x

(n)

] such that x

(i)

∈ R

m

is a m-

dimensional vector x

(i)

= [x

(i)

1

, x

(i)

2

, . . . , x

(i)

m

] at

time t = i. Usually, the predictive models seek

to predict the next point given a time series.

That is, for a predictive model M and a time

series X = [x

(1)

, x

(2)

, . . . , x

(n)

], M(x

(i)

) = x

(i+1)

.

Some models may differ from this perspective,

such as predicting more than one data point,

M(x

(i)

) = [x

(i+1)

, x

(i+2)

], or re-building the time-

series backwards M(x

(i)

) = x

(i−1)

.

Given a predictive model M and a time series X,

Y = M(X ) is the predicted sequence of X using M

such that Y = [y

(1)

, y

(2)

, . . . , y

(n)

], and y

(i)

is the at-

tempt from M to build x

(i)

. Our goal is to reconstruct

the sequence X , compute the prediction errors based

on the prediction M(x

(i)

) compared to x

i

, compute

the anomaly scores (using the error distribution) and

identify the anomalies on X.

3 PRELIMINARIES

This section discusses the network architectures used

by our approach introduced in (Malhotra et al., 2015;

Malhotra et al., 2016). Our proposal is an ensemble

model that combines both strategies.

3.1 Stacked LSTM

Consider two sets of time series: s

N

for training the

prediction model M and v

N

for validating M. Let

s

N

= [s

(1)

N

, s

(2)

N

, . . . , s

(n)

N

] such that s

(i)

N

∈ R

m

is a m-

dimensional vector s

(i)

N

= [s

(i)

N

1

, s

(i)

N

2

, . . . , s

(i)

N

m

] at time

t = i. The same applies for v

N

.

For s

(i)

N

, each one of the m dimensions (s

(i)

N

∈ R

m

)

is taken by one unit in the input layer, and there is one

unit in the output layer for each of the l future predic-

tions for each of the m dimension. The LSTM units in

a hidden layer are fully connected through recurrent

connections. (Malhotra et al., 2015) stacks LSTM

layers such that each unit in a lower LSTM hidden

layer is fully connected to each unit in the LSTM

hidden layer above it through feedforward connec-

tions. Figure 1 shows the Stacked LSTM architec-

ture. The prediction model M is learned using the

non-anomalous training sequence s

N

.

Input

Layer

LSTM LSTM

Output

Layer

Figure 1: Stacked LSTM model as proposed by (Malhotra

et al., 2015).

Consider X a set of time series, and a predic-

tion length of l, each of the selected d dimensions

of x

(t)

∈ X for l < t ≤ n − l is predicted l times.

Error vectors are computed for each x

(t)

such that

e

(t)

= [e

(t)

11

, . . . , e

(t)

1l

, . . . , e

(t)

d1

, . . . , e

(t)

dl

] where e

(t)

i j

is the

difference between x

(t)

i

and the value predicted by the

model M at time t − j. In (Malhotra et al., 2015),

the prediction model trained on s

N

is used to com-

pute the error vectors for each point in the validation

and test sequences. The error vectors are modelled

to fit a multivariate Gaussian distribution N (µ, Σ) .

The validation set is used to estimate µ and Σ us-

ing Maximum Likelihood Estimation. The anomaly

score p

(t)

of an error vector e

(t)

is given by the value

of N at e

(t)

, in other words, p

(t)

is computed as

(e

(t)

− µ)

T

Σ

(−1)

(e

(t)

− µ) for an observation x

(t)

. For

x

(t)

, the value predicted is considered as anomalous if

the p

(t)

> τ, else it is classified as normal. The value

of τ is learned using v

N

by maximizing F1-score (con-

sidering a classification problem where that anoma-

lous points belong to a class and normal points to an-

other class).

3.2 Encoder Decoder Model

The network architecture discussed in this section

is composed of an LSTM-based encoder that learns

Model-centered Ensemble for Anomaly Detection in Time Series

701

fixed-length vector representation of the input time-

series. And an LSTM-based decoder that uses this

representation to reconstruct the time-series using the

current hidden state and the value predicted at the pre-

vious time-step. The network architecture was pro-

posed in (Malhotra et al., 2016) and it is illustrated in

Figure 2.

LSTM

Decoder

LSTM

Encoder

h

1

h

2

h

3

x

1

x

2

x

3

x'

1

x'

2

x'

3

h

4

x

4

h'

1

h'

2

h'

3

h'

4

Initialize with

internal state

x'

4

Input

Output

Figure 2: Encoder-Decoder model as proposed by (Malho-

tra et al., 2016).

In general, by using Encoder Decoder architec-

ture, the representation is learned from the entire

sequence which is then used to reconstruct the se-

quence. This is different from usual prediction based

anomaly detection models. Given s

N

for training the

prediction model M, h

(i)

E

is the hidden state of encoder

at time t

i

for each i ∈ {1, 2, ..., n} where h

(i)

E

∈ R

c

,

c is the number of LSTM units in the hidden layer

of the encoder. The encoder and decoder are jointly

trained to reconstruct the time series in reverse order

as {s

(n)

N

, s

(n−1)

N

, . . . , s

(1)

N

}. The final state h

(n)

E

of the

encoder is used as the initial state for the decoder.

A linear layer on top of the LSTM decoder layer is

used to predict the target. During the decoding phase,

the decoder uses s

(i)

N

and the internal state h

(i−1)

D

to

predict s‘

(i−1)

N

corresponding to target s

(i−1)

N

. Let s

N

be a set of normal training sequences, the encoder

decoder model is trained to minimize the objective

∑

s

(i)

N

∈ s

N

∑

n

i=1

s

(i)

N

− s‘

(i)

N

2

.

For an observation, x

(t)

, the anomaly score p

(t)

in

(Malhotra et al., 2016) is computed similarly as ex-

plained in the last section by modeling the error vec-

tors to fit a Multivariate Gaussian distribution. The

next section discusses our approach.

4 TSPME-AD: TIME SERIES

PREDICTION MODEL

ENSEMBLE FOR ANOMALY

DETECTION

In this paper, we combine the models (Malhotra

et al., 2015; Malhotra et al., 2016) using a model-

centered ensemble technique that attempts to com-

bine the anomaly score from both models built on the

same dataset. However, there exist some challenges

in the combination process. According to (Aggarwal,

2013), the main issues are normalization and com-

bination. The former corresponds to the problem of

different models may output anomaly scores not eas-

ily comparable. The latter is the problem of deciding

which combination function is the best (the minimum,

the maximum or the average). These are still open

questions, according to (Aggarwal, 2013), the liter-

ature on outlier ensemble analysis is very sparse so

the solutions for these mentioned issues are not com-

pletely known.

To address the first issue, a damping function is

applied to the anomaly scores, in order to prevent it

from being dominated by a few components (Aggar-

wal, 2013). Examples of a damping function could

be the square root or the logarithm. The second issue

is addressed in this paper by using a weighted aver-

age on the damped scores, that can be trained using

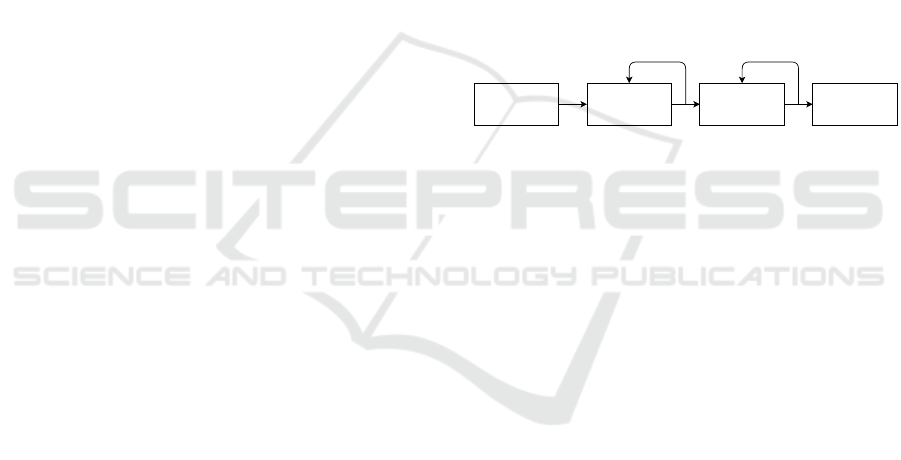

some sort of optimization algorithm. Figure 3 gives

an overview of the TSPME-AD pipe to construct the

model.

To construct the ensemble, we first calculate the

anomaly scores for each model in our ensemble as

in Figure 4, then we use a damping function on all

anomaly scores as in Figure 5, and aggregate each

set of scores using the weighted average function as

shown in Figure 6. In the experiments, we show

that the damped weighted average function (used

by TSPME-AD) performs better than the ensemble

model using the logarithm as a damping function.

With our new aggregated set of anomaly scores, we

try to find a threshold that maximizes some desired

score on the validation set as exemplified in Figure 7.

For a time series X , let the anomaly score a

i

∈

R and b

i

∈ R be computed from the prediction value

outputted by the models (Malhotra et al., 2015) and

(Malhotra et al., 2016), respectively. Our approach

uses the combination function shown in Equation 1 to

compute the anomaly score ∀x

i

∈ X :

A

i

=

w

(1)

× lna

i

+ w

(2)

× lnb

i

w

(1)

+ w

(2)

(1)

We say that x

i

is anomalous if

A

i

> τ

where τ is learned as one of the weights.

The weights w

(1)

, w

(2)

and τ are learned from the

validation set v

N

during the training phase, with w

1

,

w

2

∈ [0, 1] and τ ∈ R. And the goal is to maximize the

F1-score.

ICAART 2020 - 12th International Conference on Agents and Artificial Intelligence

702

Calculate anomaly

scores for each model

Use a damping function

on the anomaly scores

Aggregate all scores

using a weighted

average function

Set a threshold and

calculate some score

like F

1

Optimize weights and

thresholdto maximize

said score

Figure 3: The full pipe of TSPME-AD.

a

1

a

2

a

p

...

M

1

...

M

1

M

1

Figure 4: First, all models try to reconstruct the time series,

and we calculate the anomaly scores.

In this paper, we focus on the combination of the

models proposed by (Malhotra et al., 2015) and (Mal-

hotra et al., 2016), but the combination function can

be extended to any number of models with their re-

spective variations of hyper-parameters, and can be

generalized as in Equation 2.

A

i

=

w

(1)

× ln a

(1)

i

+ w

(2)

× ln a

(2)

i

+ · · · + w

(p)

× ln a

(p)

i

w

(1)

+ w

(2)

+ · · · + w

(p)

(2)

In Equation 2, p is the number of different mod-

els used to reconstruct the time series. From the au-

thors’ knowledge, none of the previous work that pro-

a

1

a

2

a

p

...

da

1

da

2

da

p

...

ln(x) ln(x) ln(x)

Figure 5: Applying a damping function to all anomaly

scores. e.g. the natural log function.

poses model-centered outlier ensemble models uses

this function or an LSTM based approach for outliers

detection (Aggarwal, 2013; Liu et al., 2012).

5 RELATED WORK

Anomaly detection models in time series have been

investigated by using machine learning and statistical

approaches as discussed in (Chandola et al., 2009).

Besides the aforementioned techniques, a new one

which is recently gaining momentum is deep learn-

ing and generally used to deal with non-linear mod-

els. However, only a few studies consider deep neural

networks for resolving outlier detection. (Kieu et al.,

2018) proposes an outlier detection framework to

identify an anomaly in multidimensional time-series

data. The framework incorporates several deep neu-

ral network-based autoencoders. The idea behind us-

ing autoencoders is they likely to fail to reconstruct

outliers using small feature space. Therefore, devia-

tions between the original input data and the recon-

structed data can be taken as indicators of outliers.

The paper (Malhotra et al., 2016) proposes an LSTM

encoder-decoder architecture that is trained to recon-

struct instances of normal behavior. When given an

anomalous time series, it may not be able to rebuild it

properly. Another paper that follows the same idea is

(Malhotra et al., 2015), however, the model proposed

stacks LSTM networks. Both paper (Malhotra et al.,

2015; Malhotra et al., 2016) solves the same prob-

lem than this approach, however, we gather the best

of both papers by combining them to derive a com-

bined decision.

da

1

da

2

da

p

...

A

W

1

W

2

W

p

Figure 6: Aggregating all sets of anomaly scores using a

weighted average function.

Model-centered Ensemble for Anomaly Detection in Time Series

703

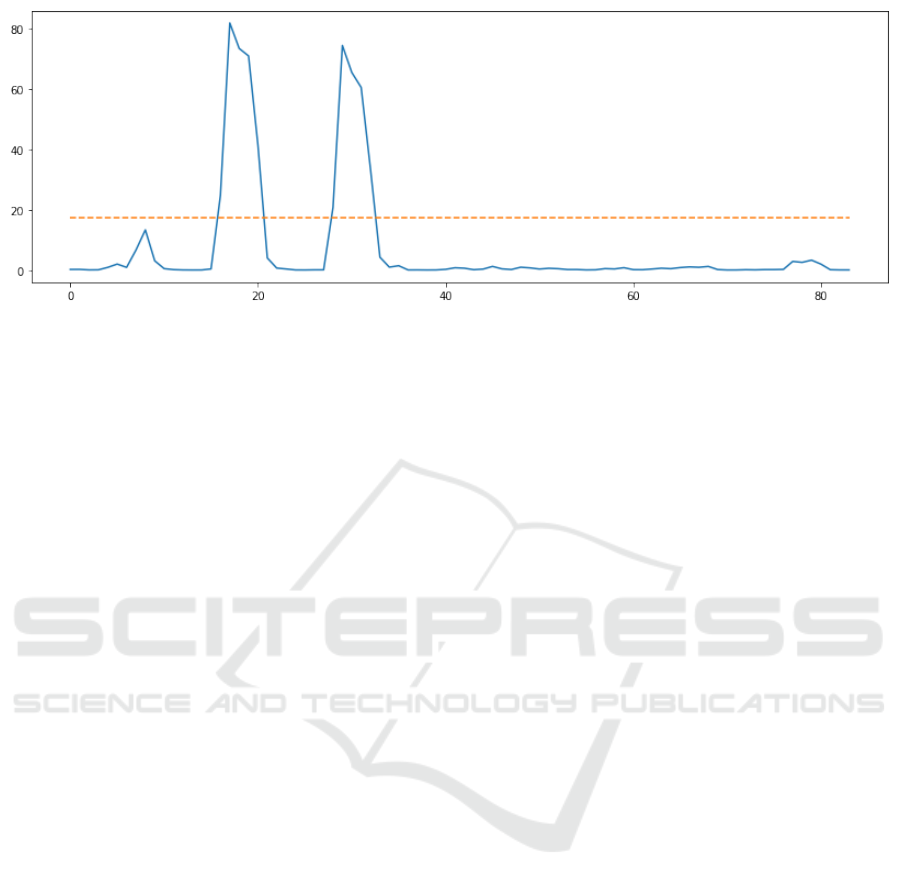

Figure 7: Setting a threshold to discriminate between ’normal’ and anomalous points.

The approach proposed in (Kong et al., 2018) can

detect long-term traffic anomaly with crowdsourced

bus trajectory data. The time series segments are ex-

tracted from bus trajectory data to describe the whole

city traffic situation from both temporal and spatial

aspects. (Kong et al., 2018) extracts the average ve-

locity and average stop time which can describe traf-

fic conditions and travel demand respectively. Then

(Kong et al., 2018) excavates poor segments which

are the bottleneck of traveling in one line by cal-

culating their anomaly index. The approach (Tariq

et al., 2019) proposes an anomaly detector for a satel-

lite system using a multivariate Convolutional LSTM

combined with a complementary Mixtures of Proba-

bilistic Principal Component Analyzer. The proposed

model learns from a large amount of normal teleme-

try data, it predicts between normal and abnormal

telemetry sequence.

Another type of anomaly detection algorithms

uses clustering techniques. Paper (Wang et al., 2018)

proposes a clustering algorithm that discretizes the

time series data into time windows, and clusters all

subsequences within each window. Univariate sub-

sequences in the same cluster within a window are

similar to each other. The behavior patterns of ob-

jects are obtained by the cluster centers, and if a time

series does not follow such behavior it is anomalous.

For multivariate time series, the algorithm transforms

the original time series into a new feature space in

which each feature is the distance to a pattern. The

smaller the distance, the more similar the data is to

the pattern. (Wang et al., 2018) performs clustering

on the transformed data, and assign anomaly score to

each time series based on the clustering results and

distances to normal cluster. Other clustered based ap-

proaches for anomaly detection are (Gao et al., 2012;

Iverson, 2004).

The main difference between TSPME-AD and

the previous one is a model-centered based approach

that uses a damped averaging function to combine

the best of the state-of-the-art detection models to

derive a combined decision. There exist few simi-

lar approaches that propose an ensemble model for

anomaly detection (Aggarwal, 2013) as (Liu et al.,

2012; Gao and Tan, 2006). However, none of these

approaches models normal behavior by profiting of

LSTM neural networks for multidimensional time se-

ries.

6 EXPERIMENTS AND RESULTS

In this section, we conduct some experiments with

two real-world datasets and report the precision, re-

call, F

1

and F

0.1

scores for TSPME-AD and the base-

line models (Malhotra et al., 2015; Malhotra et al.,

2016). We also study different combination functions

to ensemble the baseline models.

6.1 Experimental Setup

We split the dataset into 4 groups, s

n

, v

n

, v

a

, t

a

, where

s

n

and v

n

consist of a set of the time-series without

anomalies, and the other two groups (v

a

and t

a

) are

the remaining with at least one anomaly each.

We trained the models with s

n

using v

n

for early

stopping. Also, the training set (s

n

and v

n

) were used

to generate the error distribution, and then to calculate

the anomaly scores of the models.

We used the set v

a

to train the weights of the com-

bination function and the threshold τ. Finally, with

the set t

a

we calculated the anomaly scores and com-

pared TSPME-AD with the baseline models.

6.1.1 Competitors

For the stacked LSTM model, we implemented an

LSTM network with 30 and 20 LSTM nodes on the

ICAART 2020 - 12th International Conference on Agents and Artificial Intelligence

704

first and second hidden layers respectively, using the

Sigmoid activation function for the hidden layers, and

a linear activation for the output.

Since the Stacked LSTM presents as a hyper-

parameter, the number of points ahead to predict at

each step. In these experiments, we varied as 2, 4, 8

and 16 the number of points ahead to predict.

The Encoder-Decoder model only needs to re-

construct the original time-series, however there is a

hyper-parameter that is the number of hidden LSTM

units. We used the same number for the encoder and

the decoder. In the experiments, we varied the num-

ber of hidden nodes as 16, 32, 64 and 128.

6.2 Datasets

In what follows, we provide a brief overview of each

used dataset.

6.2.1 Power Demand

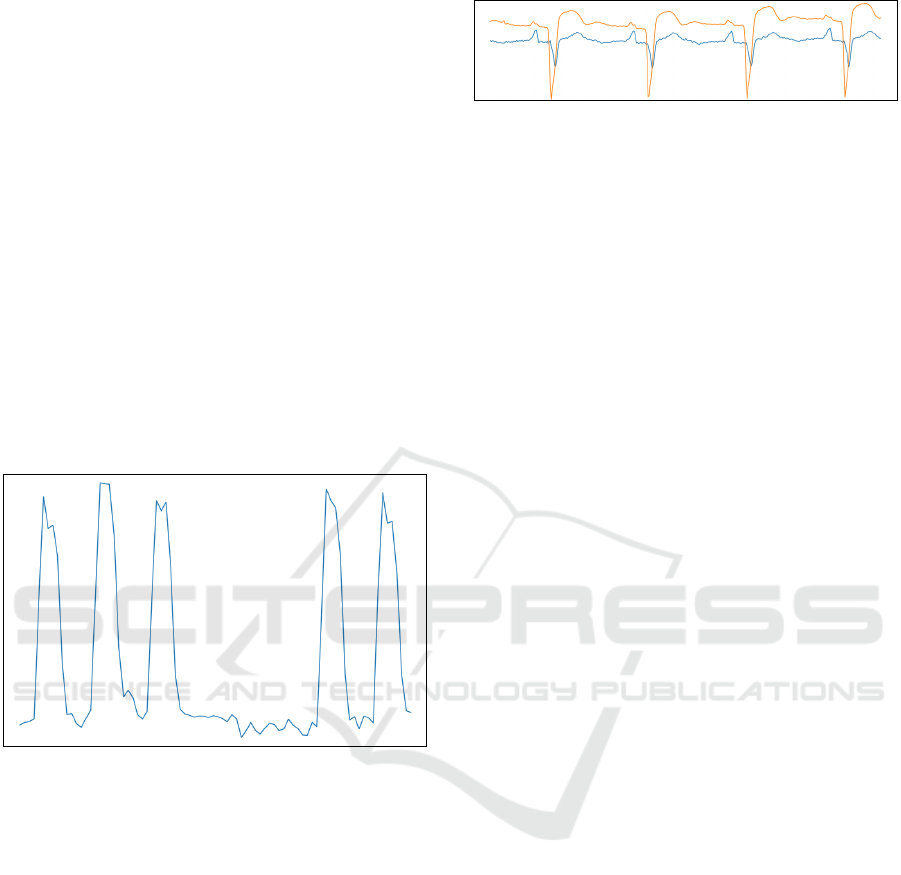

Figure 8: A normal week of power demand, starting at

Wednesday.

The power demand dataset provided by (Keogh

et al., 2007) registered the demand for energy sup-

ply for one year. The normal behavior is high demand

during the weekdays, and low during the weekends.

Then, the high demand on the weekends or low de-

mand on weekdays indicate for us anomalies not an-

notated.

The dataset is then sub-sampled by a factor of 8,

and broken in non-overlapping windows of 84 points,

that represent exactly one week of data. This was

also performed in (Malhotra et al., 2016). Figure 8

shows a normal behavior of power demand starting

on Wednesday.

The sets s

n

, v

n

and v

a

were built using the first

40% of dataset of the year, and the remaining to the

set t

a

. So we can better calculate the scores, as we

will have more anomalous points to test.

Figure 9: 4 heartbeats of the electrocardiogram dataset.

6.2.2 Electrocardiogram

The other real-world dataset is the mitdbx_108 also

provided by (Keogh et al., 2007), that depicts an elec-

trocardiogram with three distinct anomalies. This

dataset is not so well behaved like the power demand

since the heartbeat can occur at a different pace in dif-

ferent parts of the time series. This dataset is particu-

larly harder to train the encoder-decoder model since

it’s harder to find the right size and skip for the sliding

window.

This dataset is sub-sampled by a factor of 4, and

broken in non-overlapping windows of 93 points,

which represents on average one cycle of a heartbeat

of the patient’s electrocardiogram. Figure 9 shows

four cycles of a patient’s heartbeat.

As we applied in the power demand dataset, we

divided the first 40% of the e.c. to create s

n

, v

n

and v

a

and the remaining we allocated to t

a

.

6.3 Results

In this section, we present the results outputted by

TSPME-AD and its competitors. We compare our

proposal with’ Stacked LSTM (SL), and Encoder-

Decoder (ED) anomaly detection techniques. We also

evaluate the combination of these techniques using

the following ensemble strategies: Simple average

Ensemble (SA), Damped Average Ensemble (DA),

and Simple Weighted Average Ensemble (SWA).

As we mentioned before, to evaluate these

anomaly detection strategies, we use Power Demand

and Electrocardiogram datasets. We measure the per-

formance in terms of f-measure, studying two levels

of weighting between precision and recall. First, we

compute F1-score, using β = 1, which gives a bal-

anced weight to both measures. After, we compute

F

0.1

, F-measure with β = 0.1, which provides higher

weight to precision than to recall in the F-measure for-

mula. The reason to evaluate F

0.1

is the extremely

imbalanced behaviour of the time series data. As

the number of normal data is higher than the num-

ber of anomalies, an approach that produces a higher

number of false positives may not be feasible in an

anomaly detection problem. Additionally, we also an-

alyze the precision and recall separately.

Model-centered Ensemble for Anomaly Detection in Time Series

705

6.3.1 Evaluation Results from Power Demand

Dataset

Power Demand dataset is a periodic time series data.

It means that the number of points per cycle is con-

stant in time. This characteristic aids pattern recogni-

tion, and consequently, the anomaly prediction.

Table 1 shows the precision, recall, F

0.1

and F

1

for all the baseline models and the ensemble models

evaluated, trained and tested with Power Demand. As

we can see, the Simple Average (SA) and Damped

Average (DA) ensembles achieved the best results in

terms of f

0.1

and F

1

, respectively. In this experiment,

TSPME-AD achieved the second-best result in terms

of F

1

and F

0.1

.

This experiment shows that the weighted damped

average strategy of TSPME-AD achieves quality re-

sults, but it does not outperform the simple damped

average approach (DA). The great performance of

these damping strategies can be explained by the out-

put of the anomaly detection base models. A damping

average attenuates the input values before averaging.

As the output range of these models is wide, a damp-

ing strategy helps to standardize the model’s outputs.

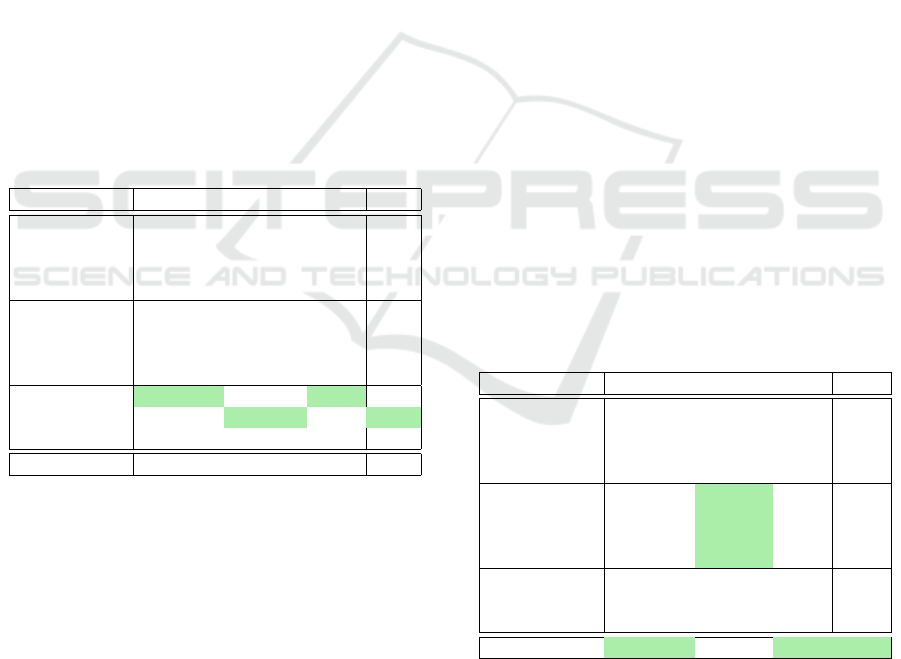

Table 1: Test results for the Power Demand dataset.

MODELS

a

Precision Recall F

0.1

F

1

SL [K = 2] 4.42% 77.78% 0.04 0.08

SL [K = 4] 5.49% 77.78% 0.05 0.10

SL [K = 8] 22.86% 44.44% 0.22 0.30

SL [K = 16] 12.77% 66.67% 0.12 0.21

ED [H = 16] 47.06% 44.44% 0.47 0.45

ED [H = 32] 3.39% 22.22% 0.03 0.05

ED [H = 64] 59.09% 72.22% 0.59 0.65

ED [H = 128] 18.52% 27.78% 0.18 0.22

SA 100.0% 44.44% 0.98 0.61

DA 76.19% 88.89% 0.76 0.82

SWA 25.00% 72.22% 0.25 0.37

TSPME-AD 76.47% 72.22% 0.76 0.74

a

SL: Stacked LSTM, ED: Encoder Decoder, SA:

Simple Average Ensemble, DA: Damped Aver-

age ensemble, SWA: Simple Weighted Average

Ensemble, TSPME-AD: Time Series Prediction

Model Ensemble for Anomaly Detection.

6.3.2 Evaluation Results from

Electrocardiogram Dataset

As the duration of a cyclic in an electrocardiogram

varies from one instance to another, this data is called

as quasi-periodic time-series. This class of time-

series is challenging to build a prediction model be-

cause we also need to discover an average duration of

a cyclic, as done by (Malhotra et al., 2016).

As in the previous subsection, Table 2 shows the

precision, recall, F

0.1

and F

1

for all baseline models

and the ensemble model trained and tested using this

dataset. However, the TSPME-AD achieved the best

results regarding F

1

, F

0.1

, and precision, which is dif-

ferent from the results obtained using the Power De-

mand dataset. The Encoder-Decoder-based models

achieve the best recall results, but the precision score

of these models indicates that almost all normal data

are classified as anomaly data.

In this experiment, the standard ensemble fusion

strategies, such as SA, DA, and SWA, are not able to

combine the baseline models (Malhotra et al., 2015;

Malhotra et al., 2016) properly. The low performance

of these ensembles can be explained by the low per-

formance of encoder-decoder base models. The stan-

dard ensemble functions can not attenuate the poor

anomaly detection ability of Encoder-Decoder mod-

els.

We can conclude that the TSPME-AD fusion strat-

egy (using a weighted damped average function) can

compensate poor results of some anomaly detection

baseline models and produce an ensemble with better

quality results than the other fusion approaches and

baseline models individually.

It is worth to mention that TPSME-AD, in general,

outperforms the detection anomaly models from the

state-of-the-art techniques (SL and ED) as already ex-

pected since our ensemble model combines the best of

models (Malhotra et al., 2015; Malhotra et al., 2016)

on detecting anomalous time series.

Table 2: Test results for the Electrocardiogram.

MODELS

a

Precision Recall F

0.1

F

1

SL [K = 2] 22.37% 47.80% 0.22 0.30

SL [K = 4] 18.37% 57.07% 0.18 0.28

SL [K = 8] 20.97% 48.29% 0.21 0.29

SL [K = 16] 42.28% 30.73% 0.42 0.36

ED [H = 16] 7.02% 100% 0.07 0.13

ED [H = 32] 7.36% 100% 0.07 0.14

ED [H = 64] 7.37% 100% 0.07 0.14

ED [H = 128] 7.37% 100% 0.07 0.14

SA 30.84% 48.29% 0.31 0.38

DA 11.33% 60.00% 0.11 0.19

SWA 34.05% 46.34% 0.34 0.39

TSPME-AD 41.00% 47.80% 0.41 0.44

a

SL: Stacked LSTM, ED: Encoder Decoder, SA:

Simple Average Ensemble, DA: Damped Aver-

age ensemble, SWA: Simple Weighted Average

Ensemble, TSPME-AD: Time Series Prediction

Model Ensemble for Anomaly Detection.

ICAART 2020 - 12th International Conference on Agents and Artificial Intelligence

706

7 CONCLUSION AND FUTURE

WORK

In this paper, we provide an approach for anomaly

detection which combines two state-of-the-art detec-

tion models, one based on stacked LSTM and another

one encoder-decoder based. TPSME-AD, in general,

outperforms the detection anomaly models from the

state-of-the-art techniques as already expected since

our ensemble model combines the best of models

(Malhotra et al., 2015; Malhotra et al., 2016) on de-

tecting anomalous time series. In the experiments, we

also show that, for a quasi-periodic time series data,

our model can outperform also standard ensemble fu-

sion approaches, such as simple average, damped av-

erage, and simple weighted average.

As a future direction, we aim at evaluating our

proposal with other datasets like the electrocardio-

gram, and the space-shuttle valve time-series (Keogh

et al., 2007). Another future improvement can be

added to a regularization of the combination function

so that we can mitigate the overfitting in the validation

dataset.

ACKNOWLEDGMENTS

This work is partially supported by the FUNCAP SPU

8789771/2017, and the UFC-FASTEF 31/2019.

REFERENCES

Aggarwal, C. C. (2013). Outlier ensembles: position paper.

ACM SIGKDD Explorations Newsletter, 14(2):49–58.

Chandola, V., Banerjee, A., and Kumar, V. (2009).

Anomaly detection: A survey. ACM computing sur-

veys (CSUR), 41(3):15.

Gao, J. and Tan, P.-N. (2006). Converting output scores

from outlier detection algorithms into probability es-

timates. In Sixth International Conference on Data

Mining (ICDM’06), pages 212–221. IEEE.

Gao, Y., Yang, T., Xu, M., and Xing, N. (2012). An un-

supervised anomaly detection approach for spacecraft

based on normal behavior clustering. In 2012 Fifth

International Conference on Intelligent Computation

Technology and Automation, pages 478–481. IEEE.

Hochreiter, S. and Schmidhuber, J. (1997). Long short-term

memory. Neural computation, 9(8):1735–1780.

Iverson, D. L. (2004). Inductive system health monitoring.

Keogh, E., Lin, J., Lee, S.-H., and Van Herle, H. (2007).

Finding the most unusual time series subsequence: al-

gorithms and applications. Knowledge and Informa-

tion Systems, 11(1):1–27.

Kieu, T., Yang, B., and Jensen, C. S. (2018). Outlier detec-

tion for multidimensional time series using deep neu-

ral networks. In 2018 19th IEEE International Con-

ference on Mobile Data Management (MDM), pages

125–134. IEEE.

Kittler, J., Hater, M., and Duin, R. P. (1996). Combining

classifiers. In Proceedings of 13th international con-

ference on pattern recognition, volume 2, pages 897–

901. IEEE.

Kong, X., Song, X., Xia, F., Guo, H., Wang, J., and Tolba,

A. (2018). Lotad: Long-term traffic anomaly detec-

tion based on crowdsourced bus trajectory data. World

Wide Web, 21(3):825–847.

Liu, F. T., Ting, K. M., and Zhou, Z.-H. (2012). Isolation-

based anomaly detection. ACM Transactions on

Knowledge Discovery from Data (TKDD), 6(1):3.

Malhotra, P., Ramakrishnan, A., Anand, G., Vig, L., Agar-

wal, P., and Shroff, G. (2016). Lstm-based encoder-

decoder for multi-sensor anomaly detection. arXiv

preprint arXiv:1607.00148.

Malhotra, P., Vig, L., Shroff, G., and Agarwal, P. (2015).

Long short term memory networks for anomaly detec-

tion in time series. In Proceedings, page 89. Presses

universitaires de Louvain.

Meng, F., Yuan, G., Lv, S., Wang, Z., and Xia, S. (2018).

An overview on trajectory outlier detection. Artificial

Intelligence Review.

Tariq, S., Lee, S., Shin, Y., Lee, M. S., Jung, O., Chung,

D., and Woo, S. S. (2019). Detecting anomalies in

space using multivariate convolutional lstm with mix-

tures of probabilistic pca. In Proceedings of the 25th

ACM SIGKDD International Conference on Knowl-

edge Discovery & Data Mining, pages 2123–2133.

ACM.

Wang, X., Lin, J., Patel, N., and Braun, M. (2018). Exact

variable-length anomaly detection algorithm for uni-

variate and multivariate time series. Data Mining and

Knowledge Discovery, 32(6):1806–1844.

Model-centered Ensemble for Anomaly Detection in Time Series

707