Comprehensive Performance Measures, Job Satisfaction and

Managerial Performance: The Effect of Trust in Superior and

Organizational Commitment

Utami Puji Lestari

1

and Yusep Friya Purwa Setya

1

1

Department of Accounting, Politeknik Negeri Jakarta, Jalan Prof. Dr. G. A. Siwabessy, Kampus Baru UI, Depok,

Indonesia

Keywords: Performance, measures, job, satisfaction, trust, commitment.

Abstract: This study’s objectives are, first, to investigate if the use of financial and non-financial measures is related to

some employee performances, such as job satisfaction, managerial performance, and commitment to the

organization. This study also investigates if financial and non-financial performance measures affect

employees’ job satisfaction and managerial performance through employees’ trust in superiors and their

commitment to the organization. The data were collected from management-level employees of two service

industries – public accounting firms and state-owned administrative service – located in Jakarta, Bogor,

Depok, Banten, and Serang. The 79 data were analyzed by using PLS-SEM with SmartPLS Software Version

3.2.8. The results show that (1) financial performance measures do not affect job satisfaction directly or

indirectly, (2) financial performance measures affect managerial performance through commitment to the

organization, and (3) the use of non-financial measures as the company’s employee performance evaluation

affect employee job satisfaction and managerial performance indirectly through higher trust in superior and

commitment to organization.

1 INTRODUCTION

Companies cannot depend only on traditional

accounting-based measures for their performance

evaluations in today’s more competitive situation

(Chenhall, 1997; Chenhall & Langfield-Smith, 2007;

Hoque, Mia, & Alam, 2001; Kaplan & Norton, 1992).

They have been forced to adopt a variety of

performance improvement programmes, for instance

benchmarking, which need an upgrade of their

performance measurement systems to the more

comprehensive one that includes non-financial

performance measures (Bai & Sarkis, 2012;

Kulatunga, Amaratunga, & Haigh, 2011; Micheli &

Manzoni, 2010; Muchiri, Pintelon, Gelders, &

Martin, 2011; Neely, 1999). Regardless of the

increasing tendency of the adoption of more complete

performance measurement evaluation system, there is

not enough empirical support on the behavioural

consequences of the use of this system (C. M. Lau,

2015; C. M. Lau & Roopnarain, 2014). In other

words, there is a need to comprehend how the use of

both financial and non-financial performance

measures affect employees’ attitudes and

performance. This study aims to fill this knowledge

gap by investigating the consequense of the use of

financial and non-financial performance measures on

employees’ attitudes and performances, including

their trust in superior, organizational commitment,

job satisfaction and managerial performance.

This study includes the effect of trust in superior

on the association concerning fianancial and non-

financial performance measures and employees’ job

satisfaction and managerial performance, because

better performance evaluation tend to happen when

there is a trust between subordinates and their

superiors in an organization. Prior studies have found

that there is a positive association between

performance evaluation and trust in superiors (e.g.

Chia, Lau, & Tan, 2014; C. M. Lau & Sholihin,

2005). This study contributes to this area by studying

trust in superior in the context of financial and non-

financial performance measures in a service industry.

The research of organizational commitment is

important as it has significant effect on employees’

performance. In the context of job satisfaction as

116

Lestari, U. and Purwa Setya, Y.

Comprehensive Performance Measures, Job Satisfaction and Managerial Performance: The Effect of Trust in Superior and Organizational Commitment.

DOI: 10.5220/0010545000003153

In Proceedings of the 9th Annual Southeast Asian International Seminar (ASAIS 2020), pages 116-126

ISBN: 978-989-758-518-0

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

employees’ performance, the relationship between

organizational commitment and job satisfaction is

unclear. Some studies have used job satisfaction as

the dependent variable (e.g. Vandenberg & lance,

1992); while other previous studies have recognised

job satisfaction as the independent variable (Jernigan,

Beggs, & Kohut, 2002; Lok & Crawford, 2001; Tan

& Lau, 2012). Regarding organizational commitment

and managerial performance, some studies have

found a positive relationship (e. g. Chong & Law,

2016; Mathieu & Zajac, 1990); while other studies

have found no relationship (Steers, 1977; Wiener &

Vardi, 1980). This study extends Chong and Law’

(2016) study by adding job satisfaction as one of

dependent variable. However, this study differs from

Chong and Law’ (2016) study as this study

investigates the impact of financial and non-financial

performance measures on employees’ job satisfaction

and managerial performance through trust in superior

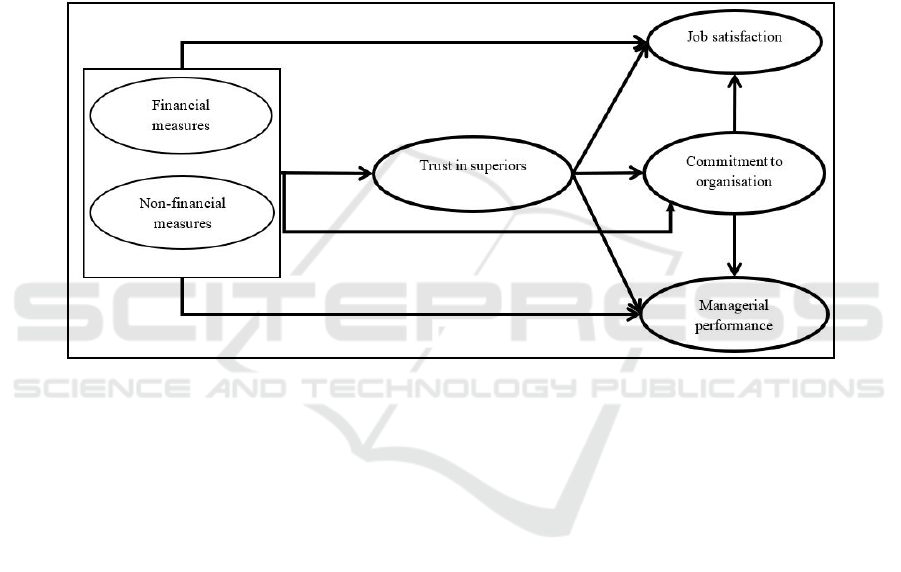

and organizational commitment. Figure 1 presents the

model of the study.

The literature relevant to this study is reviewed

and followed by hypotheses development. The

research method and the results of the study then

presented. The last section concludes the paper with

conclusions, limitation and suggestions.

Figure 1: Research Model

2 LITERATURE REVIEW AND

HYPOTHESES

DEVELOPMENT

2.1 The Use of Financial and

Non-financial Performance

Measures and Employees’ Job

Satisfaction and Managerial

Performance

Companies' use of financial and non-financial

performance measures is believed to have favorable

behavioral significances (C. M. Lau & Sholihin,

2005). It provides some indications and encourages

subordinates to make some progress in their activities

(Hoque et al., 2001). In other words, these

significances tend to improve subordinates’

performance, such as their job satisfaction and

managerial performance, which lead to the following

hypotheses.

H1: Financial performance measures are

associated with job satisfaction

H2: Non-financial performance measures are

significantly associated with job satisfaction

H3: Financial performance measures are

significantly associated with managerial

performance

H4: Non-financial performance measures are

significantly associated with managerial

performance

Comprehensive Performance Measures, Job Satisfaction and Managerial Performance: The Effect of Trust in Superior and Organizational

Commitment

117

2.2 The Use of Financial and

Non-financial Performance

Measures, Trust in Superior and

Employees’ Job Satisfaction and

Managerial Performance

The concept of trust used in this study is borrowed

from Read (1962), who conceptualized trust as

“Subordinates’ trust in superior’ motivation

regarding subordinates status and career in the

company.” Multiple financial and non-financial

performance measures usage as the employees’

performance evaluation may increase subordinates’

trust in superior (C. M. Lau & Sholihin, 2005;

Whitener, Brodt, Korsgaard, & Werner, 1998). By

using financial and non-financial measures that

represent a more comprehensive measures, these

show that the company has taken into account the

contributions made by the subordinates, superior then

would be perceived as more concern about their

organization and subordinates, which lead to higher

subordinates’ trust in superior (C. M. Lau & Sholihin,

2005). While subordinates and superiors in an

organization trust each other, there would be less

organizational conflicts (C. M. Lau & Sholihin,

2005), which lead to higher job satisfaction and

managerial performance. Accordingly, the following

hypotheses are tested.

H5: Financial performance measures are

significantly associated with job satisfaction

through trust in superior

H6: Non-financial performance measures are

significantly associated with job satisfaction

through trust in superior

H7: Financial performance measures are

significantly associated with managerial

performance through trust in superior

H8: Non-financial performance measures are

significantly related to managerial performance

through trust in superior

2.3 The Use of Financial and

Non-financial Performance

Measures, Commitment to

Organization and Job Satisfaction

and Managerial Performance

Porter, Steers, Mowday & Boulian (1974) define

commitment to the organization as the relative

strength of an individual’s identification with and

attachment to an organization. Previous studies in

organizational behavior show that organizational

commitment is a critical factor, positively affecting

employees' behavior, such as enhancing their effort,

performance, and loyalty to an organization (Mathieu

& Zajac, 1990; Sholihin & Pike, 2010).

By using multiple financial and non-financial

performance measures, an organization would be able

to evaluate individual performance from many

perspectives (Kaplan & Norton, 1996). As it is seen

as more comprehensive, individual that evaluated by

that kind of performance measurement tend to show

a more favorable behavior, including a higher

commitment to organization (C. M. Lau & Moser,

2008). Previous study by Lau and Moser (2008)

suggest that the use of non-financial performance

measure in manufacturing companies has a positive

effect on organizational commitment. Employees

with higher organizational commitment tend to have

a higher motivation to support their organization in

achieving their goals (Chong & Law, 2016). In other

words, employees with higher organizational

commitment have higher performance than those

with lower organizational commitment. The

discussions lead to the following hypotheses.

H9: Financial performance measures are

significantly associated job satisfaction through

commitment to the organization

H10: Non-financial performance measures are

significantly related to job satisfaction through a

commitment to the organization

H11: Financial performance measures are

significantly associated with managerial

performance through a commitment to

organization

H12: Non-financial performance measures are

significantly related to managerial performance

through a commitment to organization

2.4 Trust in Superior and Commitment

to Organization

It is mentioned before that organization which have

subordinates with higher trust in superior may have

less conflicts (C. M. Lau & Sholihin, 2005). As this

situation leads to a more comfort work environment,

it would then increase employees’ attachment to their

organization (Chong & Law, 2016). In other words,

trust in superior may lead to higher organizational

commitment. Accordingly, the following hypothesis

is developed.

H13: Trust in superior is significantly related to

commitment to organization

ASAIS 2020 - Annual Southeast Asian International Seminar

118

2.5 The Use of Financial and

Non-financial Performance

Measures, Trust in Superior,

Commitment to Organization and

Employees’ Job Satisfaction and

Managerial Performance

The use of multiple financial and non-financial

performance measures as employees’ performance

evaluation tools in an organization may increase

subordinates’ trust in superior (C. M. Lau & Sholihin,

2005; Whitener et al., 1998). This will lead to higher

employees’ organizational commitment (Chong &

Law, 2016) and their’ effort to help companies in

achieving their objectives, which in turn, may

improve employees performance. The following

hypotheses are tested.

H14: Financial performance measures are

significantly associated with job satisfaction via

trust in superior and a commitment to

organization

H15: Non-financial performance measures are

significantly associated with job satisfaction via

trust in superior and a commitment to

organization

H16: Financial performance measures are

significantly associated with managerial

performance via trust in superior and

commitment to organization

H17: Non-financial performance measures are

significantly ssociated with and commitment to

organization

3 METHOD

3.1 Sample and Data Collection

Procedure

Data were collected from employees at the middle

and senior level of accounting firms and one state-

owned administrative service located in Jakarta,

Bogor, Depok, Tangerang, Bekasi, Banten and

Serang. Data of accounting firms is obtained from the

list in the Ministry of Finance electronic database.

The accounting firms – one type of business service –

were selected as based on Indonesian Central Bank’

Activity Survey, in the future would become one of

service sectors with the highest business growth in

Indonesia (Raswa, 2015). The state-owned

administrative service was selected as based on

Indonesian Ministry of Finance (2009), is one of

government institution that has successfully reform

its bureaucracy.

An email was sent to the accounting firms in the

list, asking the partner of the firms to obtain two

names of their senior auditors and supervisors or send

the link of the questionnaire directly to two of their

senior and/or supervisor auditors. For the state-owned

administrative service, after obtaining the research

permission from the head office, the link of the survey

questionnaire was emailed to the public relations

department of each office, asking them to send the

link to the middle and senior managers. Of the 303

emails sent to the respondents, only 79 fill the

questionnaire, constituting a 26.07% response rate.

This rate is higher than the 10%-20% of average

response rate for surveys of higher management level

of participant-level (Menon, Bharadwaj, & Howell,

1996; Voola, Casimir, Carlson, & Agnihotri, 2012).

The demographic data show that the participants

consist of 19 females (24.05%) and 60 males

(75.95%). Only eight participants were part time

employees (10.13%), while the rest were full time

employees (89.87%). Most of the participants have

worked at their current workplace for less than five

years (49.37%), 17.72% have been employed for 5 to

10 years at the same place, and 32.91% have worked

for more than 10 years on the same workplace. All

participants held tertiary education, with about

58.23% holding bachelor’s degrees and 41.77%

owned master’s degrees.

3.2 Measurement of Variables

3.2.1 Non-financial Performance Measures

The financial and non-financial performance

measures were assessed by using the instrument

developed by Lau and Moser (2008). The participants

were asked to rate the importance of the items when

their superior is evaluating their performance. The

instruments have shown satisfactory reliability level

with Cronbach Alpha of 0.821 (financial measures)

and 0.912 (non-financial measures).

3.2.2 Trust in Superior

This variable is measured using a four-item

instrument developed by Read (1962). The

participants were asked to rate the extent to which

they agree with the statements. The instruments have

demonstrated high internal reliability with Cronbach

Alpha value of 0.821. One item was deleted as it has

factor loading lower than 0.5.

Comprehensive Performance Measures, Job Satisfaction and Managerial Performance: The Effect of Trust in Superior and Organizational

Commitment

119

3.2.3 Organizational Commitment

Organizational commitment was measured using an

eleven-item instrument developed by Mowday,

Steers and Porter (1979). After deleting two items that

have factor loadings below 0.5, the variable

demonstrated satisfactory internal reliability with

Cronbach Alpha value of 0.944.

3.2.4 Job Satisfaction

The variable was evaluated using an instrument

developed by Rusbult and Farrel (1983). The items of

this variable have satisfactory factor loadings, with

Cronbach Alpha value of 0.943.

3.2.5 Managerial Performance

Managerial performance was measured using the

nine-item self-rating instrument developed by

Mahoney, Jerdee and Carroll (1965). The items have

a satisfactory loadings value with Cronbach Alpha of

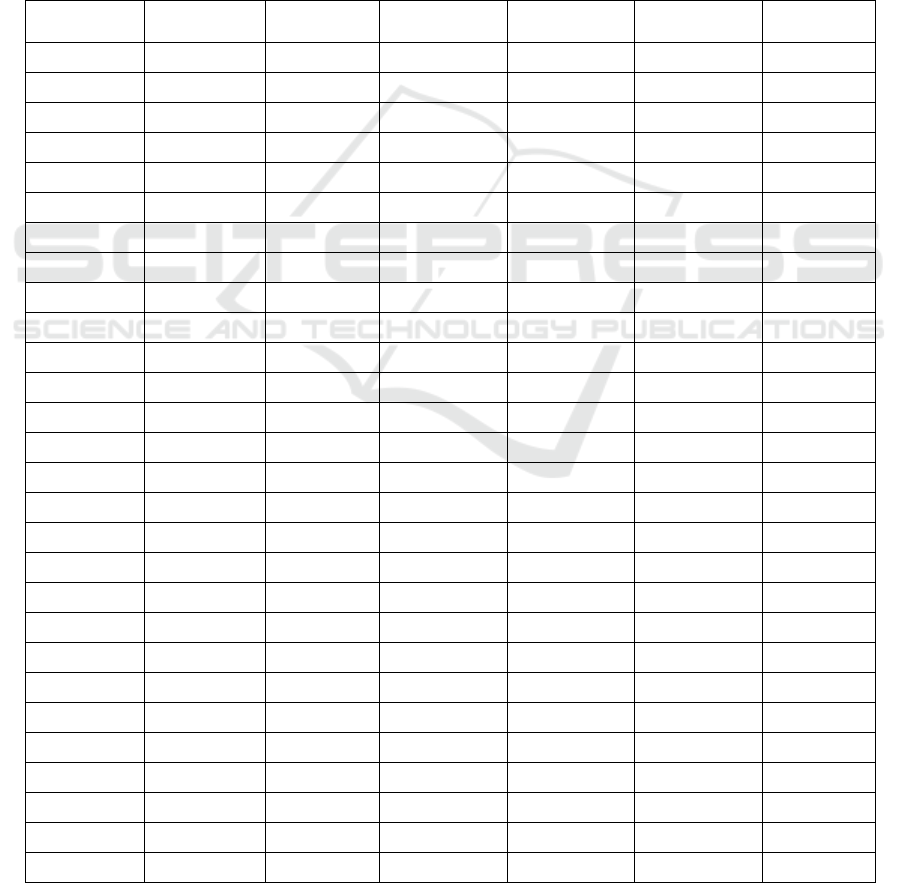

0.961. Table 1 shows the factor loadings for all items

of each variables while Table 2 demonstrate the

results of construct reliability and validity test. As

shown in Table 3, all of the variables have acceptable

discriminant validity as the square root AVE for each

variable is more significant than any value of the non-

diagonal element.

Table 1: Factor Loadings Of Variables.

Commitment Fin

Job

Satisfaction

Managerial

p

erformance

Non Fin Trust

F1 0,904

F2 0,843

F3 0,828

JobS1

0,906

JobS2

0,771

JobS3

0,924

JobS4

0,934

JobS5

0,914

JobS6

0,842

MPerf2

0,888

MPerf3

0,947

MPerf4

0,839

MPerf5

0,944

MPerf6

0,827

MPerf7

0,714

MPerf8

0,900

MPerf9

0,879

Mperf1

0,905

NF1

0,789

NF2

0,783

NF3

0,744

NF4

0,766

NF5

0,801

NF6

0,754

NF7

0,717

NF8

0,809

NF9

0,711

OrgCom1 0,701

ASAIS 2020 - Annual Southeast Asian International Seminar

120

OrgCom10 0,626

OrgCom11 0,900

OrgCom2 0,834

OrgCom3 0,814

OrgCom4 0,663

OrgCom5 0,898

OrgCom6 0,888

OrgCom7 0,709

OrgCom8 0,879

OrgCom9 0,893

Trust2

0,777

Trust3

0,935

Trust4

0,856

Table 2: Construct Reliability and Validity.

Cronbach's

Alpha

rho_A

Composite

Reliabilit

y

Average Variance

Extracted (AVE)

Organizational commitment 0,944 0,953

0,953 0,651

Financial measures 0,821 0,822

0,894 0,738

Job Satisfaction 0,943 0,954

0,955 0,781

Managerial performance 0,961 0,966

0,967 0,764

Non-Financial measures 0,912 0,921

0,927 0,585

Trust in superior 0,821 0,853

0,893 0,737

Table 3: Fornell Larker Discriminant Validity.

Commitment Fin

Job

Satisfaction

Managerial

p

erformance

Non-Fin Trust

Organizational commitment 0,807

Financial measures 0,609 0,859

Job Satisfaction 0,699 0,537 0,884

Managerial performance 0,696 0,391 0,643 0,874

Non-Financial measures 0,638 0,680 0,487 0,511 0,765

Trust in superior 0,608 0,440 0,487 0,546 0,559 0,858

4 RESULTS

Partial least square equation modelling with

SmartPLS

®

software Version 3.2.8 (Ringle, Wende,

& Becker, 2015) was used to test the models. By

using bootstrapping with 5.000 samples with

replacement, the results in Table 4 have shown that

all of the R

2

values of each independent variables are

higher than 0.1, which means that variables explained

by the dependent variables have statistical and

practical significance.

Comprehensive Performance Measures, Job Satisfaction and Managerial Performance: The Effect of Trust in Superior and Organizational

Commitment

121

Table 4: The R-Square Values.

R Square R Square Adjusted

Organizational Commitment 0,547 0,529

Job Satisfaction 0,513 0,487

Managerial performance 0,519 0,493

Trust in superior 0,305 0,287

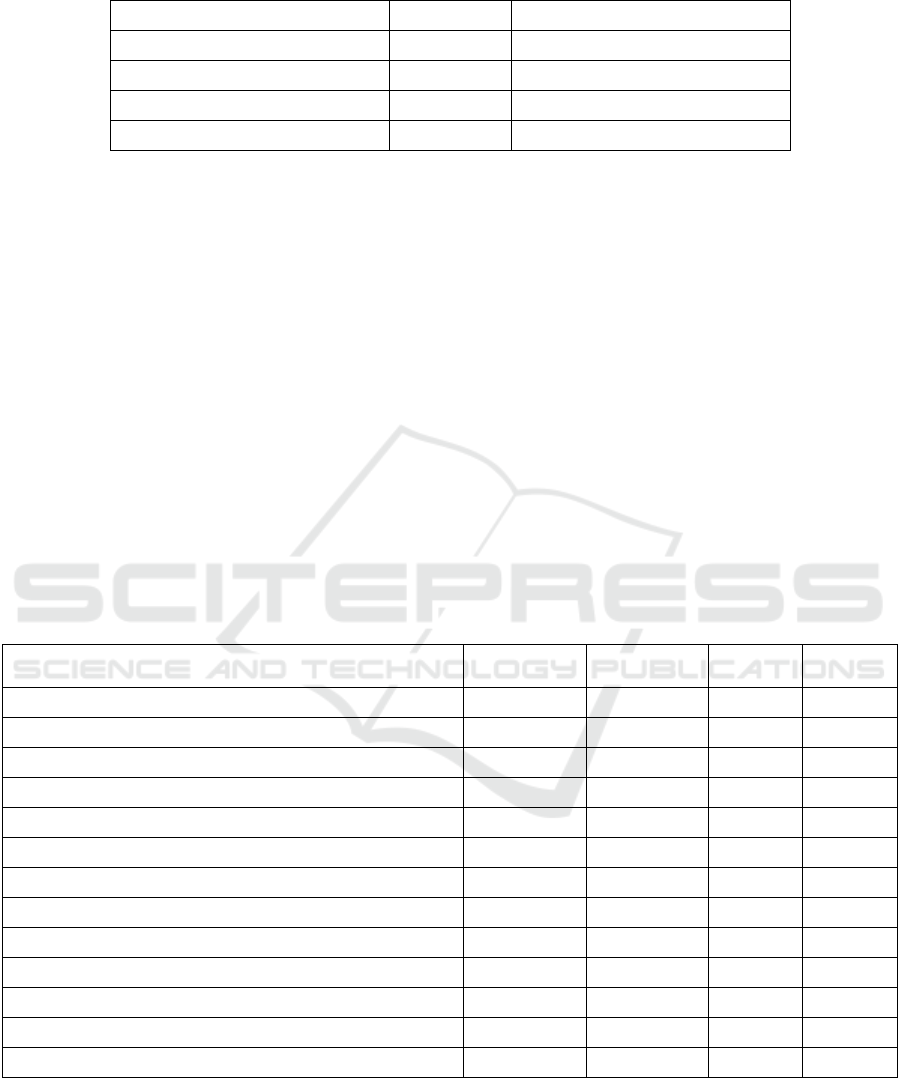

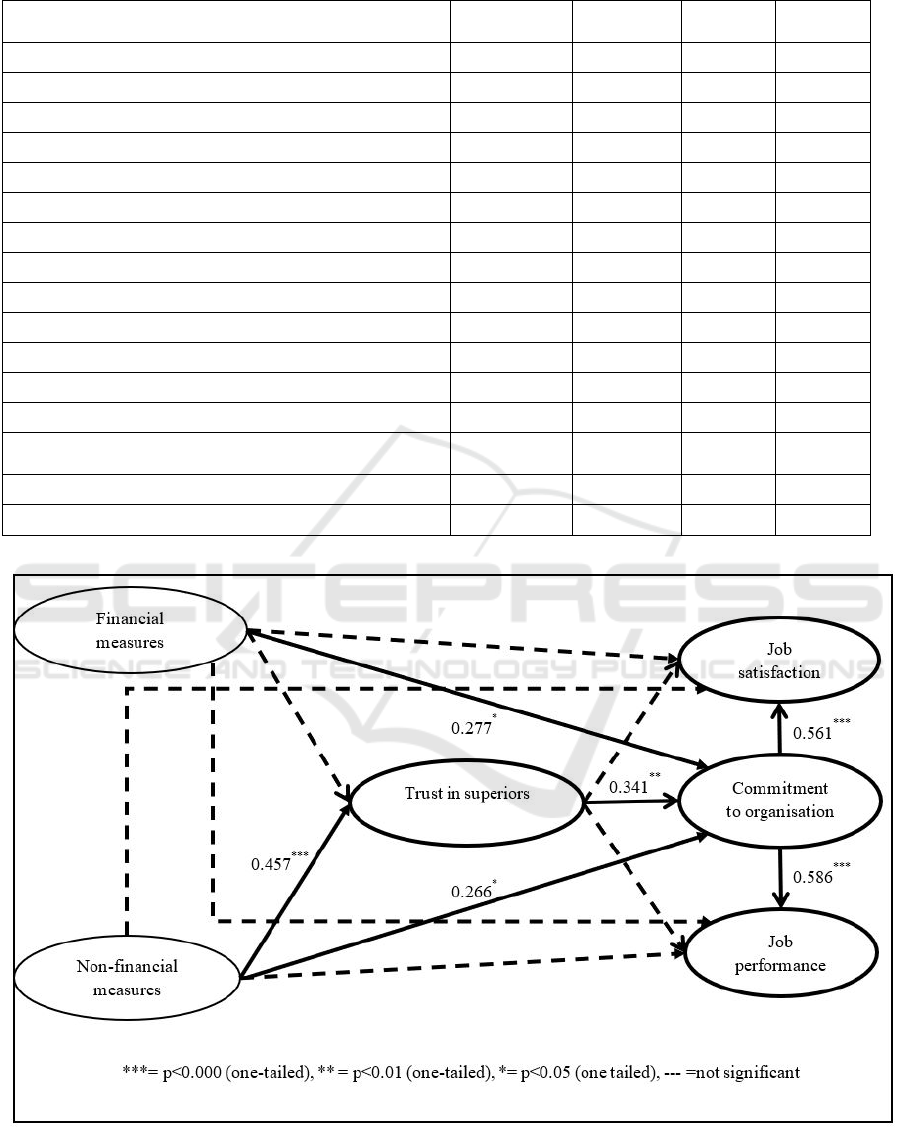

The results presented in Table 5, Table 6, and

Figure 2 advice that only H10, H11, H13, H15 and

H17 are significant. H10 states that non-financial

performance measures are significantly related to job

satisfaction through organizational commitment;

while H11 states that financial performance measures

are connected significantly to managerial

performance. The results in Table 6 specify that non-

financial performance measures are connected

significantly to job satisfaction via organizational

commitment (0.149, p<0.005, one-tailed), and

financial performance measures are significantly

related managerial performance through

organizational commitment (0.162, p<0.05, one-

tailed). Therefore, H10 and H11 are supported. H13

states that trust in superior is significantly related to

organizational commitment. Table 5, Figure 2

indicate that trust in superior is associated

significantly with organizational commitment (0.341,

p<0.001, one-tailed), supporting H13. Finally, H15

and H17 state that non-financial performance

measures are significantly related to job satisfaction

through trust in superior and commitment to the

organization, and non-financial performance

measures are significantly associated with managerial

performance through trust in superior and

commitment to the organization respectively. Table 6

indicates that non-financial performance measures

are associated significantly with job satisfaction

through trust in superior and commitment to

organization (0.087, p<0.05, one-tailed) and non-

financial performance measures are associated

significantly with managerial performance through

trust in superior and commitment to organization

(0.091, p<0.05, one-tailed), which supported H15 and

H17 respectively.

Table 5: Beta Coefficients, Standard Deviation, t-Values and p-Values - Direct Effects.

Beta

Coefficient

Standard

Deviation

T Values P Values

Commitment -> Job Satisfaction 0,561 0,162 3,451 0,000

Commitment -> Managerial performance 0,586 0,131 4,481 0,000

Fin -> Commitment 0,277 0,135 2,051 0,020

Fin -> Job Satisfaction 0,188 0,172 1,090 0,138

Fin -> Managerial performance -0,134 0,138 0,969 0,166

Fin -> Trust 0,129 0,149 0,863 0,194

Non-Fin -> Commitment 0,266 0,149 1,790 0,037

Non-Fin -> Job Satisfaction -0,046 0,137 0,335 0,369

Non-Fin -> Managerial performance 0,131 0,157 0,837 0,201

Non-Fin -> Trust 0,457 0,133 3,431 0,000

Trust -> Commitment 0,341 0,108 3,157 0,001

Trust -> Job Satisfaction 0,088 0,136 0,645 0,260

Trust -> Managerial performance 0,177 0,115 1,531 0,063

ASAIS 2020 - Annual Southeast Asian International Seminar

122

Table 6: Beta Coefficients, Standard Deviation, t-Values, p-Values - Indirect Effects.

Beta

Coefficient

Standard

Deviation

T Values P Values

Fin -> Trust -> Commitment 0,044 0,055 0,805 0,211

Non-Fin -> Trust -> Commitment 0,156 0,070 2,225 0,013

Fin -> Commitment -> Job Satisfaction 0,155 0,102 1,525 0,064

Non-Fin -> Commitment -> Job Satisfaction 0,149 0,088 1,688 0,046

Fin -> Trust -> Commitment -> Job Satisfaction 0,025 0,034 0,724 0,235

Trust -> Commitment -> Job Satisfaction 0,191 0,088 2,180 0,015

Non-Fin -> Trust -> Commitment -> Job Satisfaction 0,087 0,051 1,717 0,043

Fin -> Trust -> Job Satisfaction 0,011 0,028 0,403 0,344

Non-Fin -> Trust -> Job Satisfaction 0,040 0,069 0,582 0,280

Fin -> Commitment -> Managerial performance 0,162 0,083 1,958 0,025

Non-Fin -> Commitment -> Managerial performance 0,156 0,108 1,443 0,075

Fin -> Trust -> Commitment -> Managerial performance 0,026 0,034 0,762 0,223

Trust -> Commitment -> Managerial performance 0,200 0,078 2,559 0,005

Non-Fin -> Trust -> Commitment -> Managerial

p

erformance

0,091 0,047 1,953 0,026

Fin -> Trust -> Managerial performance 0,023 0,036 0,637 0,262

Non-Fin -> Trust -> Managerial performance 0,081 0,062 1,306 0,096

Figure 2: Structural Model Results – Direct Effect

Comprehensive Performance Measures, Job Satisfaction and Managerial Performance: The Effect of Trust in Superior and Organizational

Commitment

123

5 CONCLUSIONS

This study’s objectives are to examine if financial and

non-financial measures are connected to some

employees’ performances, for instance, job

satisfaction, managerial performance and

organizational commitment. This study also

investigates whether financial and non-financial

performance measures affect employees’ job

satisfaction and managerial performance through

employees’ trust in superiors and their organizational

commitment. The findings show that (1) financial

performance measures affect organizational

commitment and (2) non-financial performance

measures affect (a) employees’ trust in superiors and

(b) their organizational commitment. As the results

also indicates that there are (1) no connection

between financial and non-financial performance

measures and (a) job satisfaction and (b) managerial

performance; (2) no relationship between employees’

trust in superior and (a) job satisfaction and (b)

managerial performance; and (3) employees’ trust in

superiors affect their organizational commitment; the

indirect effect tests have pointed out that (1) financial

performance measures affect managerial

performance fully through organizational

commitment and (2) non-financial performance

measures affect job satisfaction and managerial

performance fully through employees’ trust in

superiors and their organizational commitment.

The contributions of this study to the theory are as

follows. This study is advising the importance of

financial and non-financial performance measures on

the employees’ attitudes, namely employees’ trust in

superior and organizational commitment. Therefore,

this study’s results support Solihin and Pike (2010)

and Lau and Moser (2008). This study also indicates

that employees' trust in superiors and organizational

commitment increase our understanding on how

financial and non-financial performance measures

affect job satisfaction and managerial performance.

The use of financial performance measures would

affect managerial performance only through

organizational commitment. This result support

Solihin and Pike (2010), who suggest that the

association between financial performance measures

and organizational commitment is direct. The use of

non-financial performance measures would affect job

satisfaction and managerial performance through

employees’ organizational commitment only or

through both employees’ trust in superior and

organizational commitment. These results support

Chong and Law (2016) who argue that trust in

superior and organisational commitment have a

significant role in increasing managerial

performance. The lack of direct and indirect link

between financial performance measures and job

satisfaction through trust in superior and or

organizational commitment indicates that this

relationship may happen through other factors.

This study’s practical contributions are to enhance

employees’ job satisfaction and managerial

performance; organizations need to design and

manage a clear performance measurement system and

raise their employees’ trust in superiors to gain better

employees’ organizational commitment.

There are some limitations to this study. The use of

only two types of service industries makes the results

may not apply to other sectors. Future research should

include other service industries. Second, more than

30% of the respondents have worked for the same

organization for more than ten years. This may raise

the issue of “survivor bias” as these employees tend

to have stronger ties with their organization

(Hrebiniak & Alutto, 1972). As a result, their

commitment to the organization is relatively high,

which leads to better managerial performance and job

satisfaction. Research in the future may study this

issue in different settings.

REFERENCES

Bai, C., & Sarkis, J. 2012. Supply-chain performance-

measurement system management using

neighbourhood rough sets. International Journal of

Production Research, 50(9), 2484-2500.

doi:10.1080/00207543.2011.581010

Chenhall, R. H. 1997. Reliance on manufacturing

performance measures, total quality management and

organisational performance. Management Accounting

Research, 8 (2), 187-206.

Chenhall, R. H., & Langfield-Smith, K. 2007. Multiple

perspectives of performance measures. European

Management Journal, 25(4), 266-282.

doi:http://dx.doi.org/10.1016/j.emj.2007.06.001

Chia, D. P. S., Lau, C. M., & Tan, S. L. C. 2014. The

relationships between performance measures and

employee Outcomes: The mediating roles of procedural

fairness and trust. In A. Davila, M. J. Epstein, & J.-F.

Manzoni (Eds.), Performance Measurement and

Management Control: Behavioral Implications and

Human Actions (Studies in Managerial and Financial

Accounting) (Vol. 28, pp. 203-232): Emerald Group

Publishing Limited.

Chong, V., & Law, M. B. C. 2016. The effect of a budget-

based incentive compensation scheme on job

performance: The mediating role of trust-in-supervisor

and organisational commitment. Journal of Accounting

& Organizational Change,, 12(4).

ASAIS 2020 - Annual Southeast Asian International Seminar

124

Departemen Keuangan Republik Indonesia. 2009. Laporan

Kinerja Departemen Keuangan pada Kabinet Indonesia

Bersatu 2004-2009. Retrieved from

http://www.kemenkeu.go.id/sites/default/files/LKDK

%202004-2009%20low%20res.pdf

Hoque, Z., Mia, L., & Alam, M. 2001. Market competition,

computer-aided manufacturing and use of multiple

performance measures: an empirical study. British

Accounting Review, 33, 23-45.

Hrebiniak, L. G., & Alutto, J. A. 1972. Personal and role-

related factors in the development of organizational

commitment. Administrative Science Quarterly, 555-

573.

Jernigan, I. E., Beggs, J. M., & Kohut, G. F. 2002.

Dimensions of work satisfaction of predictors of

commitment typpe. Journal of Managerial Psychology,

17(7), 564-579.

Kaplan, R. S., & Norton, D. P. 1992. The balanced

scorecard--measures that drive performance. Harvard

Business Review, 70(1), 71-79. Retrieved from

http://search.ebscohost.com/login.aspx?direct=true&d

b=buh&AN=9205181862&site=ehost-live

Kaplan, R. S., & Norton, D. P. 1996. The Balanced

Scorecard-Translating Strategy into Action. Boston:

Harvard Business School Press.

Kulatunga, U., Amaratunga, D., & Haigh, R. 2011.

Structured approach to measure performance in

construction research and development. International

Journal of Productivity and Performance Management,

60(3), 289-310.

doi:http://dx.doi.org/10.1108/17410401111112005

Lau, C. M. 2015. The effects of nonfinancial performance

measures on role clarity, procedural fairness and

managerial performance. Pacific Accounting Review,

27(2), 142-165.

Lau, C. M., & Moser, A. 2008. Behavioural effects of

nonfinancial performance measures: the role of

procedural fairness. Behavioral Research in

Accounting, 20(2), 55-71.

Lau, C. M., & Roopnarain, R. 2014. The effect of non-

financial and financial measures on employee

motivation to participate in target setting. British

Accounting Review, 46, 228-247.

Lau, C. M., & Sholihin, M. 2005. Financial and

nonfinancial performance measures: How do they

affect job satisfaction? The British Accounting Review,

37(4), 389-413. doi:10.1016/j.bar.2005.06.002

Lok, P., & Crawford, J. 2001. Antecedents of organisational

commitment and the mediating role of job satisfaction.

Journal of Managerial Psychology, 16(8), 594-613.

Mahoney, T. A., Jerdee, T. H., & Carroll, S. J. 1965. The

job of management. Industrial Relations, 97-110.

Mathieu, J. E., & Zajac, D. M. 1990. A review and meta-

analysis of the antecedents, correlates, and

consequences of organizational commitment.

Psychological Bulletin, 108, 171-194.

Menon, A., Bharadwaj, S. G., & Howell, R. 1996. The

Quality and Effectiveness of Marketing Strategy:

Effects of Functional and Dysfunctional Conflict in

Intraorganizational Relationships. Journal of the

Academy of Marketing Science, 24(4), 299. Retrieved

from

http://libraryproxy.griffith.edu.au/login?url=http://sear

ch.ebscohost.com/login.aspx?direct=true&db=bth&A

N=9610060967&site=ehost-live&scope=site

Micheli, P., & Manzoni, J.-F. 2010. Strategic performance

measurement: Benefits, limitations and paradoxes.

Long Range Planning, 43(4), 465-476.

doi:http://dx.doi.org/10.1016/j.lrp.2009.12.004

Mowday, R., Steers, R., & Porter, L. 1979. The

measurement of organizational commitment’. Journal

of Vocational Behavior, 14, 224-247.

Muchiri, P., Pintelon, L., Gelders, L., & Martin, H. 2011.

Development of maintenance function performance

measurement framework and indicators. International

Journal of Production Economics, 131(1), 295-302.

doi:http://dx.doi.org/10.1016/j.ijpe.2010.04.039

Neely, A. 1999. The performance measurement revolution:

why now and what next. International Journal of

Operations & Production Management, 19(2), 205-

228.

Porter, L. W., Steers, R. M., Mowday, R. T., & Boulian, P.

V. 1974. Organizational commitment, job satisfaction,

and turnover among psychiatric technicians. Journal of

Applied Psychology, 59, 603-609.

Raswa, E. 2015. Keuangan, Real Estat, dan Jasa Perusahaan

Rajai Kegiatan Usaha Kuartal I 2015. Indonesian

Finance Today. Retrieved from

http://ift.co.id/posts/keuangan-real-estat-dan-jasa-

perusahaan-rajai-kegiatan-usaha-kuartal-i-2015

Read, W. H. 1962. Upward communication industrial

hierarchies. Human relations, 15, 3-15.

Ringle, C. M., Wende, S., & Becker, J.-M. 2015. SmartPLS

3. Bönningstedt: SmartPLS. Retrieved from

http://www.smartpls.com

Rusbult, C. E., & Farrel, D. 1983. A longitudinal test of the

investment model: impact on job satisfaction, job

commitment, and turnover variation in rewards, costs,

alternatives, and investments. Journal of Applied

Psychology 68, 429 – 438.

Sholihin, M., & Pike, R. 2010. Organisational commitment

in the police service: Exploring the effects of

performance measures, procedural justice and

interpersonal trust Financial Accountability &

Management, 26(4), 392-421.

Steers, R. M. 1977. Antecedents and outcomes of

organisational commitent. Administrative Science

Quarterly, 22, 46-55.

Tan, S. L. C., & Lau, C. M. 2012. The impact of

performance measures on employee fairness

perceptions, job satisfaction and organisational

commitment. Journal of Applied Management

Accounting Research, 10(2), 57.

Vandenberg, R. J., & lance, C. E. 1992. Examining the

causal order of job satisfaction and organisational

commitment. Journal of Management, 18(1), 153-167.

Voola, R., Casimir, G., Carlson, J., & Agnihotri, M. A.

2012. The effects of market orientation, technological

opportunism, and e-business adoption on performance:

A moderated mediation analysis. Australasian

Comprehensive Performance Measures, Job Satisfaction and Managerial Performance: The Effect of Trust in Superior and Organizational

Commitment

125

Marketing Journal (AMJ), 20(2), 136-146. Retrieved

from

http://www.sciencedirect.com/science/article/pii/S144

1358211000802

Whitener, E. M., Brodt, S. E., Korsgaard, M. A., & Werner,

J. M. 1998. Managers as initiators of trust: An exchange

relationship framework for understanding managerial

trustworthy behavior. The Academy of Management

Review, 23(3), 513-530.

Wiener, Y., & Vardi, Y. 1980. Relationship between job,

organisation and career commitment and work

outcomes - an integrative approach. Organisational

Behaviour and Human Performance, 26, 81-96.

ASAIS 2020 - Annual Southeast Asian International Seminar

126