Preferences of Islamic Commercial Bank Customers in Paying Zakah

Ida Syafrida, Indianik Aminah, Taufik Awaludin

Accounting Department, Politeknik Negeri Jakarta, Jl. Prof Dr.G.A. Siwabessy, Depok, Indonesia

Keywords Islamic Commercial Bank, Online Zakah, Preferences

Abstract This study aims to identify the use of online payment facilities, the types of zakah paid, and the zakah

payment facilities most frequently used by Islamic commercial bank customers. This is important to do, so

that Islamic banks can formulate the right policies in collecting zakah funds. The method used is descriptive

based on the results of a survey of Islamic bank customers in the Jabodetabek area. Research finds the

majority of Islamic bank customers have used electronic money, payment financial technology (fintech),

and market places for payment transactions. There are less Islamic bank customers who have paid zakah on

assets and zakah on income. In general, Islamic bank customers pay zakah by cash deposits through zakah

officers/volunteers, direct distribution, online transfer by ATM, and cash deposit via teller. Very few

customers use payment facilities through technology service applications both fintech, market places, even

base on the research none use applications from Islamic banks for paying their zakah.

1 INTRODUCTION

The Islamic Banking Roadmap (2015-2019)

describes several strategic issues that have an impact

on the development of Islamic banking, including

minimal capital and low efficiency. Policies are

needed to strengthen capital and improve efficiency.

To achieve optimal economies of scale, banking

corporations must increase core capital to more than

Rp. 5 T (Bank Indonesia Study), so that additional

funding sources are needed for the development of

Islamic banks. One of the potential sources of funds

that can be obtained by Islamic banks is zakah funds

from the public which will be channeled through the

Amil Zakah Agency (BAZ) or the Amil Zakah

Institution (LAZ).

Indonesia is a country with the largest Muslim

population in the world, and has a huge potential for

zakah. Indonesia's zakah potential reaches 1.7% of

2010 Gross Domestic Product (GDP) and it is

estimated that GDP will reach Rp. 21 thousand

Trillion in 2020, then the projection of national

zakah collection under the 2020 consolidation

program is equivalent to 30.3% of the national zakah

potential which at that time will reach Rp. 357

Trillion. According to National Amil Zakah Agency

(BAZNAS) data, the potential for zakah in Indonesia

is around Rp. 280 Trillion, but the collection of

zakah funds at the end of 2018 just reached Rp. 8.1

Trillion and in 2019 it increased to Rp. 10 Trillion.

However, if the data is compared to the total GDP of

Indonesia in 2019 which reached Rp. 15,834 trillion,

the realization of the collection of zakah funds will

only reach the equivalent of 0.06% of GDP.

However, the realization of the collection and

growth of Zakah funds in formal institutions for the

period 2014-2018 continues to increase by an

average of 25% per year. This shows that public

awareness is getting better in paying zakah through

official amil zakah institutions.

To increase the amount of zakah fund collection,

BAZ and LAZ must continue to collaborate with the

zakah stakeholders. One of the potential

breakthroughs is to take advantage of raising funds

through internet or online technology applications,

including the use of digital payment technology

provided by Islamic banks. Currently, several

Islamic banks have expanded digital innovation to

provide convenience for their customers to make

transactions, such as: Bank Muamalat with

Muamalat Din, Bank Syariah Mandiri with Mandiri

Syariah Mobile, BNI Syariah with Hasanah Mobile,

BRI Syariah with BRIS Online. According to

BAZNAS data, banking use as a method of paying

zakah in 2017 there were 133,202 transactions from

the total transactions or 89.3%. Then in 2018,

transactions with banks rose to 163,572 or 91.4%. In

2019, there was a decline in the use of banking

42

Syafrida, I., Aminah, I. and Awaludin, T.

Preferences of Islamic Commercial Bank Customers in Paying Zakah.

DOI: 10.5220/0010511200003153

In Proceedings of the 9th Annual Southeast Asian International Seminar (ASAIS 2020), pages 42-48

ISBN: 978-989-758-518-0

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

methods to 65,738 transactions or 79% (BAZNAS,

2020).

The rapid development of internet technology

allows transactions to be carried out online easily,

safely and quickly. The use of online and digital

channels has increasingly become a necessity for

zakah managers (BAZ and LAZ) so that access to

zakah fund collection is increasingly varied.

Although the existence of these online and digital

channels is relatively new for some people, seeing

the potential population in Indonesia which reaches

around 265 million and 132 million of them are

active internet users, online and digital payment

channels have enormous potential as alternative

channels in collect zakah funds. Zakah payer can

pay his zakah funds either offline, online, or through

the digital zakah application. Of course, in this case,

zakah payer have certain preferences that underlie

them in donating zakah online and digitally.

For this reason, Islamic banks need to identify

the use of online payment facilities, the types of

zakah paid, and the zakah payment facilities that are

most frequently used by their customers. Thus,

Islamic banks can take the right policy in collecting

zakah funds as a source of bank funds.

2 THEORY

Zakah is part of property with certain conditions

which Allah SWT obliges the owner to submit to

those entitled to receive it with certain conditions as

well. Pillars of zakah are the elements that must be

fulfilled before doing zakah. The pillars of zakah

include people who give zakah (zakah payer), assets

that are zakah, and people who are entitled to

receive zakah (mustahik).

"FinTech" or the combined term of Financial

Technology refers to an emerging industry using

technology-centered information technology and

aims to increase the efficiency of the financial

ecosystem. Since its inception, FinTech has

successfully established its presence in the global

financial industry due to the benefits and advantages

of its innovative technology systems. With the

development of financial services, advances in

information technology, and the evolution of the

financial sector, FinTech has become a new

opportunity in the financial industry. This platform

is expected to attract regulatory bodies, serve

industry and product services to understand

consumer behavior in order to gain a distinct

competitive advantage. In general, digitization and

technology have allowed the development of new

business models across industries. New entrants

have become challenging competitors due to low

cost operations, digital and connected offerings that

are changing industry dynamics, forcing different

ways to compete in existing businesses (Porter &

Heppelmann, 2014).

There are a number of previous studies related to

the preference or determination of zakah payer in

donating zakah, important factors in online and

digital application systems as well as perspective

and individual factors for zakah payer in paying

zakah, including: Durodolu (2016) research

investigates the Technology Acceptance Model

(TAM). The research results provide a deeper

understanding and development of TAM as a

suitable model for Communication and Information

Technology for Development (ICT4D) / social

informatics / community informatics studies and to

explain the relationship between Information

Literacy skills and technology acceptance. Other

research (bin Mohamed Fisol, bin Abdul Hamid, &

Cheumar, 2017) aims to investigate the relationship

between attitudes, subjective norms, perceived

behavioral control, levels of knowledge and

religiosity with Muslim intentions to use Islamic

cooperative products and services. The results

revealed that there was a significant relationship

between attitudes, subjective norms, perceived

behavioral control, level of knowledge and

religiousity with Muslim intentions to use Islamic

cooperative products and services.

Then the research of Ahmad, et al (2014) aims to

measure the awareness of the online e-zakah system

in Selangor and also to examine the extent to which

the use of online e-zakah among individual zakah

payers uses the Integrated Acceptance Theory and

Use of Technology (UTAUT) model. The results of

the research provide intellectual challenges and

contribute to knowledge in the area of user

perceptions of IT use and provide much-needed

evidence of the need to increase awareness and use

of online e-zakah. Meanwhile, other research (Al

Azizah & Choirin, 2018) provides discussion of

several issues related to financial technology as a

financial innovation that can be used in terms of

zakah disbursement in Indonesia. The research

results reveal that the determinants of Islamic

technology and finance encourage accelerating

economic growth and poverty alleviation.

The results of the research by Doktoralina,

Bahari, Abdullah (2018) present the factors that

determine the mobilization of zakah payments, for

example awareness, willingness to donate, trust in

collection and distribution with the latest

Preferences of Islamic Commercial Bank Customers in Paying Zakah

43

technological developments. This research uses

documentation analysis method. The factors that

influence mobilization are awareness, willingness to

donate, trust in collection and distribution with the

latest technological developments to help mobilize

income zakah payments at Zakah Institutions.

Friantoro & Zaki's research (2018) analyzes the

strengths, weaknesses, opportunities, and threats of

using financial technology to collect zakah in

Indonesia. Literature shows that there are always

opportunities for amil zakah institutions to use

financial technology to collect zakah because of the

power of information technology in the era of 4.0.

However, there are always threats and drawbacks to

using financial technology.

Then Hijriana & Nugroho's research (2018)

reveals that by using financial technology, financial

inclusion will increase and have a positive

correlation with the human development index. This

relationship will guide Indonesia to a state of zakah

optimization. Furthermore, Rachman & Salam's

(2018) reveals that financial technology or fintech,

as an information medium used to implement

technology-based financial services, has become a

great foundation in efforts to increase the

effectiveness and efficiency of financial services. An

integrated zakah management system has been

developed and needs innovation to be developed.

This means that fintech-based zakah management

will continue to grow and grow well, both on the

market and consumer side (especially for the

demand aspect), so that regulations, standardization

and efforts are needed to ensure zakah management

using fintech media.

Tantriana & Rahmawati's (2018) aims to identify

the level of preference of the people of Surabaya in

determining how zakah (payments made annually

based on Islamic law) on certain types of property

are used for charitable and religious purposes. Based

on the analysis, it is found that the variable

knowledge of zakah, the level of certainty and the

level of satisfaction has a significant effect on

muzaki preferences for zakah payments. Santoso

(2019) uses qualitative research methods with

SWOT analysis techniques to analyze corporate

strategy factors (strengths, weaknesses,

opportunities and threats). This study finds a

strategy to optimize zakah through improving the

management and information system about zakah-

based digitalization institutions. From the results of

previous studies, research has not been found that

specifically links the payment of zakah with the

banking industry, especially Islamic banks. This

study connects zakah funds with Islamic banks as

one of the channels for raising these funds.

3 METHOD

This research is a type of library research and survey

where the researcher first reviews the literature

which is closely related to the research problem. In

this study, the data used are secondary and primary

data. Secondary data were obtained from literature

books and journals which produced a number of

questions as a questionnaire. After that, the

researcher made a questionnaire and asked a number

of respondents to answer the questionnaire.

Respondents answered the questionnaire based

on Judgment Analysis in accordance with the

respondent's belief in the questions and statements in

the questionnaire. The questionnaire contains two

parts; the first part is designed to collect information

on status, education, employment, and income from

the sample. In the second part, contains information

on the use of online payments from Islamic bank

customers, the types of zakah paid, and the most

frequently used zakah payment facilities. The

questionnaire uses closed questions with choices and

also open-ended questions that can be filled in on

your own. Then the data from the questionnaire will

be analyzed descriptively to reveal data on the

characteristics of respondents and data related to the

research objectives. The next stage, the researcher

conducted the interpretation, conclusions and

research recommendations.

The research population is all customers of

Islamic banks in the Jabodetabek area. The sample

selection of research respondents was carried out by

purposive sampling and non-probability sampling.

Of the 250 questionnaires distributed, 201

questionnaires were received back, and 80

questionnaires were categorized as users of Islamic

banks. The research period is carried out for 3

months in 2020.

4 RESULT AND DISCUSSION

4.1 Responden Characteristics

The following is information about the status,

education, occupation, and income of the

respondents:

ASAIS 2020 - Annual Southeast Asian International Seminar

44

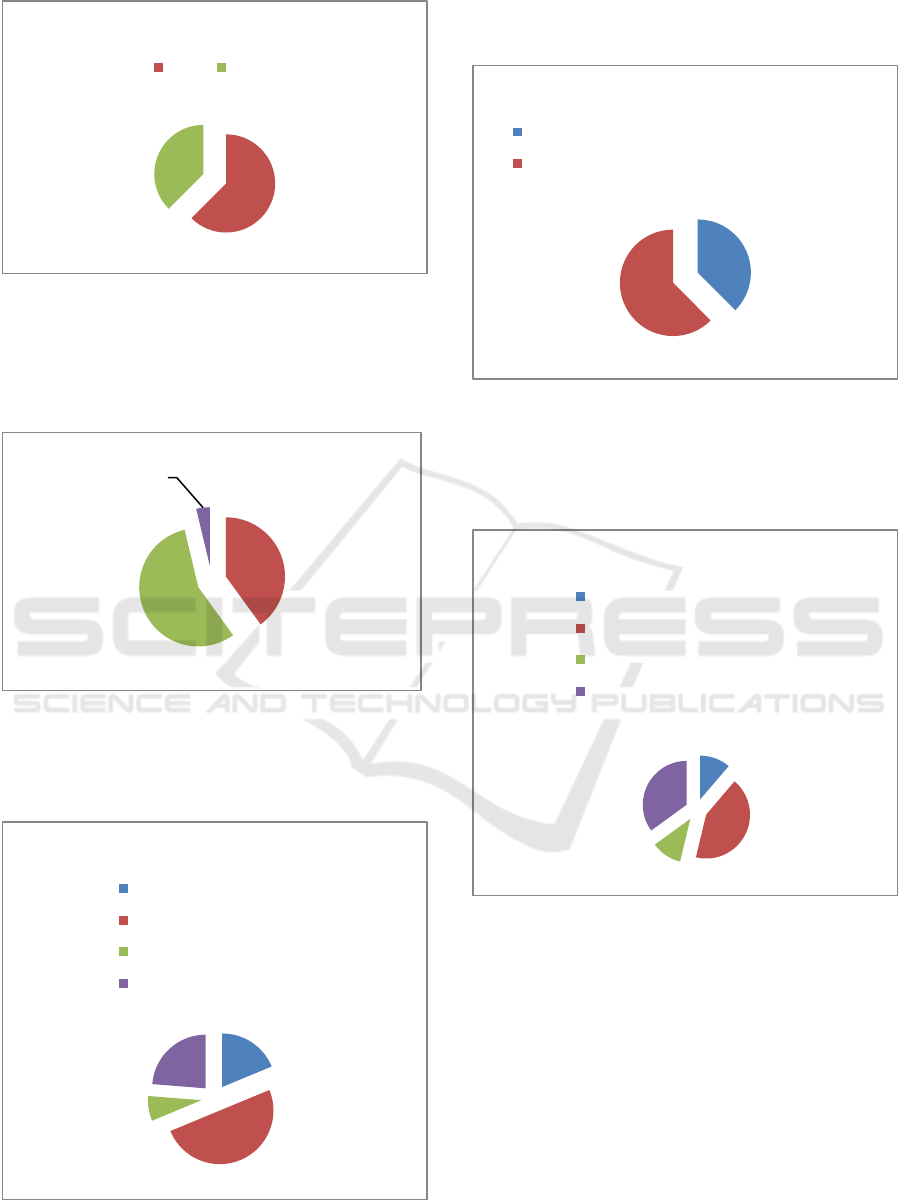

Figure 1. Sex

Based on the gender of the sample, it is known that

the most respondents who filled out the

questionnaire were male (62%).

Figure 2. Status

Based on their status, more than half of the

respondents were married (56%).

Figure 3. Education

The majority of respondents' last education was

undergraduate (50%).

Figure 4. Educational Background

More specifically (63%), the respondents' education

has a non-Islamic economic/ management/business

background.

Figure 5. Job

In terms of work, most of the respondents are private

permanent employees (43%).

62%

38%

Male Female

Single

40%

Married

56%

Widow/

Wodower

4%

19%

50%

7%

24%

Postgraduate

Undergraduate

Diploma

High school & equivalent

37%

63%

Islamic Economic/Management/Business

Non Islamic Economic/Management/Business

11%

43%

11%

35%

teacher / lecturer / researcher

private permanent employees

entrepreneur

other

Preferences of Islamic Commercial Bank Customers in Paying Zakah

45

Figure 6. Income

Based on the respondent's income data, it is known

that the most (33%) are above Rp. 4 million s.d. 8

million.

4.2 Respondent Online Payment

Transactions

Following are the results of a questionnaire related

to online payment transactions carried out by

customers of Islamic banks:

Figure 7. Electronic Card Usser

Based on data, it is known that the majority (66%) of

respondents are electronic card users, consist of:

BCA Flazz, Mandiri E-Money, BNI Tap Cash,

BRIZZI, Bank DKI Jackcard, and Indomaret Card.

Figure 8. Market Place User

Base on data from the use of market places, the

majority of respondents (94%) are already users of

market place transactions, those are Bukalapak,

Tokopedia, Lazada, Shopee, JD.ID, Tiket.com,

Traveloka, Airy, Pegipegi, RedDoorz, and Blibli.

Figure 9. Payment Fintech User

From the figure, it can be seen that in general the

respondents (74%) are users of payment features:

GoPay, OVO, DANA, T-Cash / Link Aja, Japri

apps, and cashbac.

4.3 Respondents' Zakah Payments and

Facilities

Data related to zakah paid and the channel of

payment often used by respondents based on the

questionnaire results:

30%

6%

33%

15%

16%

>Rp 10.000.000

Rp 8.000.001,- s.d Rp 10.000.000,-

Rp 4.000.001,- s.d Rp 8.000.000,-

Rp 2.000.001,- s.d Rp 4.000.000,-

< Rp 2.000.000

66%

34%

yes no

94%

6%

yes no

74%

26%

yes no

ASAIS 2020 - Annual Southeast Asian International Seminar

46

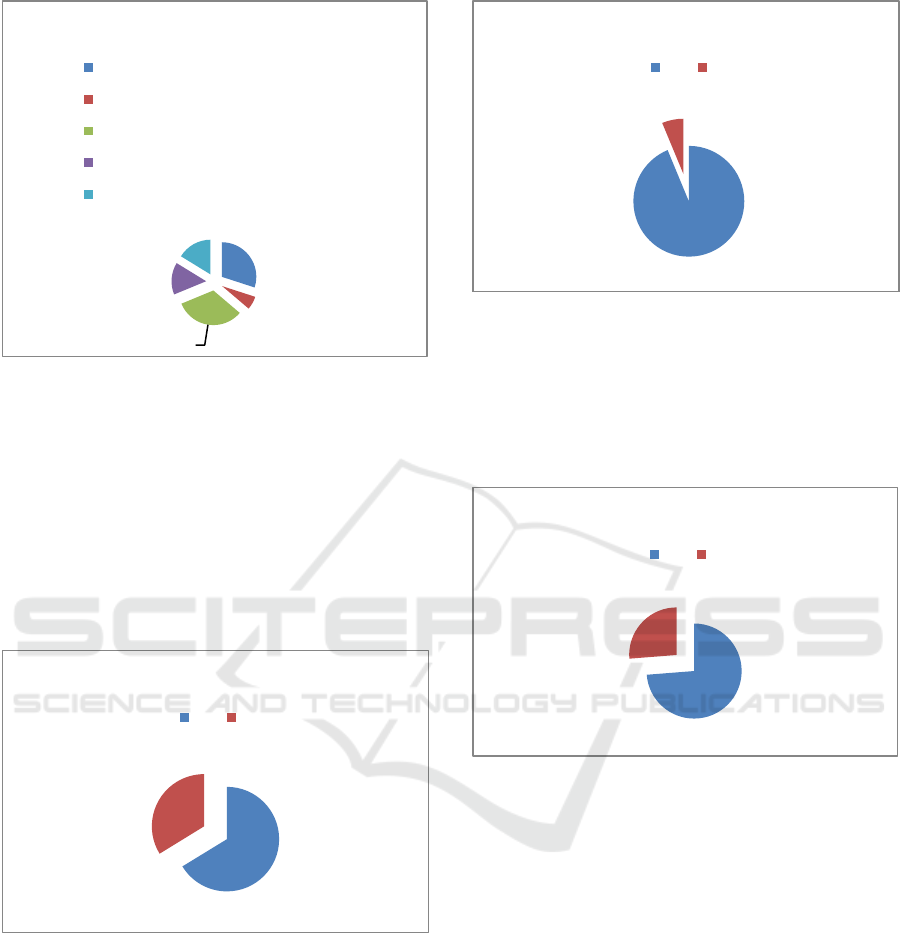

Figure 10. Frequencies of Zakah Payment

The majority of respondents (85%) always carry out

the obligation to give zakah.

Figure 11. Zakah on Asset

More of the respondents (60%) do not pay zakah of

property/maal.

Figure 12. Zakah on Income

More respondents do not pay zakah on income

(54%). The greatest potential of zakah comes from

zakah on assets and zakah on income. For this

reason, there is still a large opportunity for Islamic

banks to raise funds from its types of zakah

.

Figure 13. Favourite Zakah Distribution Channel

Based on the data, most respondents still use

payment by cash deposits through zakah

officers/volunteers, then online through ATM

transfers and direct distribution followed by online

via mobile/phone banking transfers. Very few

respondents use payment facilities through

technology service applications, both fintech and

market places. From research, no respondents have

even used the application provided by Islamic banks

for their zakah payments.

This data can provide information that modern

online payment applications are still not popular in

the public as a channel of paying zakah. Even

though the majority of people in the Jabodetabek

area have fintech applications and market places for

daily transactions payment.

5 CONCLUSION

The conclusion from the results of this study are:

1. The majority of Islamic bank customers have

used electronic money and payment fintech for

payment transactions. Almost all customers as

users of market place transaction. They are

already familiar with information/digital

technology.

2. There are many Islamic bank customers who

have not paid zakah on assets and zakah on

income. This indicates that there are still great

85%

15%

always ever

40%

60%

yes no

46%

54%

yes no

17%

14%

4%

3%

45%

1%

16%

online transfer by ATM

online transfer by mobile/phone banking

online transfer through ziswaf aplication

online through the technology service application

(Fintek) online shop / market place

cash deposit through zakat officers / volunteers

cash deposit via teller

direct distribution

Preferences of Islamic Commercial Bank Customers in Paying Zakah

47

opportunities for Islamic bank funding sources

from zakah.

3. In general, customers of Islamic banks pay

zakah by cash deposits through zakah

officers/volunteers, then direct distribution,

online transfer by ATM, and cash deposit via

teller. Very few zakah payer use payment

facilities through technology service

applications, both fintech and market places,

and this research no one has used applications

from Islamic banks for their zakah payments.

6 RECOMMENDATION

Recommendations to Islamic banks and Amil Zakah

Agencies/Amil Zakah Institutions are:

1. In terms of the high use of electronic money by

the public, Islamic banks need to innovate in the

form of providing machines for zakah payments

using electronic money and put them in the

public area such as shopping, parking, and gas

stasion area, specially in mosques.

2. Related to the low awareness of paying zakah on

asset and zakah on income, Islamic banks need

to collaborate with religious leaders toprovide an

understanding of the obligations of zakah on

asset and zakah on income.

3. Islamic banks need to collaborate with Amil

Zakah Agency/Amil Zakah Institution to

socialize online zakah payment channels that are

widely owned by the public and also use digital

platforms banking provided by almost all Islamic

banks.

ACKNOWLEDGEMENTS

We acknowledge the support of fund received from

Ministry of Research and Technology of Republik

Indonesia. I would also like to thanks Ministry of

Education and Culture of Republik Indonesia dan

Politeknik Negeri Jakarta for the research

opportunity.

REFERENCES

Ahmad, N. N., Tarmidi, M., Ridzwan, I. U., Hamid, M., &

Roni, R. (2014). The application of unified theory of

acceptance and use of technology (UTAUT) for

predicting the usage of E-Zakah online system.

International Journal of Science and Research (IJSR),

3(4), 63-70.

Al Azizah, U. S., & Choirin, M. (2018). Financial

Innovation on Zakah Distribution and Economic

Growth. In International Conference of Zakah.

bin Mohamed Fisol, W. N., bin Abdul Hamid, M., &

Cheumar, M. T. (2017). Determinant Factors

Muslim’s Intention To Use Islamic Cooperative

Products And Services: A Case Study In Southern

Thailand. The 3rdCHREST International Conference.

Doktoralina, C. M., Bahari, Z., & Abdullah, S. R. (2018).

Mobilisation of Income Zakah Payment In Indonesia.

Ikonomika, 3(2), 189-204.

Durodolu, O. O. (2016). Technology acceptance model as

a predictor of using information system'to acquire

information literacy skills. Library Philosophy and

Practice.

Friantoro, D., & Zaki, K. (2018). Do We Need Financial

Technology for Collecting Zakah?. In International

Conference of Zakah.

Hijriana, S., & Nugroho, V. A. (2018). Role of Financial

Technology in Zakah Optimization. In International

Conference of Zakah.

Porter, M. E., & Heppelmann, J. E. 2014. How smart,

connected products are transforming competition.

Harvard business review, 92(11), 64-88.

Rachman, M. A., & Salam, A. N. (2018). The

Reinforcement of Zakah Management through

Financial Technology Systems. International Journal

of Zakah, 3(1), 57-69.Syarifuddin, A. 2003. Garis-

Garis Besar Fiqh, Jakarta: Prenada Media, hlm. 40.

Santoso, I. R. (2019). Strategy for Optimizing Zakah

Digitalization in Alleviation Poverty in the Era of

Industrial Revolution 4.0. IKONOMIKA, 4(1), 35-52.

Tantriana, D., & Rahmawati, L. (2018). The Analysis of

Surabaya Muzaki’s Preference for Zakah Payment

through Zakah Digital Method. In International

Conference of Zakah.

ASAIS 2020 - Annual Southeast Asian International Seminar

48