The Influence of Emotional Intelligence and Spiritual Intelligence

towards the Understanding Level of Accounting

Ade Rizka Rahmad, Riri Zelmiyanti

Department of Business Management, Batam State Polytechnic, Batam, Indonesia

Jl. Ahmad Yani, Batam Center, Batam 29461, Indonesia

Keyword: Emotional Intelligence, Spiritual Intelligence, Accounting Understanding Level

Abstract: This study aims to determine whether there is an influence between emotional intelligence and spiritual

intelligence on the level of understanding of accounting. This study uses primary data in the form of a

questionnaire with a 5-point Likert scale and a 2-point Guttman scale. Criteria for respondents in this study

are students who had taken the Expertise Competency Test (UKK) at the Batam State Polytechnic. Emotional

intelligence in this study was measured by five indicators namely self-awareness, self-regulation, motivation,

empathy and social skills. Spiritual intelligence in this study was measured using the ability to be flexible,

self-awareness, the ability to deal with and utilize suffering, the ability to deal with and transcend pain,

the reluctance to cause unnecessary losses while accounting understanding was measured using the ability to

understand assets, liabilities and capital. The results of this study found that emotional intelligence has a

positive influence on the level of understanding of accounting and that spiritual intelligence has a positive

influence on the level of understanding of accounting. This study only uses the variables of emotional

intelligence and spiritual intelligence. Future studies are expected to add variables such as learning behavior

or learning interest.

1 INTRODUCTION

The competition in the world of work keep increasing

due to the era of the Asean Economic Community

(MEA). MEA is expected to be able to provide great

opportunities for Indonesian workers especially in the

accounting profession. MEA has positive and

negative impacts in the field of employment, positive

impacts in the form of employment opportunities and

negative impacts in the form of increasing

competition in the world of work. Various strategies

are carried out to survive in this era such as increasing

the competence of accountants. Good accountant

competency is not judged by the ability to think,

but also judged by how someone is able to control

their emotions and feelings and be able to adapt to

others.

There is an agreement in the MEA that

accountants become one of the professions

participating in free market competition

1

. Higher

education as an institution appointed to educate

students to work as a Professional Accountant.

Professional means that an accountant is able to

understand the accounting profession correctly.

Students are now accustomed to memorizing learning

patterns so that it is difficult to understand correctly

what has been learned. This was proven during the

Expertise Competency Test (UKK) at Batam State

Polytechnic. There are 320 students who took the

competency examination but only 180 students have

passed and are competent even though they are

known to have high GPA scores. So, it can be

concluded that the students who did not pass were

43.75 percent.

Accounting is an activity of identifying,

measuring, and reporting economic-related

information, so it is not only related to numbers but

also related to reasoning that requires logic.

Reasoning can be obtained by an accountant if he

has an understanding of accounting. Understanding

of accounting can be seen from the level of

intelligence in understanding and knowing about

accounting. The level of understanding of accounting

is influenced by three factors namely intellectual

intelligence, emotional intelligence and spiritual

intelligence (Prasetyaningsih, 2018). Emotional

192

Rahmad, A. and Zelmiyanti, R.

The Influence of Emotional Intelligence and Spiritual Intelligence towards the Understanding Level of Accounting.

DOI: 10.5220/0010356001920199

In Proceedings of the 2nd International Conference on Applied Economics and Social Science (ICAESS 2020) - Shaping a Better Future Through Sustainable Technology, pages 192-199

ISBN: 978-989-758-517-3

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

intelligence is one of the factors that can influence the

level of understanding of accounting. Emotional

intelligence is related to one's ability to control

emotions, motivate themselves, have a sense of

empathy and encourage others to succeed. Research

conducted by Alam & Ahmad (2017) proves that

teachers are able to improve student learning

achievement, one of which i

s because there is high emotional intelligence in

themselves. The results of the study also prove the

teacher will do teaching in more effective ways so

as to facilitate his students in accepting lessons, this

proves that emotional intelligence has an important

role in improving student achievement.

There are other factors that can improve

accounting understanding, namely spiritual

intelligence. Spiritual intelligence is one's expertise

in interpreting life by giving a positive value in every

problem that occurs. Giving positive values can

awaken the soul to take positive actions. Research by

Hersan (2010) proves that low spiritual intelligence

will present a lazy generation, easily discouraged and

hard to get along with. This causes a lack of

motivation to learn so that difficulties in

understanding the lesson. Students who only pursue

grades tend to take various actions to get good grades

including cheating during exams so that students

ignore their spiritual values.

In addition to emotional and spiritual

intelligence, there are other factors that can affect

the level of understanding of accounting namely

intellectual intelligence. Intellectual intelligence is a

person's intelligence in thinking, reasoning, and

problem solving. Research conducted by Satria &

Fatmawati (2017) proves that someone who has high

intellectual intelligence (IQ) is easier to understand

and understand accounting. In line with Pasek's

(2016) research in testing intellectual intelligence

influences the understanding of accounting. The

results show that intellectual intelligence on

accounting understanding has a positive impact.

Research that discusses intellectual intelligence on

accounting understanding has been carried out and

the results are always positive.

Other research related to emotional intelligence

and spiritual intelligence conducted by Fahrianta,

Sham, & Syahdan, (2012) the results prove emotional

intelligence, spiritual intelligence has a positive

effect on accounting understanding. Different results

are obtained from research conducted by Rimbano &

Putri (2016) which shows emotional intelligence on

accounting understanding has a positive impact, but

does not have a positive effect on spiritual

intelligence. There is a difference between the two

causes researchers want to reexamine emotional

intelligence, spiritual intelligence on the level of

understanding of accounting.

This research is a development of Rodrigues,

Jorge, Pires, & Antonio (2019) who tested spiritual

intelligence and emotional intelligence in

understanding the creativity and entrepreneurial

intentions of higher education students. The

difference between this research and the previous

one is that the first researcher examined creativity and

entrepreneurial intentions while this research

examined the level of understanding of accounting.

Another fundamental reason for conducting this

research is because it saw the results of the Expertise

Competency Examination (UKK) in Batam State

Polytechnic which reached 43.75 percent who did not

pass. Based on the description that has been

described, researcher takes the title of the research

"The Influence of Emotional Intelligence and

Spiritual Intelligence towards the Understanding

Level of Accounting".

2 LITERATURE REVIEW AND

HYPOTHESIS

2.1 Theory of Planned Behavior

The theory of planned behavior is a theory that arises

because there is a direct intention to behave, the

theory explains or controls a person's behavior

(Ajzen, 1991). According to (Ajzen, 1991) a person's

intention towards behavior is thought to be due to

three factors consisting of attitudes towards behavior

(attitude toward the behavior), subjective norms, and

perceived behavioral control (Ajzen, 1991).

2.2 Understanding of Accounting

Understand according to Indonesia Dictionary has a

meaning as clever or true understanding, while

comprehension is an act of understanding. So, it can

be interpreted that understanding accounting is a

person's ability to understand and understand

correctly about accounting. Accounting

understanding in this study was measured using an

understanding of assets, liabilities and capital.

2.3 Emotional Intelligence

Emotional intelligence is intelligence that is related

to one's ability to control emotions, motivate yourself,

The Influence of Emotional Intelligence and Spiritual Intelligence towards the Understanding Level of Accounting

193

have a sense of empathy and encourage others to

succeed. Indicators of emotional intelligence

according to (Goleman, Boyatzis, & Boston, 2002),

namely:

a. Self awareness means that the individual knows

or is aware of his own situation.

b. Self-management (self management) means that

the individual is able to regulate and control the

situation in him.

c. Motivation (motivation) means that the

individual is able to motivate himself to achieve

goals.

d. Empathy (empathy) means individual awareness

of the feelings, interests and interests of others.

Empathy is the sympathy that one has towards

others.

e. Social skills (social skills) means the ability to

build responses in accordance with the wishes of

others. Social skills are more related to how one

can easily understand the feelings of others.

2.4 Spiritual Intelligence

Spiritual intelligence is someone's expertise in

interpreting life by giving a positive value in every

problem that occurs. Giving positive values can

awaken the soul to take positive actions. Indicators

of spiritual intelligence according to (Zohar &

Marshall, 2001):

a. The ability to be flexible is one's ability to adjust

spontaneously and actively in achieving the

results to be achieved.

b. Self-awareness is a person's ability to face and

realize the situation that comes with him.

c. The ability to deal with and take advantage of

suffering is one's ability to remain strong in

dealing with each problem encountered and take

lessons from each of these problems.

d. The ability to deal with and surpass pain is the

ability of someone who does not want to add to

the problem and spread hatred against others so

that they try to hold back anger.

e. The reluctance to cause unnecessary loss, that is

someone who always thinks before acting so that

undesirable things do not happen.

2.5 Hypothesis Development

2.5.1 Effects of Emotional Intelligence and

Understanding Level of Accounting

Research conducted by Alam & Ahmad (2017)

proves that teachers with high emotional intelligence

can improve student learning achievement. The

results of the study also prove that high emotional

intelligence in teachers can teach in more effective

ways, making it easier for students to receive lessons.

Indirectly students who have emotional intelligence

in themselves will always be motivated to learn so

that it is easy to understand the lesson. Conversely, if

students do not have emotional intelligence in

themselves, they will not be motivated to learn and

understand accounting. Based on the description

above, the first hypothesis can be drawn as follows:

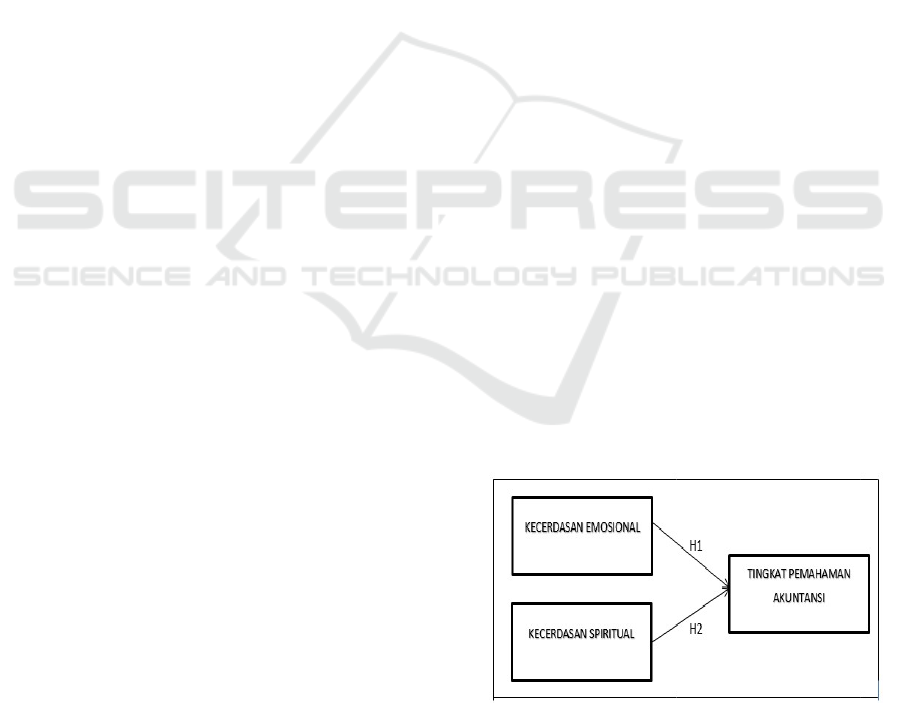

H1: Emotional Intelligence Has a Positive Impact

on Understanding Level of

Accounting.

2.5.2 Effects of Spiritual Intelligence and

Understanding Level of Accounting

Research conducted by Hersan (2010) proves that

low spiritual intelligence will produce a generation

that is easily discouraged, depressed and like fighting.

This causes a lack of motivation to learn so that

difficulties in understanding the lesson. Students

who only pursue achievement values in the form of

numbers tend to try to get good grades including

cheating during exams so that they ignore their

spiritual values. The research also proved that high

spiritual intelligence can encourage students to study

hard and have creativity. Based on these studies it can

be concluded that having high spiritual intelligence

can take positive actions and will consider which

things are good or bad on him.

H2: Spiritual Intelligence Has a Positive Impact

on Understanding Level of

Accounting.

Based on the description of the development of

the hypothesis that has been described, then the

hypothesis model in this study is as follows:

Figure 1. Hypothesis Research Model Source: self-

processed (2020)

ICAESS 2020 - The International Conference on Applied Economics and Social Science

194

3 METHOD

This research uses a quantitative method approach

because there is hypothesis testing. This study uses

primary data where the data is collected by itself and

obtained directly from the object. This data collection

is done in two ways namely first, giving

questionnaires to the object of research and filled

directly by the respondent. Second, the distribution of

questionnaires using an online system (Google

Form). The population in this study are Batam State

Polytechnic students who have taken the Expertise

Competency Test (UKK). The sample used in this

study was 76 students from 2015 to 2016. The

instrument in this study used 52 questions that were

modified from research conducted by Zakiah (2013),

Saputra (2018) and Juniarti (2014). The

measurements in this study use a Likert Scale and

Guttman Scale. The sample selection technique in

this study is simple random sampling, because every

population has the same opportunity to become a

research sample.

3.1 Data Processing and Analysis

Techniques

Data processing techniques in this study using SPSS

26.0. Analysis of the data used is descriptive

statistical analysis, validity and reliability, classic

assumption tests consisting of normality and

heteroscedasticity tests, simple linear regression

analysis. The simple linear regression analysis

equation model is as follows:

PA = α+β1KE+е………………………(H1)

PA = α+β1KS+е………………..……..(H2)

Keterangan:

PA =Understanding Accounting

α =Constant

β1,β2 =Regression coefficient for KE & KS

variables

KE =Emotional Intelligence

KS =Spiritual Intelligence

е =Eror

4 RESULTS AND DISCUSSION

4.1 Characteristics of Respondents

The sample used in this study was the students of

Batam State Polytechnic accounting and managerial

accounting courses for the 2015 and 2016. The

sample of this study amounted to 76 respondents. The

respondents who filled out the questionnaire were 80

respondents, but found incomplete data of 4

respondents. Based on this, the sample that met the

study criteria amounted to 76 respondents.

The description of respondent characteristics can

be seen in table 1 below:

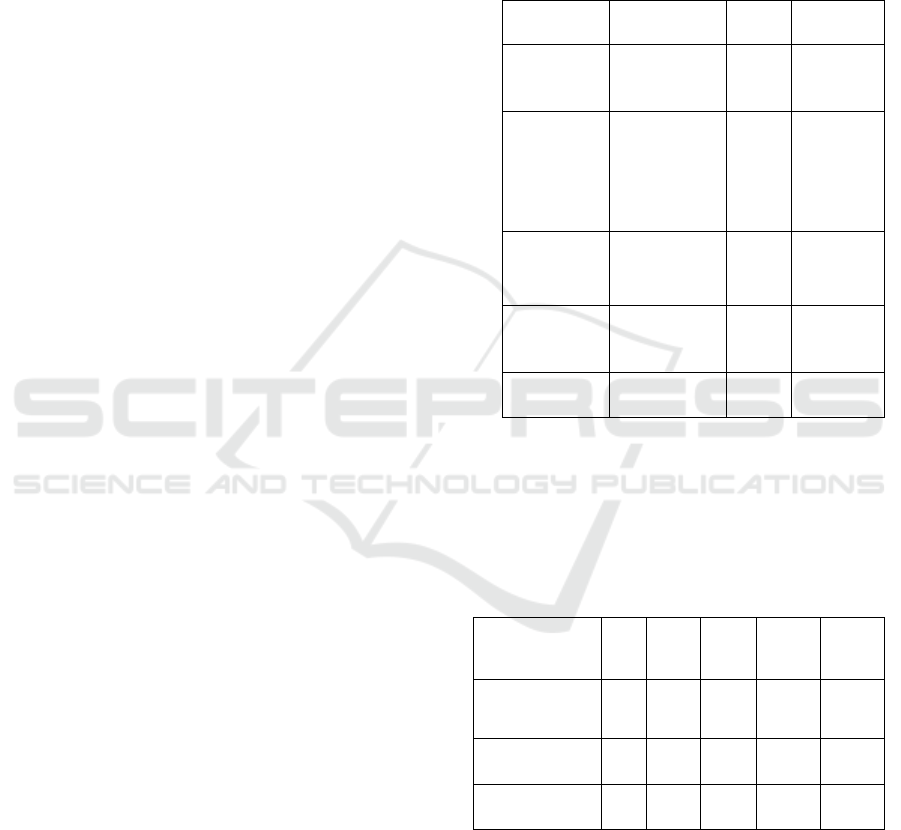

Table 1 Characteristics of Respondents

Criteria

for

Respondents

Total

Percentage

Gender

Male

Female

14

62

18.4%

81.5%

Age

20

years

21

years

22

years

23

years

1

48

24

3

1.3%

63.1%

31.5%

4.0%

Program

Study

Accounting

Managerial

Accounting

18

58

23.6%

76.3%

Year of

the

Force

2015

2016

14

62

18.4%

81.5%

Number

of

Samples

76

100%

Source: self-processed data (2020)

4.2 Descriptive statistics

Descriptive statistical data of each variable to be

analyzed in this study can be seen in table 2 below:

Table 2 Descriptive Statistics

N

M

in

M

ax

The

mean

S

td. Dev

Understanding o

f

Accounting

76

9

22

17.38

2,941

Emosioanal

Intelligence

76

34

93

75.16

8,767

Spiritual

Intelligence

76

24

55

45.30

4,702

Source: Data processed from SPSS V. 26

Based on table 2 it can be seen that the accounting

understanding variable has a mean value of 17.38 and

a standard deviation of 2.941. These results state that

the mean value is greater than the standard deviation

so it can be concluded that the evaluation of

accounting understanding has a high variation of

The Influence of Emotional Intelligence and Spiritual Intelligence towards the Understanding Level of Accounting

195

responses. Accounting understanding also has the

lowest value of 9 and the highest value of 22.

Based on table 2 it can be seen that the

emotional intelligence variable has a value the

mean75.16 and the standard deviation of 8.767. These

results state that the mean value is greater than the

standard deviation so it can be concluded that the

evaluation of accounting understanding has a high

variation of responses. Emotional intelligence also

has the lowest value of 34 and the highest value of

93.

Based on table 2 it can be seen that the spiritual

intelligence variable has a value the mean45.30 and

the standard deviation of 4.702. These results state

that the mean value is greater than the standard

deviation so it can be concluded that the evaluation

of accounting understanding has a high variation of

responses. Spiritual Intelligence also has the lowest

value of 24 and the highest value of 55.

4.3 Validity and Reliability Test Results

The results of each indicator of the questions of

emotional intelligence, spiritual intelligence and

accounting understanding in this study are valid and

reliable.

4.4 Classic Assumption Test

4.4.1 Normality Test

The normality test that can be used is the One Sample

Kolmogorov - Smirnov Test. In this test normally

distributed if the significant value> 0.05 or 5%. The

following results are tested in table 3:

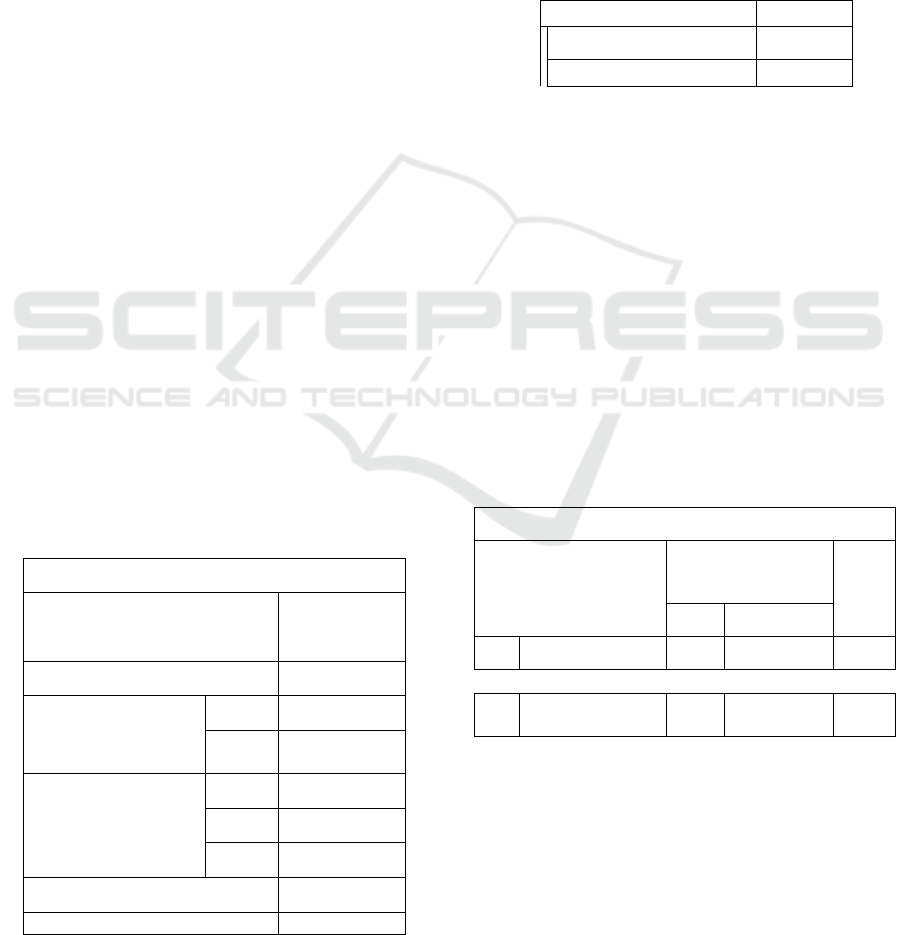

Table 3 Normality Test

One-Sam

p

le

K

olmo

g

orov-Smirnov Test

Unstandardized

Resi

d

ual

N

76

N

ormal

Parameters

a,b

Mean

.0000000

Std.

De

v

iation

1.69143235

Most Extreme

Differences

Absolute

.083

Positive

.080

N

e

g

ative

-.083

Test Statistic

.083

Asymp. Sig. (2-tailed)

.200

c,d

Based on the data above, it can be seen that the value

of Asymp.sig: (2 tailed) is 0,200. This shows that the

significant value is greater than 0.05, which means

the data is normally distributed.

4.4.2 Heteroscedasticity Test

Heteroscedasticity test was performed using the

Glejser test. If the significance value is greater than

0.05, it is free from heteroscedasticity. The following

test is in table 4:

Table 4 Heteroscedasticity Test

Va

r

ia

b

el Signifikan

S

p

i

r

itual Intelli

g

ence

.578

Emotional Intelligence .175

Source: data processed from SPSS 26

Based on the above data it can be seen that the

significant value of the correlation results from each

variable is greater than 0.05. This shows that the

emotional intelligence and spiritual intelligence that

are tested are free from heteroscedasticity.

4.5 Hypothesis Testing Results

Simple linear regression analysis is used to determine

the direction of the relationship between the

independent variable and the dependent variable. The

results of simple linear regression calculations can be

seen in Tables 5 & 6 below:

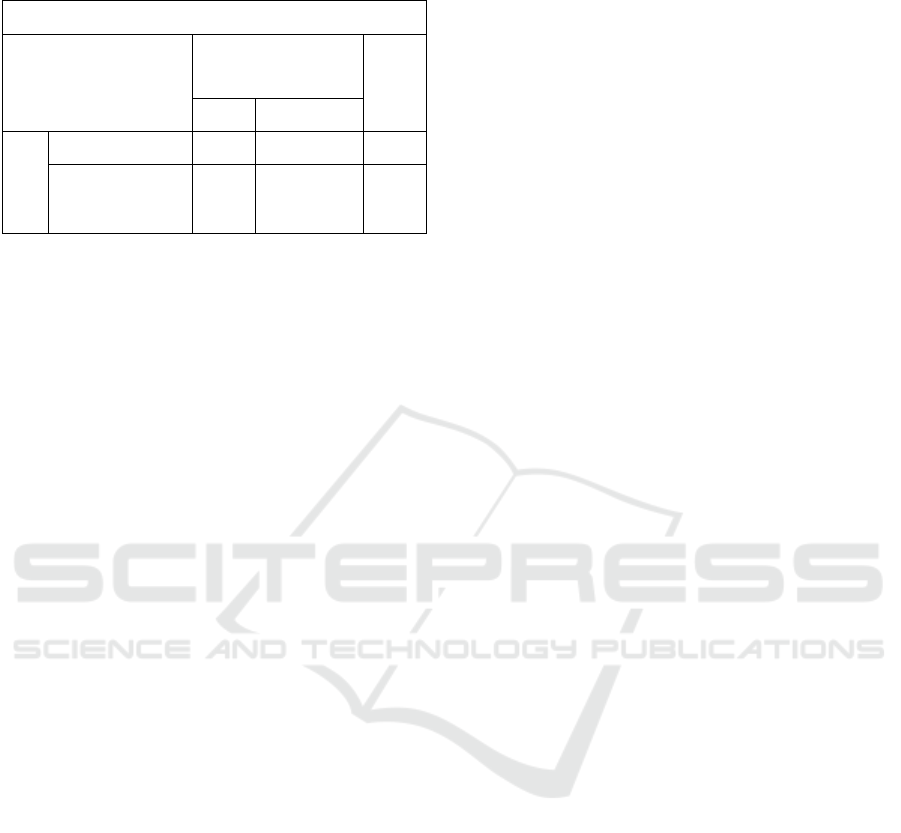

Table 5 Test Results of Simple Linear Regression Analysis

(Emotional Intelligence)

Coefficientsa

Model

Unstandardized

Coefficients

Si

g

.

B

Std. Error

1 (Constant) 9,861

1,701

.000

Emotional

Intelligence

.079 .22 .001

Source: data processed from SPSS 26 (Spiritual

Intellegence)

ICAESS 2020 - The International Conference on Applied Economics and Social Science

196

Table 6 Testing Results of Simple Linear Regression

Analysis (Spiritual Intelligence)

Coefficients

a

Model

Unstandardized

Coefficients

S

ig

B

Std. E

r

r

o

r

1

(

Constant

)

9.570

1.929

.000

Spiritual

Intelligence

.137

.042

.002

Source: data processed from SPSS 26

Emotional intelligence has a positive effect on the

level of understanding of accounting

Y = 9,861 + 0,079 + e

Based on table 5 shows that the significant value

for emotional intelligence is 0.001 with a probability

value of 0.05. Significantly smaller value than the

probability value (0.001 <0.05) indicates that

emotional intelligence has a positive influence on

the level of understanding of accounting, so it can

be concluded that H1 supported.

Spiritual intelligence has a positive effect on the

level of understanding of accounting

Y = 9,570 + 0,137 + e

Based on table 6 shows that the significant value

for spiritual intelligence is 0.002 with a probability

value of 0.05. Significant value smaller than the

probability value (0.002 <0.05) shows that spiritual

intelligence on the level of accounting understanding

has a positive effect, so it can be concluded that H2

is supported.

5 CONCLUSIONS

Based on the discussion that has been presented, the

conclusion is:

1. Emotional intelligence has a positive effect on

the level of understanding of accounting. Because

someone who has emotional intelligence on

himself he will be motivated to be able to

understand and understand accounting,

conversely if someone has no motivation in

themselves then he will be lazy to understand

accounting, it proves that emotional intelligence

is also needed in improving accounting

understanding.

2. Spiritual intelligence affects the level of

understanding of accounting. Because someone

who has spiritual intelligence on himself he will

always take positive action. Positive activities

such as learning to understand accounting and stay

away from negative things such as cheating, it can

improve students' understanding of accounting.

5.1 Limitation

This study has several limitations that require

improvement in further research. These limitations

include: (1) In this study only questionnaires were

distributed at the Batam State Polytechnic. (2)

Accounting understanding in this study is only

measured by two variables namely emotional

intelligence and spiritual intelligence. (3) The

population in this study is not extensive or limited.

5.2 Implications and Suggestions

The implication of this study consists of two namely

(1) the results of the study can be used as additional

literature for further research. (2) the results of this

study prove that emotional intelligence and spiritual

intelligence can influence accounting understanding.

Suggestions that the authors propose for further

research: (1) Future studies should increase the

number of research samples to make it wider. (2)

Further research is suggested to add variables such

as learning interest. (3) Future studies are suggested

to broaden the scope of respondents to make it easier

for researchers to get data.

REFERENCES

Agustian, AG (2003). The Secret to Success Generating

ESQ Power. Jakarta: Arga. Ajzen, I. (1991). The

Theory of Planned Behavior. Organizational Behavior

and Human Decision Processes, Volume 50 Issue: 02,

179-211.

Ajzen, I. (1991). Attitudes, Personality, and Behavior.

Organizational Behavior and Human Decision

Processes, 50 (2), 179-211.

Alam, A., & Ahmad, M. (2017). The role of teachers'

emotional intelligence in enhancing student

achievement. Journal of Asia Business Studies, Vol.

12 No. 1, 31-43.

Anam, H., & Ardillah, L. (2016). The Influence of

Emotional Intelligence, Intellectual Intelligence, Social

Intelligence on Accounting Understanding. JOURNAL

OF SCIENCE APPLIED NO. 1 VOL. 2, 1-8.

Ananto, H. (2010). Influence of Emotional Intelligence and

Spiritual Intelligence on the Understanding of

The Influence of Emotional Intelligence and Spiritual Intelligence towards the Understanding Level of Accounting

197

Accounting. Thesis Muhammadiyah University

Surakarta.

Artana, BM, Herawati, NT, & Wait for Atmdja, AW

(2014). The Influence of Intellectual Intelligence (IQ),

Emotional Intelligence (EQ), Spiritual Intelligence

(SQ) And Learning Behavior of Accounting

Understanding. e-journal S1 Ak Universitas Pendidikan

Ganesha Vol.2 No.1, 1-11.

Basuki, KH (2015). The Effect of Spiritual Intelligence and

Learning Motivation of Mathematical Learning

Achievements. Formative Journal 5 (2), 120-133.

Cherniss, C., & Goleman, D. (2003). The Emotionally

Intelligent Workplace. San Francisco, CA 94104:

JOSSEY-BASS A Wiley Company.

Chotimah, C., & Rohayati, S. (2015). The Influence of

Financial Education in the Family, Parent's Social

Economy, Financial Knowledge, Spiritual Intelligence,

and Peers to the Primary Financial Management of S1

Accounting Education Faculty Students in Economics.

Journal of Accounting Education (JPAK) Vol 3, No.02.

Fahrianta, RY, Syam, AY, & Syahdan, SA (2012). The

Influence of Emotional Intelligence and Spiritual

Intelligence of Accounting Students on the

Understanding of Accounting. Journal of the

Socioscientia Kopertis Region XI Kalimantan, Vol 04

No.02, 187-374.

Ghozali, I. (2016). Multivariate Analysis Application with

IBM SPSS 23. Semarang: BPFE Diponegoro

University.

Goleman, D. (2015). Emotional Intelligence. Jakarta: PT

Gramedia Jakarta.

Goleman, D., Boyatzis, R., & Boston, AM (2002). Primal

Leadership Realizing the Power of Emotional

Intelligence. The Harvard Business Review Press, 352.

Gomes, FC (1995). Human Resource Management.

Yogyakarta: Andi Offset.

Herlinda, MS (2016). Effects of Emotional

Intelligence, Spiritual Intelligence, Social Intelligence and

Learning Behavior on Accounting Understanding

Levels. Student Scientific Articles.

Hersan, A. (2010). Effect of Emotional Intelligence and

Spiritual Intelligence on Accounting Understanding.

Thesis, Muhammadiyah University, Surakarta.

Hernita, N. (2019). Effects of Emotional Intelligence and

Learning Interest on Accounting Understanding Level

(Case Study in Accounting Students of the Faculty of

Economics and Business, University of Lampung).

Thesis of the Faculty of Economics and Business

Bandar Lampung, 1-58.

Idrus, M. (2002). Spiritual Intelligence of Yogyakarta

Students, Psychology Psychology. Scientific and

Applied Journal, Vol. 4, No. 8, 72-91.

Juniarti, E. (2014). Analysis of Accounting Students

Understanding Level of Basic Accounting Concepts at

the Faculty of Economics, Muhammadiyah University,

Palembang. Thesis, Faculty of Economics.

Laksmi, RA, & Sujana, K. (2017). Effects of Intellectual

Intelligence, Emotional Intelligence and Spiritual

Intelligence on Accounting Understanding. E-journal

of Udayana University Accounting Vol. 21, 1373-1399.

Lazarus, RS (1993). Emotion And Adaption. From

Psychological Stress to the Emotions. 1-21.

Mangkunegara, AP (2000). HR Performance Evaluation.

Bandung: PT Refika Aditama.

Pasek, NS (2016). Effect of Intellectual Intelligence on

Accounting Understanding with Emotional Intelligence

and Spiritual Intelligence as Moderating Variables.

Scientific Journal of Accounting. Vol. 1 No. 1, 62-76.

Pramesti, G. (2014). Peel Completed Research Data With

SPSS 22. Jakarta: PT Gramedia. Prasetyaningsih, E.

(2018). Analysis of Factors Affecting Accounting

Understanding Level. Thesis Muhammadiyah

University Surakarta, 1-17.

Rimbano, D., & Putri, MS (2016). Effects of Emotional

Intelligence, Spiritual Intelligence and Learning

Behavior on Accounting Understanding Levels.

Scientific Journal of Business Oration.

Riswandi, P., & Lakoni, I. (2017). The Influence of

Emotional Intelligence, Spiritual Intelligence and

Intellectual Intelligence on Understanding of

Introductory Subjects in Accounting with Learning

Behavior as Moderation Variables in PTN and PTS

Bengkulu City. Journal of Accounting Science Vol.1

No.2, 1-16.

Rodrigues, AP, Jorge, FE, Pires, CA, & Antonio, P. (2019).

The contribution of emotional intelligence and

spirituality in understanding creativity and

entrepreneurial intention of higher education students.

Education + Training, Vol. ahead-of-print No. ahead-

of-print.

Rubiah, S. (2013). Analysis of the Effect of Understanding

of Accounting, Conditional Subjects and Educational

Background on GPA of Accounting Department

Students at the Faculty of Umrah Economics. Umrah

Journal, 1-18.

Saputra, KT (2018). Influence of Emotional Intelligence,

Spiritual Intelligence and Intellectual Intelligence,

Against the Level of Accounting Understanding.

Thesis, Lumbung Pustaka Yogyakarta State University.

Satria, MR, & Fatmawati, AP (2017). The Effect of

Emotional Intelligence on Accounting Understanding

Levels of Accounting Students in Bandung City.

Journal of Islamic Economics and Finance, Vol.01

No.1, 66-80.

Sina, PG, & Noya, A. (2012). Effects of Spiritual

Intelligence on Personal Financial Management.

Management Journal Vol.11 No.2.

Sinarti, & Sari, UM (2016). The Effect of Emotional

Intelligence on Accounting Understanding from a

Gender Perspective. Batam State Polytechnic

Repository.

Sucipto, TI (2017). Effects of Intellectual Intelligence,

Emotional Intelligence, Spiritual Intelligence and

Demographic Factors on Student Ethics. Batam State

Polytechnic Repository.

Sugiyono, PD (2014). MANAGEMENT RESEARCH

METHOD, 3rd Printing Bandung: CV. ALFABETA.

Susanti, FR (2016). The Influence of Emotional

Intelligence and Spiritual Intelligence on Accounting

Student Understanding Level of Accounting Education

ICAESS 2020 - The International Conference on Applied Economics and Social Science

198

Study Program, Faculty of Economics, State University

of Surabaya Journal of Accounting Education (JPAK)

Vol.4 No.3.

Trisnawati, IE, & Suryaningrum, S. (2003). The Influence

of Emotional Intelligence on the Understanding of

Accounting. Journal of Management Accounting 6 (5),

1073-1091.

Zakiah, F. (2013). Effects of Intellectual Intelligence,

Emotional Intelligence and Spiritual Intelligence on

Accounting Understanding. Thesis, i-121.

Zohar, D., & Marshall, I. (2001). SQ: Utilizing SQ in

Holistic Thinking to Mean Life. Mizan

The Influence of Emotional Intelligence and Spiritual Intelligence towards the Understanding Level of Accounting

199