The Effect of Tax Planning on Financial Performance of

Manufacturing Companies in Indonesia

Elisabeth Cindy Laurencia, Diah Amalia

Jurusan Manajemen Bisnis, Akuntansi Manajerial, Politeknik Negeri Batam,, Batam, Indonesia

Keywords: Tax planning, financial performance, ETR Cash, & ETR.

Abstract: This study aims to examine the effect of tax planning on the financial performance of manufacturing

companies in Indonesia. This study uses secondary data obtained from the financial statements of

manufacturing companies listed on the Indonesia Stock Exchange (IDX) for the 2014-2018 period. By using

a purposive sampling method, 245 samples were obtained. Data analysis conducted in this study is panel data

using Ordinary Least Square (OLS). The proxy of tax planning in this study uses Cash ETR & ETR and ROA

as a proxy for financial performance. The results of this study indicate the influence of tax planning on the

performance of manufacturing companies in Indonesia.

1 INTRODUCTION

Sustainable development in Indonesia is carried out

to support and improve the prosperity of the people.

State development relies on the State Budget (APBN)

as the main source of financing. In order to achieve

this goal, issues concerning financing of state

development need to be solved. Tax revenue is the

main income from domestic revenue in state

financing for state expenditure and development.

According to the state budget data for the previous 5

years

1

, in 2014 tax revenues accounted for 76%, 85%

in 2015,2016, 2018, and 86% in 2017.

Taxes, for companies, are considered as expenses

or costs that affect the income received by the

company in carrying out operational activities.

Assumptions of tax as expenses will affect earnings,

while taxes as profit distribution will affect the rate of

return on investment (Suandy, 2011). Taxes that

affect profits can be minimized through tax

management, and a reduction in corporate tax burden

can be done with tax management.

Tax planning in tax management refers to the

process of planning business and taxpayer

transactions so that tax debt becomes less but still

within tax regulations. Companies are able to

minimize many tax burdens and increase company

profits with ideal planning. Hoffman (1961), taxation,

1

Can be accessed at

https://www.kemenkeu.go.id/apbn2018

is largely based on business or accounting concepts,

so companies can modify activities such as towards

achieving tax liability reduction (Ogundajo &

Onakoya, 2016).

Research from Ogundajo & Onakoya (2016)

conducted in Nigeria with a sample of 10 of the 28

manufacturing companies in the annual consumer

goods sector showed that increasing ETR has a

reduction in ROA. Feng, Habib, & Tian's research

(2019) conducted in China found a positive and

significant relationship between aggressive tax

planning variables and share price synchrony

variables.

In contrast to previous research, Kristianto,

Andini, & Santoso (2018) explained that tax planning

has no direct effect on firm value. Yuliem (2018) also

states that tax planning does not affect firm value,

which means high or low company value does not

affect the high or low influence of tax planning

This research is a development of previous

research conducted by Ogundajo & Onakoya (2016).

The Ogundajo & Onakoya study (2016) took place in

Nigeria with a population of 28 research companies

manufacturing the annual consumer goods sector and

only previous studies used ETR as a measurement of

tax planning. This study took a research population of

166 companies listed on the Indonesia Stock

186

Laurencia, E. and Amalia, D.

The Effect of Tax Planning on Financial Performance of Manufacturing Companies in Indonesia.

DOI: 10.5220/0010355801860191

In Proceedings of the 2nd International Conference on Applied Economics and Social Science (ICAESS 2020) - Shaping a Better Future Through Sustainable Technology, pages 186-191

ISBN: 978-989-758-517-3

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

Exchange. Another difference lies in the

measurement of tax planning using ETR & CETR.

2 THEORY BASIS

2.1

EMH (Efficient Market

Hypothesis)

Fama (1970) in Sujana (2017) defines an efficient

market is a security market said to be efficient if the

prices of securities fully reflect the available

information. The information classification

concludes that there are three forms of efficient

capital markets, namely (1) a weak form of

efficiency, which is a situation where the stock price

reflects all the information in the past price record; (2)

a half-strong form of efficiency, i.e. prices also reflect

all information published not just past prices; and (3)

strong form of efficiency, i.e. all relevant information

available is reflected in the stock price.

2.2 UU No. 36 of 2008

UU No. 36 of 2008 is the fourth amendment to UU

No. 7 of 1983 concerning income tax. Article 2 of UU

No. 36 of 2008 states that the subject of taxation is (a

(1)) a person; (2) inheritance which has not been

divided as a unit replaces the entitled; (b) institution,

and; (c) permanent establishment. Article 2 paragraph

5 explains a permanent establishment is a form of

business that is used by individuals who do not reside

in Indonesia, individuals who are in Indonesia no

more than 183 (one hundred eighty-three) days within

12 (twelve) months, and an institution or agency that

is not established and is not domiciled in Indonesia to

run a business or conduct activities in Indonesia,

which may be in the form of (a) a place of

management; (b) company branches; (c)

representative office; (c) office building; (d) factory;

(e) workshop; (f) warehouse; (g) space for promotion

and sale; etc

2

2.3 Capital Structure

Modigliani & Miller (1958) was the first researcher

to develop the theory of capital structure. They

developed two propositions, namely the first claim

that the level of corporate leverage does not affect

2

Can be accessed at https://www.pajak.go.id/id/undang-

undang-nomor-36-tahun-2008

market value. The second explains that the weighted

average cost of a company as not affected by

corporate leverage (Acaravci, 2015).

2.4 Agency Theory

Agency theory is a theory that explains that in a

company two parties interact with each other. An

agency relationship is defined as a contract in which

one or several shareholders and company

management carry out certain activities that involve

the delegation of decision making authority to the

company's management. Companies that separate

management and ownership functions will be

vulnerable to agency conflict because each party has

conflicting interests, which is trying to achieve their

own (Jensen & Meckling, 1976).

2.5 Positive Accounting Theory

This theory was first coined by Watts & Zimmerman

(1986) at the William E. Simon School of Business

Administration at the University of Rochester. One of

these theories explains the political cost theory which

assumes that companies tend to show lower profits

using accounting methods and procedures so that

companies do not attract the attention of those who

oversee high-profit industries. Large companies

effectively utilize economic and political power to

reduce tax liability and are involved in tax planning

due to extensive resources (Ogundajo & Onakoya,

2016).

2.6 Tax Planning

Crumbley, Friedman, & Anders (1994) say that tax

planning is a systematic analysis aimed at minimizing

tax liabilities in the current and future periods

(Suandy, 2011). Tax planning is the first step in tax

management to minimize the company's tax burden.

Suandy (2011) divides tax planning into two, namely,

national tax planning which is carried out based on

domestic law and international tax planning which is

carried out based on domestic law and takes into

account international tax treaties and the laws of the

countries involved.

The Effect of Tax Planning on Financial Performance of Manufacturing Companies in Indonesia

187

2.7 Financial Performance

Financial performance is the company's ability to

manage and control company resources. Financial

performance is measured using the financial ratio

method (Ikatan Akuntan Indonesia, 2015).

Financial Ratio Analysis can be divided into (1)

profitability ratio analysis, used to measure a

company's ability to generate profits. For example,

ROA (Return on Asset) and ROE (Return on Equity);

(2) solvency ratio analysis, measuring the company's

ability to meet long-term obligations, payment of the

final principal of debt and other fixed obligations, for

example, debt ratio; (3) analysis of liquidity ratios, to

measure a company's ability to meet short-term debt

obligations, for example, cash ratio; (4) and activity

ratio analysis, used to measure how effectively a

company utilizes assets to generate revenue, for

example, fixed asset turnover ratios (Agnatia &

Amalia, 2018).

3 RESEARCH METHODOLOGY

This research uses descriptive quantitative because

the data used are secondary data taken from the

financial statements of manufacturing companies on

the official website of the Indonesia Stock Exchange

for the period 2014-2018. Sampling is done by a

purposive sampling method and processed using

Eviews 10.0 application. Data were then analyzed by

panel data regression using Generalized Least Square.

4 ANALYSIS AND DISCUSSION

4.1 Data Analysis

Data analysis was performed on all manufacturing

companies listed on www.idx.co.id for the 2014-2018

period. The number of companies listed as the study

population still has to go through the elimination

stage through established sampling criteria. The

results of the withdrawal criteria can be seen as

follows:

Table 1: Research Sample

Company Indication Total

Manufacturing companies listed on the

Indonesia Stock Exchange in 2014-2018,

experienced Initial Public Offering (IPO),

delisted, and moved to the non-

manufacturing sector during the research

period.

149

Companies that do not use Rupiah units. -13

Companies that do not have an Effective

Tax Rate (ETR) and Cash Effective Tax

Rate (CETR) value

-78

Data on all company components needed

in the study are incomplete

-9

Companies engaged in the property and

mining sector.

0

Selected companies become samples per

year

49

Total samples for the 2014-2018 period 245

Source: Data processed by the researcher, 2020

The first analysis conducted in this study was a

descriptive statistical analysis. Descriptive statistics

are statistical methods that describe the nature of the

results of research data in answering the problem

formulation and overall that is presented in tabular

form. Descriptive statistics are performed to

determine the min, max, mean, and standard

deviation of the dependent variable (financial

performance), independent variables (tax planning),

and control variables (leverage, size, age, and firm

growth). The results of the descriptive statistical

analysis test are in the following table:

Table 2: Analysis Descriptive Statistic Result

Variable Mean Maximum Minimum

Std.

Dev.

ROA 0.088 0.467 0.000 0.079

Tax

Payment*

0,149 4,426 0,000 0,440

Current Tax

Expense*

0,481 7,623 0,000 1,088

Leverage 0.378 0.839 0.056 0.179

Firm Size 28.723 33.474 25.619 1.729

Firm Age 39.490 87 5

16.60

7

Firm

Growth*

4,190 57,733 0,028 9,120

Sampel (N) 245 245 245 245

Note: This table presents the statistical test results. Independent

Variables: Current Tax Expense and Tax Payment. Control Variables:

Size, Leverage, Age, Firm growth. Dependent Variable: ROA (Return

on Asset). * = in trillion rupiah

Source: Data processed with Eviews 10, 2020

ICAESS 2020 - The International Conference on Applied Economics and Social Science

188

Several testing stages need to be performed before

conducting the panel data regression analysis, in

determining the appropriate panel data estimation

model. The testing phase carried out in this study

refers to Basuki & Prawoto (2016), to choose the

most appropriate model among common effects,

fixed effects, and random effects in managing panel

data, it is necessary to carry out several tests including

the chow test and the haussman test:

Table 3: Chow Test Results

Effects Test Statistic d.f. Prob.

Cross-section

F

13,207 -48,190 0,000

Source: Data processed with Eviews 10, 2020

Table 3 shows the value of the probability of

cross-section F that is equal to 0,000. The probability

value is smaller than alpha 5% (0,000 <0.05) and

shows that the best estimation model is the fixed

effect. The panel data test is then continued with the

haussman test to find out the best panel data method

between the fixed effect model and the random effect

mode

l.

Table 4 : Chi-Square Test Results

Test

Summar

y

Chi-Sq.

Statistic

Chi-

S

q

. d.f.

Prob.

Cross-section

rando

m

44,877 6 4,950

Source: Data processed with Eviews 10, 2020

Table 4 shows that the chi-square cross-section

probability value needed in selecting the panel data

estimation model is 4.9. The probability value is

greater than the significance level of alpha 5% (4.9>

0.05). Haussman test results are in accordance with

predetermined criteria if the chi-square probability

value> 0.05, then the random effect is the most

appropriate model.

The random effect method estimates panel data

where interruption variables may be interconnected

between time and between individuals. When using

the random effect model, the benefit is eliminating

heteroscedasticity. This model is also called the Error

Component Model (ECM) or the Generalized Least

Square (GLS) technique (Basuki & Prawoto, 2016).

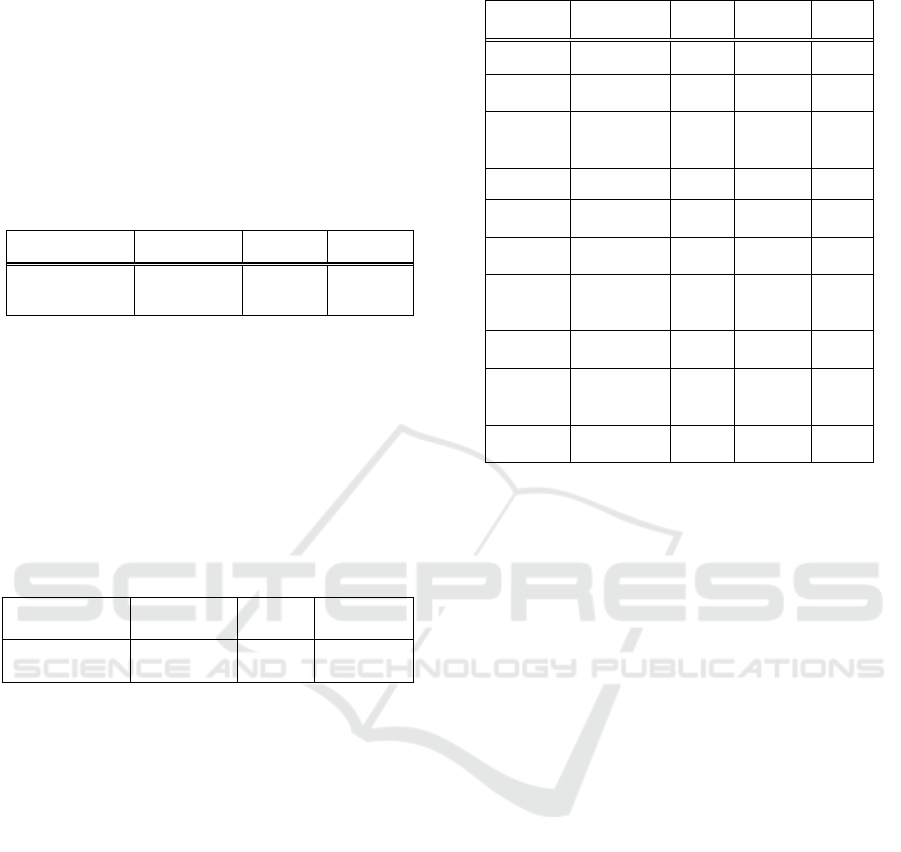

Table 5: Random Effect Test Result

Variable Coefficient

Std.

Error

t-

Statistic

Prob.

Roa 0.154 0.127 1.212 0.227

Tax

Payment

-5.294 1.556 -3.402 0.001

Current

Tax

Expense

6.681 9.262 7.214 7.214

Leverage -0.047 0.021 -2.212 0.028

Firm

Size

-0.004 0.004 -0.883 0.378

Firm

Age

0.001 0.000 3.746 0.000

BV of

Total

Asse

t

-3.951 8.761 -4.510 1.020

R-

squared

0.244

Adjusted

R-

squared

0.225

Prob(F-

statistic)

1.504

Source: Data processed with Eviews 10, 2020

The results of the random effects panel data

regression model in table 5 show a constant value of

0.154, while the coefficient value of the tax payment

variable shows a value of -5.294, the current tax

expense variable shows a value of 6.681, the variable

leverage indicates a value of -0.047, firm size

indicates the value of -0.004, firm age variable shows

a value of 0.001 and a book value of total assets

variable shows a value of -3,951. Based on the

coefficients of these variables, the panel data equation

model is as follows:

𝑅𝑂𝐴 0,154 5,294𝑇𝑃

6,681𝐶𝑇𝐸

0,047𝐿𝐸𝑉

0,004𝑆𝐼𝑍𝐸

0,001𝐴𝐺𝐸

3,951𝐵𝑉

The equation above shows the effect between tax

payment and current tax expense as independent

variables and firm size, leverage, firm age, and the

book value of total assets as control variables on the

dependent variable (ROA). The description of the

equation is the average financial performance through

ROA of 0.154 will decrease by 5.294 if the tax

payment variable increases by 1 unit, increases by

6.681 if the current tax expense variable increases by

1 unit, decreases by 0.047 if the variable leverage

decreases by 1 unit, decreases by 0.004 if the variable

size decreases by 1 unit, increases by 0.001 if the age

variable increases by 1 unit, and decreases by 3.951

if the book value of total assets variable increases by

1 unit.

H₀: Tax planning affects the financial performance of

manufacturing companies in Indonesia.

The Effect of Tax Planning on Financial Performance of Manufacturing Companies in Indonesia

189

Table 6 shows the results of hypothesis testing

using the Generalized Least Square method

Table 6: Hypothesis Test Results

Variable Coefficient

Std.

Error

t-

Statistic

Prob.

Roa 0.001 0.000 3.309 0.001

Tax

Payment

-4.516 2.301 -1.963 0.051

Current

Tax

Expense

4.336 1.026 4.227 0.000

F-

Statistic

20.524

Prob (F-

Statistic)

5.841

Source: Data processed with Eviews 10, 2020

The probability value of the independent variable

on the dependent variable with the control variable to

reduce the error rate is 5.841. The test results in Table

4.6, show that it can be stated that hypothesis 0 is

accepted with the probability value > alpha

significance level (5.841> 0.05).

4.2 Discussion & Results

4.2.1 Effect of Tax Planning on Financial

Performance of Manufacturing

Companies in Indonesia

Based on the statistical values in Table 4.3, the

hypothesis testing results with a prob value of 5.841>

0.05, it can be stated that the variable influence of tax

(X1) affects the financial performance (Y) of

manufacturing companies in Indonesia.

This research is supported by research conducted

by Ogundajo & Onakoya (2016). The results of this

study indicate that with increasing ETR there is a

reduction in ROA of 6.9%. This result is not

following the research of Kurawa & Saidu (2018)

who found an insignificant impact of corporate tax on

financial performance.

This is reinforced by Positive accounting theory,

where political costs specifically describe the

relationship of political costs or tax burdens faced by

a company. When the tax burden faced by companies

shows large numbers, then companies tend to use

accounting methods that can minimize the political

costs incurred. This illustrates the ability of a

company's performance as measured through the

financial solvency ratio, namely by measuring the

company's ability to meet long-term obligations, the

final principal payment of debt and other fixed

obligations.

5 CONCLUSIONS

This study used a descriptive quantitative method

approach with a total sample size of 245 samples

which were then analyzed by regression panel data

using ordinary least square. This study was conducted

with the aim of examining the effect of tax planning

on the financial performance of manufacturing

companies in Indonesia. The results of the research

conducted indicate the influence of tax planning on

the financial performance of manufacturing

companies in Indonesia which are listed on the IDX

for the 2014-2018 period.

This is reinforced by positive accounting theory,

namely political costs that specifically describe the

relationship between political costs or tax burdens

faced by a company. When the tax burden faced by

the company shows a large number, the company

tends to use an accounting method that is able to

minimize the political costs incurred. This illustrates

the ability of company performance as measured by

financial solvency ratios, namely by measuring the

company's ability to meet long-term obligations, final

principal payments on debt and other fixed liabilities.

Research sample data that focuses on the

manufacturing sector listed on the Indonesia Stock

Exchange so that it does not represent all companies

in other listed sectors, limitations on the dependent

variable studied, namely ROA, along with limitations

of the analysis tools used in this research are the

Eviews program version 10. Furthermore, future

research should add other additional variables that

can affect the dependent variable, use or add other

analysis tools to find out whether there are differences

in the research results, expand the sector of

companies listed on the Indonesia Stock Exchange as

the research population, and add other criteria in

selecting research samples.

REFERENCES

Acaravci, S. K. (2015). The Determinants of Capital

Structure: Evidence from the Turkish Manufacturing

Sector. International Journal of Economics and

Financial Issues, Vol. 5, No. 1, 158-171.

Agnatia, V., & Amalia, D. (2018). Pengaruh Economic

Value Added (EVA) dan Rasio Profitabilitas Terhadap

Harga Saham. Journal of Applied Managerial

Accounting, Vol. 2, No. 2, 290-303.

ICAESS 2020 - The International Conference on Applied Economics and Social Science

190

Basuki, A., & Prawoto, N. (2016). Analisis Regresi Dalam

Penelitian Ekonomi & Bisnis. Jakarta: Rajawali Pers.

Crumbley, D. L., Friedman, J. P., & Anders, S. B. (1994).

Dictionary of Tax Terms, Barron's Bussiness Guides.

New York.

Feng, H., Habib, A., & Tian, G. L. (2019). Aggressive Tax

Planning and Stock Price Synchronicity: Evidence from

China. International Journal of Managerial Finance,

829-857.

Ikatan Akuntan Indonesia. (2015). Pernyataan Standar

Akuntansi Keuangan. Jakarta: Salemba Empat.

Jensen, M., & Meckling, W. (1976). Theory of The Firm:

Managerial Behavior, Agency Costs, and Ownership

Structure. Journal of Financial Economics 3, 305-360.

Kristianto, Z., Andini, R., & Santoso, E. B. (2018).

Pengaruh Perencanaan Pajak Dan Tax Avoidance

Terhadap Nilai Perusahaan Dengan Kinerja Keuangan

Sebagai Variabel Intervening. Journal of Accounting,

Vol 4, No. 4.

Modigliani, F., & Miller, M. (1958). The Cost of Capital,

Corporate Finance, and The Theory of Investment.

American Economic Review, 261-297.

Munawir, S. ( 2004). Analisis Laporan Keuangan.

Yogyakarta: Penerbit Liberty.

Ogundajo, G., & Onakoya, A. (2016). Tax Planning and

Financial Performance of Nigerian Manufacturing

Companies. International Journal of Advanced

Academic Research, Vol 2, Issue 7, 64-80.

Suandy, E. (2011). Perencanaan Pajak. Jakarta Selatan,

DKI Jakarta, Indonesia: Salemba Empat.

Yuliem, M. L. (2018). Terhadap Nilai Perusahaan ( Firm

Value ) pada Perusahaan Sektor Non Keuangan yang

Terdaftar di Bei Periode 2013-2015. Jurnal Ilmiah

Mahasiswa Universitas Surabaya, Vol 7, No 1, 520-

540.

The Effect of Tax Planning on Financial Performance of Manufacturing Companies in Indonesia

191