Purchase Intention of E-Payment: The Substitute or Complementary

Role of Brand, Sales Promotions, and Information Quality

Mutiara Lingga Ramadanty and Dwi Kartikasari

1

Department of Business Administration, Politeknik Negeri Batam, Ahmad Yani Street, Batam, Indonesia

Keywords: e-payment, e-wallet, Purchase Intention, Brand Equity, Sales Promotion, Information Quality

Abstract: e-payment is becoming more relevant in the era of the revolution industry 4.0 despite the corona health

crisis. This study aims to determine the impact of brand equity, information quality, sales promotions, and

the interaction effect between the three aforementioned antecedents to purchase intention of e-payment. The

research used structural equation modeling, hierarchical moderated regression, and simple slope analysis to

a sample of 241 respondents selected using proportionate sampling. Constructs were adapted from past

studies, but only constructs passed the validity, reliability, and model fitness were subsequently used. This

research affirms previous studies proving that information quality, brand equity, and sales promotions are

positively associated with purchase intention. This study contributes to the literature when it finds the

simultaneous significant positive effect of these three factors to purchase intention given the fact that past

studies only tested separate effects. The study also confirms preceding discoveries that acquire a stronger

effect once the interaction effect of overall determinants is considered. Yet, the interaction effect separately

tends to substitute rather than a complementary role, although not significant. Therefore, theoretically, this

study does not corroborate the new concepts of the isolated interaction effects. This study suggests new

predictors and the various context in subsequent studies for the benefits of theories and practices.

1 INTRODUCTION

Like in other countries across the world, the

financial technology abbreviated fintech, is

expanding rapidly in Indonesia (Davis et al., 2017).

Fintech utilizes innovation in financial services.

Fintech very first model was Zopa which was

introduced in 2004 in the UK (Ferdiana & Darma,

2019). In Indonesia, the growth of fintech is

extraordinary – fifty fintech companies in 2016

tripled to 167 ventures in just two years and

transaction value grows 16,3 percent annually

(Fintech Singapore, 2018). The growth of Fintech

was high before the COVID-19 outbreak, further, it

benefits expansion greater than ever due to the

massive use of e-commerce after the social

restriction following the plague. Henceforth, fintech

is becoming more relevant in the era of revolution

industry 4.0 despite the corona health crisis.

There is no standard classification of fintech. In

Indonesia, resembling in the U.S., e-payment, and e-

lending dominate the market with mobile payment

as the market leader as shown in Figure 1.

concerning who is in charge of fintech, payment

activities are regulated by the Central Bank of

Indonesia while lending ones, as well as

crowdfunding are by the Indonesian Financial

Services Authority (OJK).

Figure 1: Distribution of the Indonesian Fintech.

(Franedya & Bosnia, 2018)

As the blockbuster in the fintech ecosystem, e-

wallet offers settlement and clearing payment

services in cashless, quick, secured, and accurate

manners for all types of transactions. Various e-

payment providers compete for the position of a

298

Ramadanty, M. and Kartikasari, D.

Purchase Intention of e-Payment: The Substitute or Complementary Role of Brand, Sales Promotions, and Information Quality.

DOI: 10.5220/0010355402980308

In Proceedings of the 2nd International Conference on Applied Economics and Social Science (ICAESS 2020) - Shaping a Better Future Through Sustainable Technology, pages 298-308

ISBN: 978-989-758-517-3

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

bestseller. This position seems to be won by PT.

Dompet Anak Bangsa issued Gopay as indicated by

Figure 2. Gopay has been maintaining its place

consistently since 2017 based on the number of

monthly active users at Google Play and iOS.

Figure 2: The top three e-wallet providers in Indonesia.

(Devita, 2019)

Gopay has become the most popular online

payment application in the Indonesian community,

especially among millennials. It contributes to 30

percent of total electronic transactions nation-wide

(Devita, 2019). Gopay is used to pay diverse

transactions to a wide range of partners such as

McDonald's and enormous micro, small and

medium enterprises, as well as pay electricity bill

and buy vouchers. It targets generation Y like

university students who are attached very heavily

with mobile phones and the internet in their daily

activities. Considering its dominant impact in the

e-payment sector in Indonesia, the authors choose

Gopay as the scope of this study where the type of

extended offers is specified accordingly. Students

are also chosen as the samples because they tend

connection to Gojek.

Many factors lead to consumer interest in

using or buying technology-products online. From

the buyer’s perspective, there are internal factors

such as the perceived ease, perceived benefits, and

perceived ease of use for technology-related

products according to the technology acceptance

model (Hasim et al., 2019). Whereas from the

product’s perspective, there are external factors,

namely brand, information richness, and extended

offers (Yen, 2014).

Most literature builds upon internal factors as

the antecedents of online purchase intention while

external factors are less discussed (Putri & Noer,

2017). Thus, this work seeks to shed more light on

the role of brand, extended offers, and information

richness on online purchase intention. This work

pursues to fill in the research gap in the adoption of

e-payment. Besides, this study has a vital role to

improve the adoption of a cashless society in

Indonesia. Its implications are beneficial for both

regulators and application providers as they seek to

supervise and manage the expanding e-commerce

environment.

2 LITERATURE REVIEW

2.1 Determinants of Purchase Intention

Consumer purchase intentions reveal an interest that

triggers and encourages consumers to buy a

particular product (Agusli & Kunto, 2013). It

comprises a process shrouded in the consumer mind

when looking at a product until she decides to buy

the product at once or at a later time (Tariq, Nawaz,

Nawaz, & Butt, 2013).

Customer purchase intention is not a new

concept in sales and marketing literature. It

represents consumer behavior that invites sales

volume (Santini et al., 2016). Sales are always the

bottom line of any business. However, when

purchase intention’s literature is confined in the e-

commerce context and digital environment,

especially e-payment in Indonesia, the studies

dismount in this scope. Further, when purchase

intention is limited under quantitative studies, the

works are scant in this regard. The authors

summarize the related studies as follows:

Purchase Intention of e-Payment: The Substitute or Complementary Role of Brand, Sales Promotions, and Information Quality

299

Table 1: Summary of literature findings on aspects

affecting electronic purchase intention.

Independent

va

r

ia

b

les

Context Studies Findings

Brand Merchant

characteristics

Two studies

(Akar &

Nasir, 2015)

Significant

positive impact

Brand quality

and brand

equity of

branded

we

b

site

Chang et al.

(2017)

Significant

positive impact

Retailer brand

in e-

commerce

Putri & Noer

(2017); Yen

(2014)

Significant

positive

impact, but

contradictory

in substitute

and

complement

effect

Information

quality

Merchant

characteristics

Two studies

(Akar &

Nasir, 2015)

Significant

positive impact

Information

richness in v-

commerce for

se

r

v

ices

Chesney et al.

(2017)

Significant

positive impact

Information

quality and

media

Richness

(information

supplied by

seller)

Chen & Chang

(2018)

Significant

positive

precursors

with

satisfaction as

an intervening

va

r

ia

b

le

Information

richness

Putri & Noer

(2017); Yen

(2014)

Significant

positive

impact, but

ambiguous in

substitute and

complement

effect

Sales

promotions

Relative

advantages

Twelve

studies (Akar

& Nasir,

2015)

Significant

positive impact

Sales

promotions

Santini et al.

(2016)

Significant

positive impac

t

Extended

offers

Putri & Noer

(2017); Yen

(2014)

Significant

positive

impact, but

inconsistent in

substitute and

complement

effect

2.2 Information Quality Impact on

Purchase Intention

Information quality reflects the amount of

information conveyed by the seller via the media of

communication to consumers. The detailed and

complete facts greatly facilitate consumers to get a

description and specification of the products to be

purchased. The availability and completeness of info

help improving consumer buying interest.

The theory of information richness postulates

that electronic media like e-payment can promote e-

commerce, but to a lesser extent than information

richer face-to-face interactions in proportion to its

capacity to carry information (Chesney et al., 2017).

The richer the information, the higher the level of

trust, as a result, the greater intention of customers

to buy electronic products or services. When taking

satisfaction into account, the higher the quality of

information supplied by the seller, the more satisfied

the customer, henceforth, the bigger her interest to

procure (Chen & Chang, 2018). Eventually, this

work brings forth the following hypothesis:

H1: Information quality positively impact the

purchase intention of e-payment

2.3 Brand Equity Impact on Purchase

Intention

A brand is the reputation of the seller that can affect

consumer interest in using its products or services.

Every product sold in the market has a reputation in

the eyes of every consumer. A brand is something

that has been deliberately created by the suppliers to

differentiate their products with the products of their

competitors (Arifin & Fachrodji, 2015)

The theory of planned behavior (TPB) as well as the

theory of reasoned actions (TRA) claims that one’s

perceptions affect her intentions and behaviors

(Mady, 2017). This theory is adopted to explain the

link between consumers’ purchase intention and

specific brand or products (Chin et al., 2019). The

perceived brand equity and brand quality lead to

trust that entices purchase intention. In other words,

A brand is stimulus, while purchase intention is the

response to the a stimulus (Chang et al., 2017).

Thus, this study defines the following hypothesis:

H2: Brand equity positively impact the purchase

intention of e-payment

2.4 Sales Promotions Impact on

Purchase Intention

Sales promotions include additional services from

sellers such as discounts, cashback, online services,

express delivery, and other things that can increase

the interest of consumers to use products or services

from these providers. Extra promotional actions

such as discounted sale are a service that is often

ICAESS 2020 - The International Conference on Applied Economics and Social Science

300

used by a company to attract customers to continue

to buy or use its products.

The theory of Maslow’s hierarchy of needs is

highly linked with marketing activities (Hasim et al.,

2019), including sales promotions. Promotional

events are aimed to motivate a person to decide

between buying products by appealing to her needs

such as basic needs, security, love, self-esteem, and

self-actualization. Researchers declare that sales

promotions are vital for marketing strategy because

they invite customers to a transaction, thus

mitigating the psychological costs related to

purchasing (Santini et al., 2016). Therefore, this

work offers the following hypothesis:

H3: Sales promotions positively impact the purchase

intention of e-payment

2.5 The Interaction Impact of the

Brand, Information Quality, and

Sales Promotions on Purchase

Intention: Substitute or

Complement

Substitute and complementary roles are frequently

discussed in e-commerce settings. Substitute

products are interchangeable while complimentary

ones are those that might be purchased together by

users (Wang, Jiang, Ren, Tang, & Yin, 2018). Many

products in the current digital world are claimed as

substitute but research proves otherwise. For

instance, Facebook is accused to deteriorate

relationship and decrease intimacy among its users

because it substitutes for face-to-face interaction.

This claim is rejected when research finds that

Facebook acts as an extension or complementary of

face-to-face interaction (Kujath, 2011). Another

example is Uber. Its effect on public transit is

ambiguous. Uber is an alternative mode of travel,

thus one might claim it is a substitute service.

However, it can also increase the reach and

flexibility of public transit. Research shows that

Uber is not a substitute, but rather, a complement

for the average transit agency because it increases

public transit use for the average transit agency in

U.S metropolitan areas (Hall, Palsson, & Price,

2018).

Previous research has shown unclear findings of

the interaction effect between information quality,

brand, and sales promotions. Table 2 recapitulates

the results.

Table 2: Summary of literature findings on the interaction

effect of a brand, information quality, and sales

promotions on purchase intention.

Va

r

ia

b

les Interaction Stu

d

ies Fin

d

in

g

s

Information

quality and

brand equity

Complement Yen (2014) Statistically

significant

Substitute Putri &

Noer

(2017)

Not

significant

Information

quality and

sales

promotions

Complement Yen (2014) Statistically

significant

Complement Putri &

Noer

(2017)

Not

significant

Brand

equity and

sales

promotions

Substitute Yen (2014) Statistically

significant

Substitute Putri &

Noer

(2017)

Not

significant

Table 2 indicates the contradictory results of two

previous studies. This work attempts to resolve this

issue by adding more findings to support or reject

either one. Because Yen (2014) has more significant

findings, the authors propose the following

hypotheses:

H4: Information quality moderates the brand equity

in complementary impact on the increase of

purchase intention of e-payment in such a way that

e-payment provider with high information quality

will expand the effect on purchase intentions when

brand equity is well- known.

H5: Information quality moderates the sales

promotions in complementary impact on the

increase of purchase intention of e-payment in such

a way that e-payment providers with high

information quality will magnify the effect on

purchase intentions when sales promotions are high-

pitched.

H6: Brand equity moderates the sales promotions in

substitute impact on the increase of purchase

intention of e-payment in such a way that e-

payment providers with a renowned brand will

inflate the effect on purchase intentions even when

sales promotions are low.

H7: Information quality, brand equity, and sales

promotions altogether positively impact the

purchase intention of e-payment H4, H5, and H6

are hypotheses induced from the tendencies of

previous studies. While H7 is a new hypothesis to

integrate all variables simultaneously.

Purchase Intention of e-Payment: The Substitute or Complementary Role of Brand, Sales Promotions, and Information Quality

301

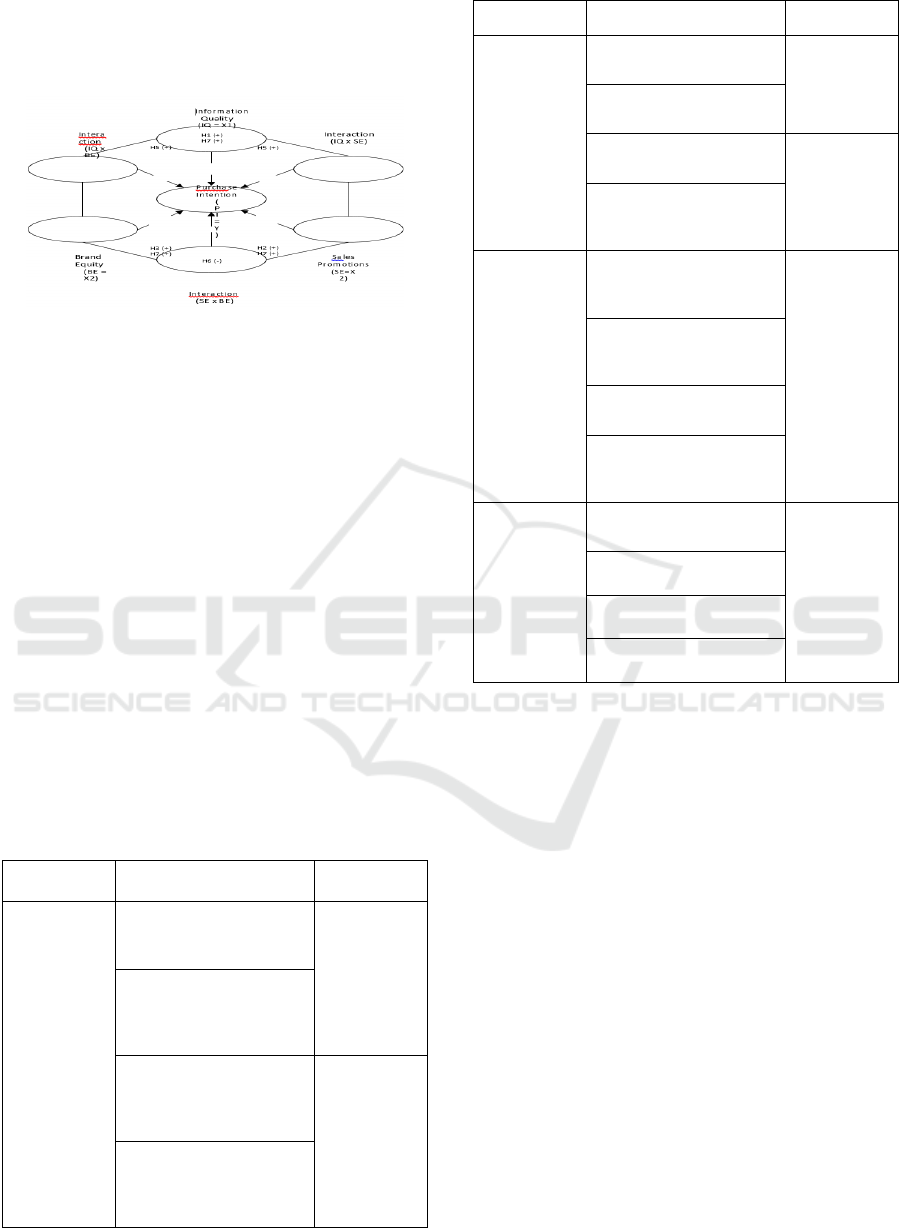

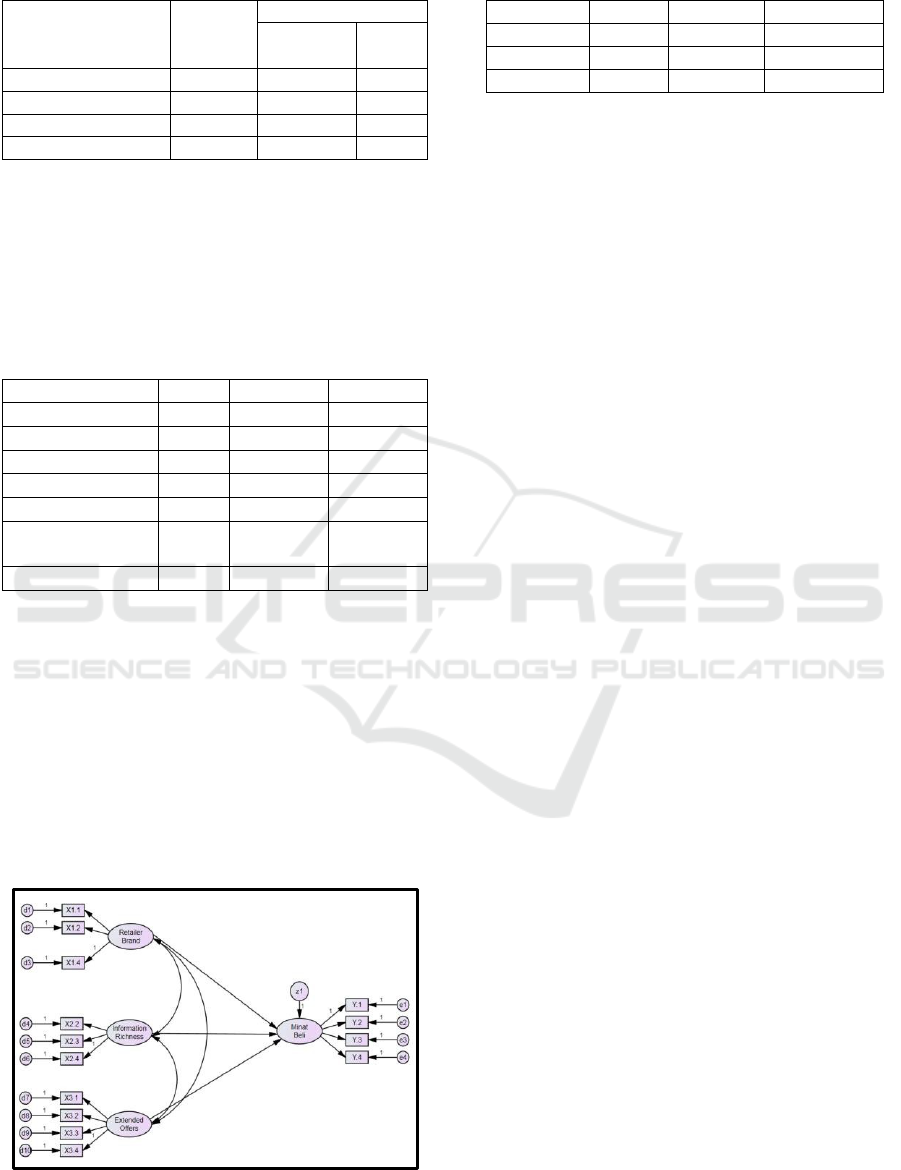

2.6 Research Model

The seven afore-mentioned hypotheses are

depicted in the research model below.

Figure 3: Research model of the role of brand, information

quality, and sales promotions on purchase intentions of e-

payment

H1, H2, and H3 were tested using Structural

Equation Model (SEM) analysis with AMOS as the

statistical tool. H4, H5, H6, and H7 were analyzed

using hierarchical moderated multiple regression

and simple slope with SPSS software.

3 RESEARCH METHOD

3.1 Research Design

This study uses quantitative research methods. The

authors adopt the instrument of past research as

follows. The study did not run a pilot test for the

questionnaire because it used parameters that were

used by other researchers.

Table 3: The operationalization of constructs (The

instrument of this study)

Construct Item Source

Information

quality

(IQ = X1)

IQ1. The e-payment

provider enables me to

obtain rich information

Yen (2014)

IQ2. The e-payment

provider supplies diverse

types of information from

electronic mass media

IQ3. The e-payment

provider equips me to get

relevant information about

its services

Putri & Noer

(2017)

IQ4. The e-payment

provider equips me to get

consistent information about

its services

Construct Item Source

Brand equity

(BE = X2)

BE1. E-payment provider is

well-known brand

Putri & Noer

(2017)

BE2. E-payment provider

has a good reputation

BE3. I recognize the e-

payment logo

Yen

(2014)

BE4. I have better opinions

about the e-payment

provide

r

Sales

promotions (SP

= X3)

SP1. The e-payment

provider offers like cashback

and promotions

Putri

& Noer (2017)

SP2. The e-payment

provider extend the offers

with its merchants

SP3. The payment and refill

processes are convenien

t

SP4. The e-payment

provider supports peripheral

services

Purchase

intention (PI =

Y)

PI1. I would like to buy

products using e-paymen

t

Putri

& Noer (2017)

PI2. I will use e-payment in

the future

PI3. I intend to buy a

product using e-paymen

t

PI4. I will buy a product

using e-paymen

t

Data were collected by questionnaire with 5-scale

Likert using Google form from January to March

2020. The respondents agreed by checking the

consent statement instead of signing it in person.

3.2 Sampling

As Structural Equation Modeling (SEM) is used in

this study, the author’s determined sample size as 15

times the number of indicators (Hair & Anderson,

1998) in (Riduwan & Akdon, 2006). This research

has 16 items as described in Table 3. Accordingly,

the required minimum sample is 16 x 15 = 240

respondents. The sampling technique used in this

research was accidental proportionate sampling as

samples taken from heterogeneous student

populations (Riduwan & Akdon, 2006). Students

were picked for their savviness on the internet and e-

commerce. Furthermore, the number of students

targeted was calculated in proportion of 16 study

programs by the following formula:

ICAESS 2020 - The International Conference on Applied Economics and Social Science

302

𝑛𝑖

𝑁𝑖

𝑁

. 𝑛

Where:

ni: the number of samples proportionately

n: the number of the total targeted samples

Ni: total population proportionately by the study

program

N: the total population of internet-savvy students

The research managed to collect response per study

program as follows:

Table 4: Samples

N

o Stud

y

p

ro

g

ram Sam

p

le

1 Business administration 27

2 Mana

g

erial accountin

g

22

3 Accountin

g

21

4 Electrical engineering 15

5 Electro manufacture en

g

ineerin

g

9

6 Mechatronics 18

7 Robotics 7

8 Instrumentation 7

9 Power

p

lant 4

10 Informatics 27

11 Multimedia and networkin

g

29

12 Geomatika 12

13 Animation 6

14 Mechanical en

g

ineerin

g

20

15 Shi

p

b

uildin

g

en

g

ineerin

g

9

16 Aircraft maintenance 8

Total 241

Samples aged from 18 to 23 years old. The majority is

20 and 21 years old.

Table 5: Validity and normality results

Indica

tor

Validity Normality

α

(≥r

table

)

St. Loading

(≥0.6)

Skew

(±2.58)

Kurtosis

(±2.58)

IQ1* 0.585 0.310

IQ2 0.834 0.845 -5.792 1.135

IQ3 0.767 0.804 -6.740 3.489

IQ4* 0.712 0.540

BE1 0.846 0.850 -7.879 5.154

BE2 0.861 0.909 -8.004 5.122

BE3* 0.536 0.260

BE4 0.875 0.913 -7.031 2.978

SP1 0.782 0.799 -6.248 1.813

SP2 0.747 0.770 -5.823 1.513

SP3 0.769 0.830 -6.037 1.542

SP4* 0.705 0.520

PI1 0.877 0.873 -6.476 1.874

PI2 0.842 0.877 -7.012 2.619

PI3 0.876 0.887 -7.425 3.052

PI4 0.884 0.859 -6.416 2.215

4 RESULTS AND DISCUSSIONS

4.1 Validity, Reliability, and Normality

This study used regression analysis utilizing SPSS as

well as SEM utilizing AMOS. The validity of

Cronbach’s alpha (α) resulting from SPSS shows

that all Cronbach’s alphas are well above its cut-off

value of 0.1264 drawn from r- table (See Table 5).

Thus, all parameters are valid according to

Cronbach’s alpha. However, when the validity is

looked closely with regards to standard loading (st.

loading) or factor loading or lambda , Table 5

shows that some items are below the threshold value

of 0.6 (Putri & Noer, 2017), hence some indicators

are eliminated (marked with an asterisk). After the

elimination of indicators, the authors rerun the

AMOS resulting in the standard loading values in

the table below. Further analysis is based on the

selected parameters only, those that fulfill the cut-

off criteria.

* eliminated indicators SEM programs assume that

endogenous variables are normally distributed.

However, as can be seen in Table 5, none of the

critical ratios of skew falls between -2.58 to 2.58,

thus data are skewed. Some indicators, i.e. IQ2,

SP1, SP2, SP3, and PI fulfill the criteria because

their critical ratios of kurtosis are from -2.58 to

2.58, thus data are partially kurtotic. Table 7

demonstrates that multivariate value is within the

threshold standards. We conclude that the residuals

of this SEM analysis are not univariate normally

distribution but joint multivariate normal (JMVN)

thus the normal distribution assumption is not

completely met. The authors expect that the large

samples in this study make up this flaw and the

analysis can be carried out further.

This study used Cronbach’s alpha not only for

validity testing but also for the reliability or internal

consistency testing. Given the decisive factors as

displayed in Table 6, all reliability coefficients

satisfy the threshold requirements including

construct or composite reliability and the average

variance extracted (AVE) where convergent validity

is met. Therefore, this research has fulfilled all the

criteria of a construct’s validity and reliability.

Purchase Intention of e-Payment: The Substitute or Complementary Role of Brand, Sales Promotions, and Information Quality

303

Table 6: Construct’s validity and reliability results

Variable Validity

α

(≥0.7)

Reliability

Construct

(≥0.7)

AVE

(≥0.5)

Information Quality 0.784 0.810 0.680

Bran

d

Equit

y

0.700 0.920 0.794

Sales Promotions 0.732 0.842 0.640

Purchase Intention 0.893 0.928 0.764

4.2 Structural Equation Model Results

To validate the SEM model as a whole, the

authors evaluate goodness-of-fitness (GoF). The

research meets all requirements regarding the

model fit.

Table 7: Goodness-of-fitness of the model

Ite

m

ValueTh

r

eshol

d

Remar

k

Probability level

absolute fit

NFI 0.967 ≥0.8 Model fit

FCFI 0.993 ≥0.95, ≤1 Model fit

II 0.993 ≥0.8 Model fit

TLI 0.991 ≥0.95, ≤1 Model fit

CMIN/DF atau

relative X

2

1.235 ≤2 Model fit

RMSEA 0.041 ≤0.06 Model fit

Test statistics in Table 8 reveals the statistically

significant positive individual path coefficients.

Column estimates (est.) exhibits positive values

while column significance (Sig.) displays values

below the cut-off significance level of 0.05.

Therefore, H1, H2, and H3 are accepted, in other

words, information quality, brand equity, and sales

promotions partially influence consumer purchase

intention of e-payment in positive a fashion. The

higher the quality of information or the better known

the brand equity or the greater sales promotions, the

larger the intention of consumers to use e-payment.

Figure 4: The Framework results of H1, H2, H3 with SEM

model

Table 8: Results of hypotheses testing with SEM model

Va

r

ia

b

le Est. (+) Sig. Decision

PI <--- IQ 0.650 0.007** H1 accepted

PI <--- BE 0.367 0.037 H2 acce

p

te

d

PI <--- SP 0.358 0.007** H3 accepted

** Statistically significant at p≤0.01, R2 = 0.937

4.3 Hierarchical Moderated Multiple

Regression Results

To test the interaction between independent

variables and the dependent variable, this study

used hierarchical moderated multiple regression as

well as simple slope analysis utilizing SPSS. The

authors used the technique of least squares

hierarchically, i.e. step 1 is the main effects

(information quality, brand equity, and sales

promotions), followed by interaction in step 2. As

such, we adapted Yen Where Y is purchase

intention, X1 is information quality, X2 is brand

equity, X3 is sales promotions, α is intercepted, is

slope coefficient, and is an error. Table 9 displays

that model 2 with the interaction between

information quality, brand equity, and sales

promotions accounted for significantly more

variance than by themselves without interaction on

consumer’s purchase intention of e-payment. R-

square significantly improved from model 1 to

model 2.

ICAESS 2020 - The International Conference on Applied Economics and Social Science

304

Table 9: Results of hypotheses testing with hierarchical

moderated multiple regression model

Predicto

r

Coeff. Sig. Remarks

Model

Step 1

IQ 0.084 0.368

BE 0.522* 0.000

SP 0.388* 0.000

R

2

0.832

F 228* 0.000 Model 1

significant, H7

acce

p

te

d

Model

Ste

p

2

IQ 0.201 0.740

BE 0.772* 0.006

SP 0.959 0.139

IQ x BE 0.009 0.952 H4 rejecte

d

IQ x SP -0.051 0.461 H5 rejecte

d

BE x SP -0.111 0.422 H6 rejecte

d

R

2

0.846

R

2

F sig

0.013* 0.010 Model 2

significantly

accounts more

variance than

model 1

F 123* 0.000 Model 2a

significant

* Statistically significant at p≤0.05

Although model 2 improved R-square, its

interactions are not statistically significant as shown

by the significance level of IQ x BE, IQ x SP, and

BE x SP that exceed 0.05. Therefore, H4, H5, and

H6 are rejected. Whilst model 1 indicates

statistically significant F value so that H7 is

accepted.

4.4 Simple Slope Results

Simple slope analysis in this study is used to

support or reject the coefficients of H4, H5, and

H6. It was done by looking at the slope of two

lines drawn using the visualization data output

obtained from (2014) and used the subsequent

regression equation in two hierarchical steps:

Item Value Threshold Remark

Multivariate 0.862 Between

±2.58

Multivariate

normal

dist

r

i

b

u

tion

D

egrees of freedom 48 ≥0 The model is

structurally

identified,

model fit.

Chi-sq

u

are X

2 0.127 ≥0.05 Overall /

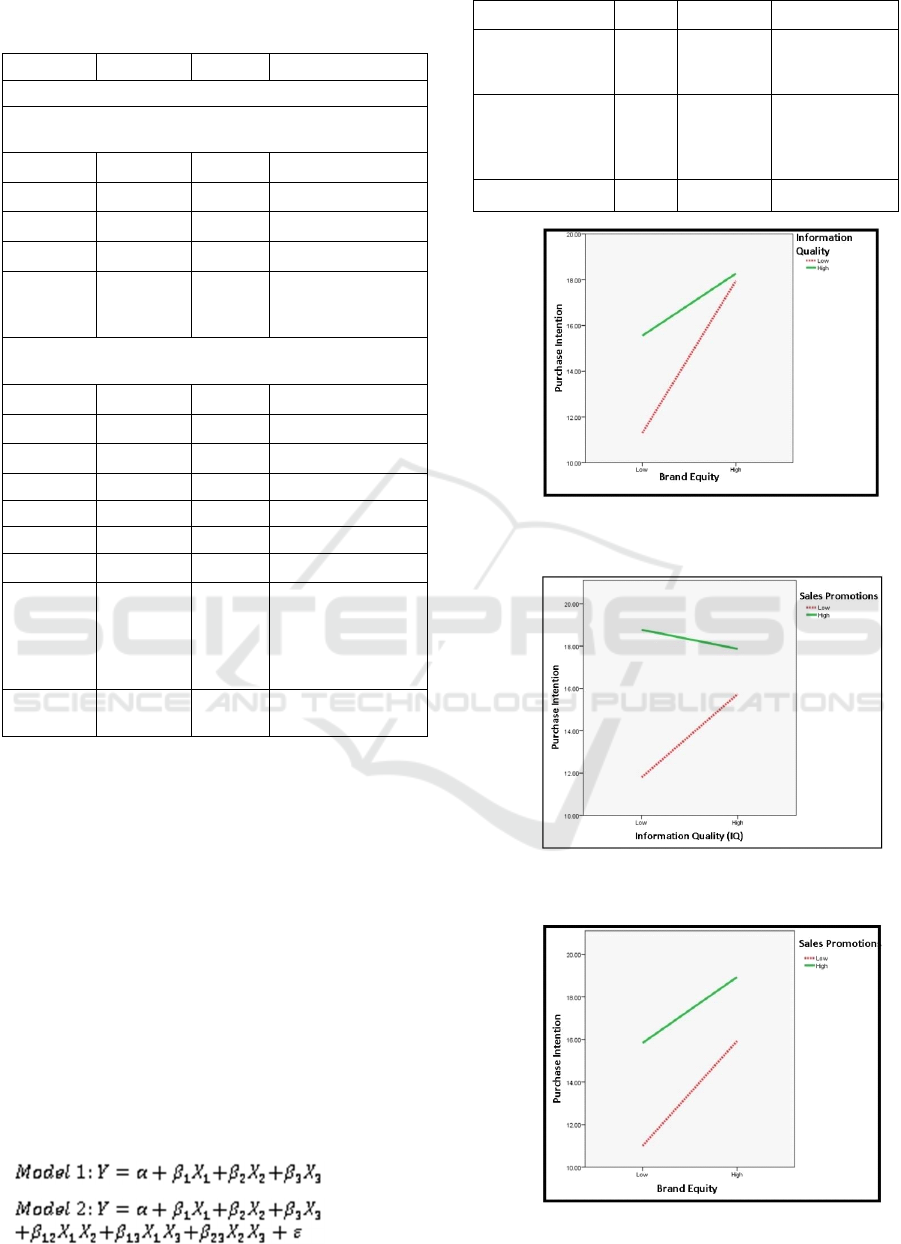

Figure 5: The substitute role of brand equity and

information quality to purchase intention of e-payment

Figure 6: The substitute role of sales promotions and

information quality to purchase intention of e-payment

Figure 7: The substitute role of brand equity and

information quality to purchase intention of e-payment

Purchase Intention of e-Payment: The Substitute or Complementary Role of Brand, Sales Promotions, and Information Quality

305

Figure 5, Figure 6, and Figure 7 demonstrate two

lines converging to a point suggesting that the

interaction between information quality, brand

equity, and sales promotions tend to be substitution

than complement which reject H4 and H5 yet

support H6 in terms of interactions. Although

hierarchical moderated multiple regression results

prove that these interactions are not statistically

significant.

4.5 Discussions

This research affirms previous studies (Yen, 2014;

Putri & Noer, 2017) proving that information

quality, brand equity, and sales promotions are

positively associated with consumer purchase

intention. This finding is consistent in this regard

supported by not only its SEM results but also

hierarchical regression results. However, this study

extends the context from the previous e-commerce

environment to the context of this study that is e-

payment. Furthermore, this study enriches literature

in a way that it finds the simultaneous significant

positive effect of these three factors (H7) to

purchase intention especially given the fact that the

two reference studies did not test this hypothesis and

only tested separate effects.

Provided the consistency of this finding with

previous researches, this study implies the managers

of e-payment providers must pay great attention to

information quality, brand equity, and sales

promotions to stimulate purchase intention and

further sales. It is obvious than consumers prefer

buying from suppliers that provide rich, updated,

relevant, and consistent information about the

products and services than those lacking

information. The consumers also tend to accept

services from well-known brands rather than

infamous ones, hence practitioners should build

their good reputation and respectable opinions as

well as keep introducing their existence via their

logos among potential users. Last, the customers

inclined to shop from sellers who offer extended

sales promotions including cashback, discounts,

enormous merchants, convenient refill, and

peripheral services that add values to the primary

services of e-payment to the shoppers.

Besides, given the outcome of this study, it is

advisable that the authority that supervises the e-

payment environment encourage the providers to put

their best efforts in the aspects of information

quality, brand equity, and sales promotions to attract

a new customer base and socialize a cashless

society. In the time of the covid-19 plague where a

cashless transaction is preferable than otherwise to

limit the spread of the virus attached in paper money

and coins, e-payment should be promoted its

advantages, offers, and prestige for more massive

utilization in the community iconsistent and clearly.

The study also confirms preceding discoveries

that R- squared improves substantially as the

interaction effect of information quality, brand

equity, and sales promotions as a whole to purchase

intention was taken into account when compared

with R-squared without the interaction effect. This

study acquires a stronger effect than earlier studies

as it exhibits a higher coefficient of determination

where the model of this study explains 84.6 percent

of the variability of data. The R-squared increases

by 1.3 percent once the interaction effect of overall

determinants is considered. This uniformity of this

finding suggests that future research should

incorporate the interaction effect of variables in the

research model to result in a sounder impact, thus

reinforce the existing theories.

This study notices that the interaction effect of

information quality and brand equity (IQ x BE),

information quality and sales promotions (IQ x SP),

brand equity, and sales promotions (BE x SP)

separately to purchase intention tend to substitute

rather than a complementary role, despite its

insignificancy. The immateriality of each interaction

effect is consistent with Putri & Noer (2017) but

opposing Yen (2014). Therefore, theoretically, this

study does not corroborate the new concepts of the

isolated interaction effects that the previous study

addressed.

Although the individual interaction effects are

not substantial, the substitute effect as shown by

simple slope graphs means that information quality

moderates the brand equity on the increase of

purchase intention of e-payment in such a way that

e-payment provider with high information quality

will expand the effect on purchase intentions when

brand equity is not prominent. Thus, information

quality substitutes brand equity on purchase

intention. Accordingly, e-wallet sellers should

provide rich information and sales promotions

especially when their brands are not well-known, in

other words, rich information and sales promotions

substitute the role of brands on purchase intention.

Likewise, e-payment providers with high

information quality and eminent brand will magnify

the effect on purchase intentions when sales

promotions are low-pitched. Consequently,

practitioners should always keep in touch with their

consumers even when they cannot offer them extra

ICAESS 2020 - The International Conference on Applied Economics and Social Science

306

promotions with consistent and rich information

about their brands.

The disparities of outcome with the past study

of Yen (2014) might be caused by differences in the

culture of respondents that result in distinct

behavior. Brands and promotions vary in different

countries and cities. For example, Gopay brand

exists in Indonesia, but not in Taiwan. Promotions of

merchants exist in Jakarta, but not in Batam. Hence

this study calls for researches in various cultures,

diverse settings, and assorted countries in the future.

Another reason that triggers dissimilar findings is

that this study uses Gopay as the context of

explaining promotions, brands, and information

quality to our samples when they stumbled on our

questionnaire. Although Gopay is the most widely

used e-payment that the majority of samples can

relate to, it might contribute to the biasness of the

study to the point where the findings are limited to

be generalized and applied to other sectors.

Some control variables might affect purchase

intention yet disbanded in this study. For instance,

Yen (2014) claimed that age contributes to purchase

intention significantly yet Putri & Noer (2017) did

not support this. Both agree that gender is not a

significant antecedent. Yen (2014) argues that

experience might be a better predictor than age and

suggests to contain this predictor isubsequent studies

for the benefits of theories and practices.

5 CONCLUSIONS

This research affirms previous studies proving that

information quality, brand equity, and sales

promotions are positively associated with consumer

purchase intention. However, this study extends

the context from the previous e-commerce

environment to e-payment. Furthermore, this study

enriches literature in a way that finds the

simultaneous significant positive effect of these

three factors to purchase intention given the fact that

past studies only tested separate effects. Provided

the consistency of this finding, managers of e-

payment providers must pay great attention to

information quality, brand equity, and sales

promotions to stimulate purchase intention and

further sales. It is obvious than consumers tend to

buy from suppliers that provide rich, updated,

relevant, and consistent information about the

products and services. The consumers also tend to

accept services from well-known brands, hence

practitioners should build their good reputation as

well as keep introducing their existence via their

logos among potential users. Last, the customers

inclined to shop from sellers who offer extended

sales promotions including cashback, discounts,

enormous merchants, convenient refill, and

peripheral services that add values to the primary

services of e- payment to the shoppers. Also, it is

advisable that the authority that supervises the e-

payment environment to encourage the providers

to put their best efforts in the three aspects as to

attract a new customer base and socialize cashless

society, more importantly in the time of covid-19

plague where a cashless transaction is preferable.

The study also confirms preceding discoveries

that acquires a stronger effect once the interaction

effect of overall determinants is considered. Yet, the

interaction effect separately to purchase intention

tends to substitute rather than a complementary role,

despite its insignificancy. Therefore, theoretically,

this study does not corroborate the new concepts of

the isolated interaction effects that the previous

study addressed. The disparities of outcome might

be caused by differences in the culture of

respondents that result in distinct behavior. Another

reason that triggers dissimilar findings is that this

study uses Gopay as the context of explaining

promotions, brands, and information quality to

samples when they stumbled on the questionnaire.

This study suggests adding experience as a predictor

and various context in subsequent studies for the

benefits of theories and practices.

REFERENCES

Agusli, D., & Kunto, Y. (2013). Analisa Pengaruh

Dimensi Ekuitas Merek Terhadap Minat Beli

Konsumen Midtown Hotel Surabaya. Jurnal

Manajemen Pemasaran Petra, 1 No.2, 2-3.

https://doi.org/ttp://dx.doi.org/10.1362/147539215X14

441363630837

Arifin, E., & Fachrodji, A. (2015). Pengaruh Persepsi

Kualitas Produk, Citra Merek dan Promosi Terhadap

Minat Beli Konsumen Ban Achilles di Jakarta Selatan.

Jurnal Ilmiah Manajemen, 127128.

Akar, E., & Nasir, V. A. (2015). A review of literature on

consumers’ online purchase intentions. Journal of

Customer Behaviour, 14(3), 215–233.

Chang, K., Hsu, C., Chen, M., & Kuo, N. (2017). How a

branded website creates customer purchase intentions.

Total Quality Management & Business Excellence,

30(3–4), 422–446.

https://doi.org/10.1080/14783363.2017.1308819

Chen, C., & Chang, Y. (2018). Telematics and Informatics

What drives purchase intention on Airbnb?

Perspectives of consumer reviews, information

quality, and media richness. Telematics and

Purchase Intention of e-Payment: The Substitute or Complementary Role of Brand, Sales Promotions, and Information Quality

307

Informatics, 35(5), 1512–1523.

https://doi.org/10.1016/j.tele.2018.03.019

Chesney, T., Chuah, S.-H., Dobele, A. R., & Hoffmann,

R. (2017). Information Richness and Trust in V-

Commerce: Implications for Services Marketing.

Journal of Services Marketing, 31(3), 295–307.

https://doi.org/https://doi.org/10.1108/JSM-02-2015-

0099

Chin, P. N., Isa, S. M., & Alodin, Y. (2019). The impact

of endorser and brand credibility on consumers’

purchase intention: the mediating effect of attitude

towards brand and brand credibility. Journal of

Marketing Communications, 1–17.

https://doi.org/10.1080/13527266.2019.1604561

Davis, K., Maddock, R., & Foo, M. (2017). Catching up

with Indonesia’s fintech industry. Law and Financial

Markets Review, 11(1), 33–40.

https://doi.org/10.1080/17521440.2017.1336398

Devita, V. D. (2019, August 12). Siapa Aplikasi E-wallet

dengan Pengguna Terbanyak di Indonesia?

https://iprice.co.id/trend/insights/e-wallet-terbaik-di-

indonesia/

Ferdiana, A. M. K., & Darma, G. S. (2019).

Understanding Fintech Through GoPay. International

Journal of Innovative Science and Research

Technology, 4(2), 257–260.

Franedya, R., & Bosnia, T. (2018, January 10). Ini Dia

Empat Jenis Fintech di Indonesia. CNBC Edukasi

Fintech.

https://www.cnbcindonesia.com/tech/20180110145

800-37-1126/ini-dia-empat-jenis-fintech-di- indonesia

Hair, J., & Anderson, R. (1998). Multivariate Data

Analysis 5th Edition. New York: Prentice Hall

International, Inc.

Hall, J. D., Palsson, C., & Price, J. (2018). Is Uber a

substitute or complement for public transit? Journal of

Urban Economics, 1-6. doi:10.1016/j.jue.2018.09.003

Hasim, M. A., Jabar, J., & Murad, M. A. (2019). A

Preliminary Research on Consumer Acceptance in

Kujath, C. L. (2011). Facebook and MySpace:

Complement or Substitute for Face-to-Face

Interaction? Cyberpsychology, Behavior, and Social

Networking, 14(1-2), 75-78. doi:DOI:

10.1089/cyber.2009.0311

Mady, T. (2017). What makes up intentions to purchase

the pioneer? A theory of reasoned action approach in

India and the USA. International Journal of Emerging

Markets, 13(5), 734–757.

https://doi.org/https://doi.org/10.1108/IJoEM-01-

2017-0007

Putri, A. T. K., & Noer, B. A. (2017). Information

Richness, Retailer Brand, Extended Offers pada Niat

Beli Konsumen Menggunakan T-Cash. Jurnal Sains

Dan Seni ITS, 6(1), 1–6.

https://doi.org/10.12962/j23373520.v6i1.21317

Riduwan, & Akdon. (2006). Rumus dan Data dalam

Aplikasi Statistika. Bandung: Alfabeta.

Santini, F. D. O., Vieira, V. A., Hoffmann, C., & Perin, M.

G. (2016). Meta-Analysis of the Long- and Short- Term

Effects of Sales Promotions on Consumer Behavior.

Journal of Promotion Management, 22(3),425–442.

https://doi.org/10.1080/10496491.2016.1154921

Tariq, M., Nawaz, M. & Butt, H. (2013). Customer

Perceptions About Branding and Purchase Intention:

A Study of FMCG in a Emerging Market. Journal of

Basic and Applied Scientific Research, 3 No.2, 341.

Wang, Z., Jiang, Z., Ren, Z., Tang, J., & Yin, D. (2018). A

Path-constrained Framework for Discriminating

Substitutable and Complementary Products in E-

commerce. Proceedings of the Eleventh ACM

International Conference on Web Search and Data

Mining (pp. 619-627). Marina Del Rey: WSDM.

doi:10.1145/3159652.3159710

Yen, Y. S. (2014). The interaction effect on customer

purchase intention in e-commerce: A comparison

between substitute and complement. Asia Pacific

Journal of Marketing and Logistics, 26(3), 472–493.

https://doi.org/10.1108/APJML-07-2013-0080

ICAESS 2020 - The International Conference on Applied Economics and Social Science

308