Stock Trend Prediction using Financial Market News and BERT

Feng Wei and Uyen Trang Nguyen

Department of Electrical Engineering and Computer Science, York University, 4700 Keele Street, Toronto, Canada

Keywords:

Language Model, Information Extraction, Neural Networks, Natural Language Processing, Financial Market,

Stock Market, Financial and Business News.

Abstract:

Stock market trend prediction is an attractive research topic since successful predictions of the market’s future

movement could result in significant profits. Recent advances in language representation such as Generative

Pre-trained Transformer (GPT) and Bidirectional Encoder Representations from Transformers (BERT) models

have shown success in incorporating a pre-trained transformer language model and fine-tuning operations to

improve downstream natural language processing (NLP) systems. In this paper, we apply the popular BERT

model to leverage financial market news to predict stock price movements. Experimental results show that our

proposed methods are simple but very effective, which can significantly improve the stock prediction accuracy

on a standard financial database over the baseline system and existing work.

1 INTRODUCTION

Recently, a new language representation model

named Bidirectional Encoder Representations from

Transformers (BERT) (Devlin et al., 2019) has

achieved huge successes in many natural language

processing tasks such as natural language inference,

question answering, named entity recognition, etc. In

this paper, we apply BERT to financial data modeling

to predict stock price movements.

Traditionally neural networks have been used to

model stock prices as time series for forecasting pur-

poses, such as in (Kaastra and Boyd, 1996; Adya and

Collopy, 1998; Zhu et al., 2008). In these earlier

works, due to the limited training data and computing

power available back then, shallow neural networks

were used to model various types of features extracted

from stock price data sets, such as historical prices

and trading volumes to predict future stock yields and

market returns.

Lately, in the community of natural language pro-

cessing, many methods have been proposed to ex-

plore additional information (mainly online text data)

for stock forecasting, such as financial news (Ding

et al., 2016; Xie et al., 2013; Hu et al., 2018; Peng

and Jiang, 2016), Twitter sentiments (Si et al., 2014;

Nguyen and Shirai, 2015; Xu and Cohen, 2018) and

financial reports (Lee et al., 2014). For example, (Hu

et al., 2018) propose to mine news sequences di-

rectly from a text with hierarchical attention mech-

anisms for stock trend prediction, where they apply

the self-paced learning mechanism to imitate effec-

tive and efficient learning. (Xu and Cohen, 2018) pro-

pose a new deep generative model jointly exploiting

text and price signals. Their model introduces recur-

rent, continuous latent variables for better treatment

of stochasticity, and uses neural variational inference

to address the intractable posterior inference.

In this paper, we propose to use the recent BERT

model to leverage on-line financial news to predict fu-

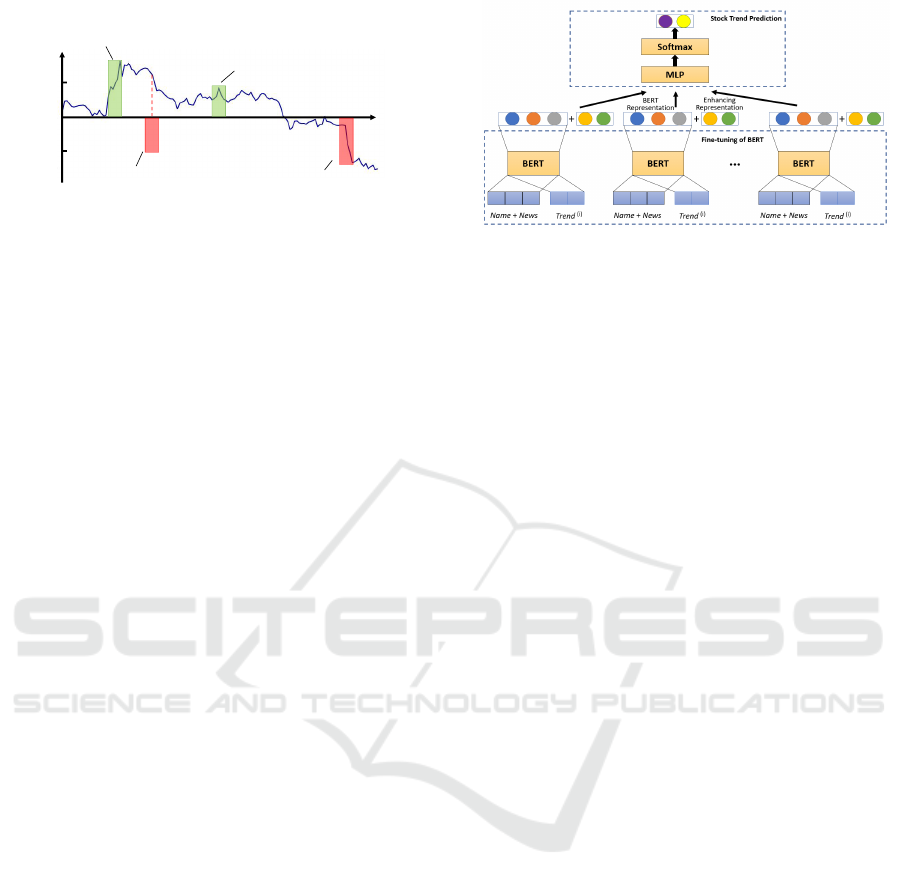

ture stock movements. Figure 1 shows how events re-

ported in the news in August 2018 affected the stock

price movement of Tesla Inc. The proposed model

combines historical price information with financial

news for more accurate predictions. We conducted

experiments on real-world data sets and experimental

results show that representations of financial news us-

ing BERT are very effective. Its incorporated enhanc-

ing semantics representations can significantly im-

prove the prediction accuracy over a model that relies

only on historical price information. Our BERT-based

model also provides more accurate predictions than

previous works (Ding et al., 2016; Hu et al., 2018;

Peng and Jiang, 2016).

The remainder of the paper is organized as fol-

lows. Section 2 presents existing work in the field of

stock trend prediction. Section 3 describes our pro-

posed neural model based on financial market news

and BERT for the stock trend prediction task. Sec-

tion 4 discusses experimental results and compares

Wei, F. and Nguyen, U.

Stock Trend Prediction using Financial Market News and BERT.

DOI: 10.5220/0010172103250332

In Proceedings of the 12th International Joint Conference on Knowledge Discovery, Knowledge Engineering and Knowledge Management (IC3K 2020) - Volume 1: KDIR, pages 325-332

ISBN: 978-989-758-474-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

325

+5%

-5%

Date

Aug 7, 2018

Musk tweets that he has “funding

secured” to take Tesla private.

Fluctuation

Aug 8, 2018

The Wall Street Journal reports SEC

inquiries into Musk tweet.

Aug 13, 2018

Musk reports interest from Saudi

investors.

Aug 17, 2018

Musk gives tearful interview

to The New York Times.

Figure 1: Example of news (CNN.com) influence of Tesla

Inc. Rectangular highlight amplitude of stock price move-

ments resulting from actual events.

the performance of our proposed model with that of

existing state-of-the-art systems. Finally, Section 5

sums up the paper with concluding remarks.

2 RELATED WORK

Stock market prediction has attracted a great deal

of attention across the fields of finance, computer

science, and other research communities. The lit-

erature on stock market prediction was initiated

by economists (Keynes, 1937). Subsequently, the

influential theory of Efficient Market Hypothesis

(EMH) (Fama, 1965) was established, which states

that the price of a security reflects all of the informa-

tion available and that everyone has a certain degree

of access to the information. EMH had a significant

impact on security investment and can serve as the

theoretical basis of event-based stock price movement

prediction.

Various studies have found that financial news can

dramatically affect the share price of a security. (Cut-

ler et al., 1988) was one of the first to investigate

the relationship between news coverage and stock

prices, since empirical text analysis technology has

been widely used across numerous disciplines. These

studies primarily use bags-of-words to represent fi-

nancial news documents. However, as (Xie et al.,

2013) point out, bag-of-words features are not the

best choice for predicting stock prices, and they ex-

plore a rich feature space that relies on frame semantic

parsing. (Wang and Hua, 2014) use the same features

as (Xie et al., 2013), but they perform non-parametric

kernel density estimation to smooth out the distribu-

tion of features. These can be regarded as extensions

to the bag-of-word method. The drawback of these

approaches is that they do not directly model events,

which have structured information.

There have been efforts to model events more

directly (Fung et al., 2002; Feldman et al., 2011).

Apart from events, to further model the long-term

Figure 2: The Architecture of our proposed stock price pre-

diction model.

dependency in time series, recurrent neural net-

works (RNN), especially Long Short-Term Memory

(LSTM) network, have also been employed for stock

price movement prediction (Akita et al., 2016; Gao,

2016).

(Peng and Jiang, 2016) proposed a system to

leverage financial news to predict stock movements

based on word embedding and deep learning tech-

niques. Our proposed model incorporates the rep-

resentation of financial news using BERT, yielding

higher accuracy than their model.

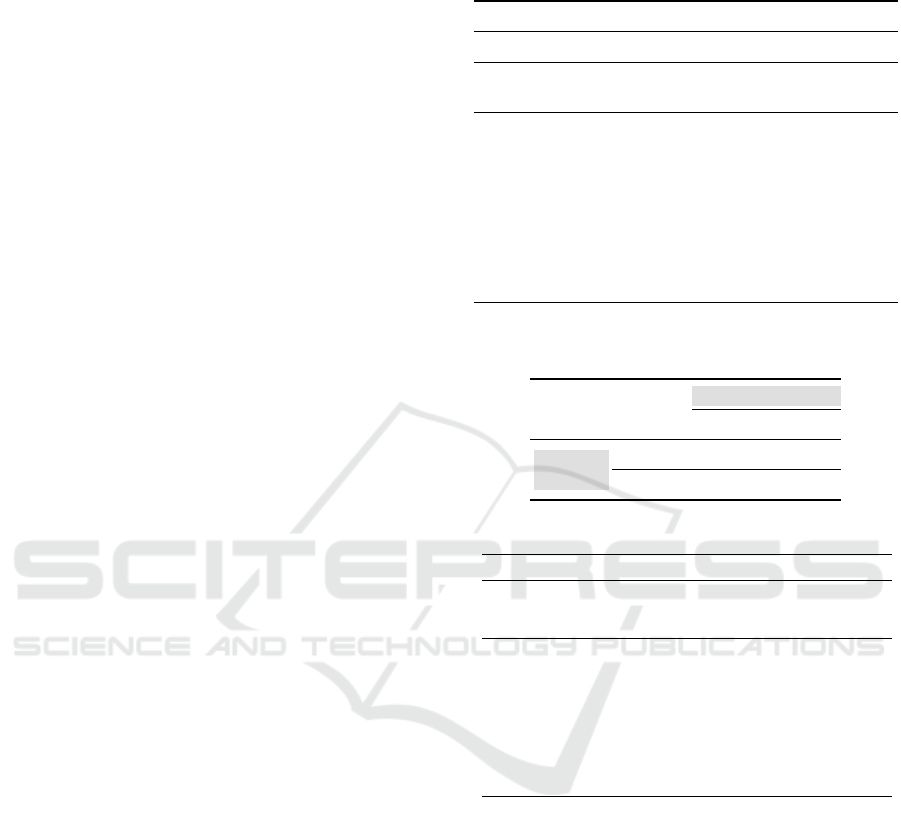

3 THE PROPOSED MODEL

The network architecture of our model is shown in

Figure 2. The input of BERT is comprised of two

parts as sentence A and sentence B, as shown in

Figure 3. In this work, sentence A is the concatena-

tion of the stock name with the related news in which

it appears, while sentence B is the stock trend based

on its next day’s closing price consulted from the Cen-

ter for Research in Security Prices (CRSP) financial

database (crs, 2018). We feed the inputs into BERT

and obtain the BERT representation, the fine-tuned

embedding of stock with related news and trends as

the BERT features. Specifically, the BERT represen-

tation is learned via BERT to indicate the relation of

sentence A and sentence B. In addition, we incor-

porate enhancing semantics (i.e., bag-of-keywords,

polarity score, and category presentation) from on-

line financial news that have been proved to be ef-

fective. Finally, we train a discriminative network to

predict the referred future trend (either up or down)

for stocks.

3.1 BERT Representation

Language model pre-training has shown to be very

effective for learning universal language representa-

tions by leveraging large amounts of unlabeled data.

KDIR 2020 - 12th International Conference on Knowledge Discovery and Information Retrieval

326

Figure 3: The network of fine-tuning BERT, based on news-

trend pairs from our financial news corpus.

Some of the most prominent models are ELMo (Pe-

ters et al., 2018), GPT (Radford et al., 2018), and

BERT (Devlin et al., 2019). Among these, ELMo

uses a bidirectional LSTM architecture, GPT exploits

a left-to-right transformer architecture, while BERT

uses the bidirectional transformer architecture.

There are two existing strategies for applying

pre-trained language models to downstream tasks:

feature-based and fine-tuning. The feature-based ap-

proach, such as ELMo, uses task-specific architec-

tures that include the pre-trained representations as

input features. The fine-tuning approaches, such

as GPT and BERT, introduce minimal task-specific

parameters and train on the downstream tasks by

jointly fine-tuning the pre-trained parameters and

task-specific parameters. This two-stage framework

has been demonstrated to be very effective in vari-

ous natural language processing tasks, such as reading

comprehension (Radford et al., 2018) and NLI (De-

vlin et al., 2019).

Inspired by (Devlin et al., 2019), it is essential to

embed stock news and trends into the same semantic

space constraining similar stock news and trends be-

ing close to each other, while dissimilar ones being

far away. In this work, as shown in Figure 3, we learn

the embeddings by fine-tuning the BERT model with

a large number of news-trend pairs from our financial

news corpus. We train our model by iterating over the

texts and mining the news-trend pairs in the corpus. In

the original BERT model, it utilizes the next sequence

prediction strategy where two sentences A and B are

fed into the model to predict whether B comes fol-

lowing A or not. This strategy drives the model to

learn better embeddings of both tokens and sentences

by mining their semantic information.

In this work, strategies are developed in construct-

ing the training data of our model to make the training

process more reasonable. For example, we are given a

sentence, “Musk, co-founder and chief executive offi-

cer of Tesla Motors, tweeted he had funding secured”.

Firstly, as shown in Figure 3, we retain the sentence

containing the stock name as the news information to

form part of sentence A. Secondly, when there are

multiple stock names in a sentence, the model will

be confused at which stock name we are interested

in. To address this problem, we set the sentence A

as the union of the stock name and the stock news

sentence it lies in, which both include the news in-

formation and emphasizes the stock name. Generally

speaking, we fine-tune the model by treating the stock

name and its news as sentence A while the trend as

sentence B, and they are separated with a special to-

ken [SEP]. The label of name-trend pair is based on

its next day’s closing price consulted from the Center

for Research in CRSP database. As for this example,

price-up is 1 while the price-down is 0, respectively.

Similar to pre-trained BERT, we predict the relation

of stock name and trend by adding a fully-connected

layer and softmax on top of the BERT representation

BERT

FT

, which is formulated as a classification task.

3.2 Enhancing Data from Historical

Prices

Given a stock s, let t and p

x

denote a target date and

the closing price of s on date x, respectively. Using

the CRSP database (crs, 2018), we retrieve the closing

prices of s on the five days before t to form a vector

p = (p

t−5

, p

t−4

, p

t−3

, p

t−2

, p

t−1

). To further enhance

the data, we compute the first and second order differ-

ences ∆p and ∆∆p as follows:

∆p = (p

t−4

, p

t−3

, p

t−2

, p

t−1

) −

(p

t−5

, p

t−4

, p

t−3

, p

t−2

)

∆∆p = (∆p

t−3

, ∆p

t−2

, ∆p

t−1

) −

(∆p

t−4

, ∆p

t−3

, ∆p

t−2

)

The enhancing data representation for each stock on a

particular date is given by R

D

= [p;∆p; ∆∆p].

3.3 Enhancing Semantics from

Financial News

We follow (Peng and Jiang, 2016) to preprocess the

text data from financial market news corpora. The

articles are first divided into sentences, and only the

sentences that contain at least a stock symbol, stock

name or company name are kept. Each of these sen-

tences is then labeled using the publication date of the

original article and the stock name. Such a sentence

may mention more than one stock, in which case the

sentence is labeled multiple times, once for each men-

tioned stock.

The sentences are then grouped based on the pub-

lication dates and the stock names to form the sam-

Stock Trend Prediction using Financial Market News and BERT

327

ples. A sample is defined as a list of sentences in ar-

ticles published on the same date and mentioning the

same stock/company. Using the closing price differ-

ence between the published date and its following day

(computed from the CRSP database), we label each

sample as “positive” (price going up the next day) or

“negative” (price going down the next day).

To retrieve enhancing semantics from financial

news for the samples, we apply the following meth-

ods (Peng and Jiang, 2016): constructing bag-of-

keywords, computing polarity scores, and category

representation.

Constructing Bags-of-Keywords. We first initial-

ized the vector representations for all words occurring

in the training set. Following [19], we manually se-

lected a small set of nine seed words, namely, ‘jump’,

‘gain’, ‘slump’, ‘drop’, ‘surge’, ‘rise’, ‘shrink’, ‘fall’,

‘plunge’, which are considered to be strong indica-

tions of stock price movements. We then performed

an iterative searching process to collect other useful

keywords. In each iteration, we compute the cosine

distance between each seed word and other words

occurring in the training set. The cosine distance

represents the similarity between two words in the

word vector space. For example, based on the pre-

calculated word vectors, we have found other words,

such as ‘tumble’, ‘slowdown’, ‘rebound’, ‘decline’,

and ‘climb’, which have similar meaning or closely

related to one or more seed words listed earlier. The

top ten most similar words were chosen and added

to the set of seed words at the end of each iteration.

The newly added seed words were used to repeat the

searching process to find another top ten most sim-

ilar words, increasing the size of the seed word set

with each iteration. The search process stopped when

the seed word set reached 1,000 words, including the

nine initial seed words. We found that the derived

keywords in the final set are very similar in meaning

as long as the seed words in the starting set are strong

indications of stock price movements. In the last step,

we generated a bag-of-keywords, a 1000-dimension

feature vector, for each sample after weighting a list

of selected keywords with term frequency–inverse

document frequency (tf-idf): R

K

∈ R

1000

.

Computing Polarity Scores. Polarity scores (Tur-

ney and Pantel, 2010) can be used to measure how ac-

curate each keyword indicates stock movements and

the extent of the accuracy. To compute the polarity

score, we first compute the point-wise mutual infor-

mation for each keyword w as follows (Turney and

Pantel, 2010):

PMI(w, pos) = log

freq(w, pos) × N

freq(w) × freq(pos)

, (1)

where freq(w, pos) denotes the frequency of the key-

word w occurring in all positive samples, N de-

notes the total number of samples in the training set,

freq(w) denotes the total number of keyword w occur-

ring in the whole training set and freq(pos) denotes

the total number of positive samples in the training

set. The polarity score for each keyword w can the be

calculated as follows:

PS(w) = PMI(w, pos) − PMI(w, neg). (2)

It should be noted that when a stock s is men-

tioned in a sentence, the keyword w in the sentence

may not indicate the price movement of s. For exam-

ple, given the sentence “Google lost half its market

share and slipped into third place behind Amazon and

Baidu in the second quarter of 2019”, which contains

the keyword ‘slip’. In this sentence, Google is asso-

ciated with keyword ‘slip’ while Amazon and Baidu

are not. If the sentence is used as a sample for Google,

the polarity score of ‘slip’ is computed as in Eq. (2).

On the other hand, if this sentence is used as a sam-

ple for Amazon or Baidu, the polarity score of ‘slip’

is flipped by multiplying by -1. To determine whether

a polarity score should be flipped or not, we used the

Stanford parser (Manning et al., 2014) to determine

whether the target stock is a/the subject of the key-

word. If it is, the polarity score stays as is. Otherwise,

the sign of the polarity score is flipped. Finally, after

being weighted with tf-idf, the polarity score repre-

sentation R

P

∈ R

1000

is obtained for each sample.

Category Representation. Certain types of market

events are frequently reported in the news such as a

company coming out with a new product, acquiring or

merging another company, etc. The stock price of the

company usually changes accordingly after the publi-

cation of such news. To take into account this factor in

our model, we use a list of categories (Peng and Jiang,

2016) that indicate such events or activities of pub-

licly listed companies, namely, new products, acqui-

sition, price rise, price drop, law suits, fiscal reports,

investment, bankrupt, government, analyst highlights.

For each category, we manually assigned a set of

words that are closely related to the category. For

example, ‘accumulated’, ‘allocate’, ‘funds’, ‘loaned’

can be seed words of the category investment to de-

scribe an investment. We used BERT WordPiece em-

bedding and an iterative search process as describe

above to expand the list of keywords associated with

each category. Words that have the cosine distances

closest to those in the current seed word sets are se-

lected until each category reaches 100 words.

KDIR 2020 - 12th International Conference on Knowledge Discovery and Information Retrieval

328

After the above process is completed, we counted

the total number of occurrences of each word in each

category. We then obtained a category representation

as R

C

= (logN

1

, logN

2

, ..., logN

c

), where N

c

is the to-

tal number of times the words in category c appear in

the sample. In the case where N

c

is zero, it is replaced

by a large negative number (e.g., -999.9) in this paper.

3.4 Predicting Price Movements of

Unmentioned Stocks

The prediction system described above are applicable

to only stocks that are reported in the media. How-

ever, there are many stocks that are rarely or never

mentioned in the news. (The New Stock Exchange

has 2,800 companies listed.) In this section we ex-

tend the above system to predict price movements of

stocks that are not mentioned in the news (unmen-

tioned stocks).

The extension includes the use of a stock correla-

tion graph illustrated in Figure 4. A stock correlation

graph is an undirected graph in which each vertex rep-

resents a stock and the edge between two vertices rep-

resents the correlation between the two stocks. The

edge is assigned a weight indicating the correlation

coefficient (ranging from -1 and 1) between the two

stocks. The higher the correlation coefficient, the

more impact one stock has on the other (and vice

versa) in terms of price movement. For example, very

often prices of stocks in the same sector, e.g., energy,

move in tandem with each other due to an event, e.g.,

an oil crash, resulting in a positive coefficient between

two stocks in the sector. To predict price movements

of unmentioned stocks on a particular day, the above

system is used to predict price movements of stocks

mentioned in the news. The obtained results are then

propagated in the graph using the correlation coef-

ficients to predict price movements of unmentioned

stocks.

To build the correlation graph, we selected the

top 5,000 stocks from the CRSP database (crs, 2018)

based on their market capitals and retrieved their clos-

ing prices for the seven years between January 1, 2012

and December 31, 2018. For every pair of stocks in

the set, we kept only the stock pairs that have an over-

lapped trading period of at least 252 days, the number

of trading days in one year. (Stocks can be added to or

removed from the stock market.) The minimum dura-

tion of one year ensures the reliability of the derived

correlation coefficient. During the process of con-

structing the graph, we discarded the edges whose ab-

solute correlation values are smaller than 0.8 as they

were deemed unreliable. In future work, we will as-

sess how this threshold of correlation coefficient af-

Figure 4: Illustration of a part of correlation graph which

contains eight stocks. The symbol in the circle are the ticker

name of the stock. The value along the edges are the corre-

lation score of the two stocks connected by that edge.

fects the prediction performance.

To predict price movements of the unmentioned

stocks, we first run our BERT model to obtain pre-

diction results from the mentioned stocks. The results

are then used to construct a vector x ∈ R

5000

. Each of

the 5,000 dimensions is associated with a stock and

has two values output by our BERT model indicat-

ing the probability of price going up and down re-

spectively. If a sample is identified as ‘price-down’,

its probability is multiplied by -1 to be distinguished

from a ‘price-up’ probability. For the unmentioned

stocks, the two probability values are set to zero.

Let A ∈ R

5000×5000

be a symmetric matrix that rep-

resents the correlation graph. The propagation pro-

cess through the graph can be implemented as a ma-

trix multiplication as follows: x

0

= Ax.

The graph propagation is repeated multiple time

until x

0

converges, which contains predicted price

movements of the unmentioned stocks.

4 EXPERIMENTS AND ANALYSIS

4.1 Data Collection

The financial news data used in this paper, which con-

tains 212,347 articles from CNN and 238,265 from

CNBC, was collected. The news articles were pub-

lished in the period from January 2012 to December

2018. For each news article, the publication times-

tamp, title, and content were extracted. Then, each of

the collected news to a specific stock was correlated,

if the news mentioned the name of the stock in the title

or content. Finally, the news without any correlation

to stocks was filtered out.

The historical stock security data are obtained

from the CRSP database, which is published by the

Chicago Business School and is widely used in finan-

cial modeling. The CRSP database is properly ad-

Stock Trend Prediction using Financial Market News and BERT

329

justed for all special price events such as stock splits

as well as dividend yields. We only use the security

data from 2012 to 2018 to match the period of finan-

cial news. For the following experiments, we split the

dataset into a training set (85%) from January 2012

to May 2016, and a test set (15%) from June 2016 to

December 2018. Then we further randomly sample a

validation set from the training set with 10% size of it,

to optimize the hyper-parameters and choose the best

epoch.

4.2 Stock Trend Prediction using BERT

and Enhancing Semantics

The model in this work has two networks to train, in-

cluding the fine-tuning of BERT and the stock trend

prediction module, we will detail the parameter set-

ting as follows.

In the first set of experiments, we use our BERT

model to predict stock trends based on a variety of

enhancing semantics, namely bag-of-keywords (R

K

),

polarity score (R

P

) and category presentation (R

C

).

Considering the memory consumption of GPU, we

exploit the uncased BERT

BASE

model for fine-tuning,

where the model consists of 12 layers, with 768 hid-

den units and 12 heads. Therefore, the BERT rep-

resentation, BERT

FT

, we obtained is of length 768.

As for fine-tuning over our financial news corpus,

all hyper-parameters are tuned on the development

set. The maximum length, dropout probability and

batch size we used are 50, 0.1 and 128, respectively.

AdamW (Loshchilov and Hutter, 2018) is applied for

optimization with an initial learning rate of 5e-5. The

maximum number of epochs is selected from [20, 30,

40].

Specifically, we use the enhancing data represen-

tation (R

D

) and BERT

FT

to create the baseline and

various enhancing semantics derived from the finan-

cial news are added on top of it. We measure the

final performance by calculating the accuracy and

Matthews Correlation Coefficient (MCC) on the test

set. As shown in Table 1, the enhancing semantics

derived from financial news can significantly improve

the prediction accuracy and MCC score. According

to the results in the table, baseline model incorpo-

rating R

P

yields higher accuracy than R

K

and R

C

.

Moreover, baseline model incorporating R

P

and R

P

yields higher accuracy than the other two combina-

tions. Additionally, we have obtained the best perfor-

mance, i.e., an accuracy score of 58.4% and an MCC

score of 0.33, by using all the enhancing represen-

tations discussed in Sections 3.2 and 3.3. We have

also applied the event embeddings (Ding et al., 2016)

and news embeddings (Hu et al., 2018) to the baseline

Table 1: Performance comparison of stock trend prediction

on the test set.

System Accuracy (%) MCC

(Peng and Jiang, 2016) (word embedding) 55.5 0.25

(Ding et al., 2016) (event embedding) 56.0 0.28

(Hu et al., 2018) (news embedding) 55.8 0.26

R

D

52.3 0.18

Baseline = R

D

+ BERT

FT

54.9 0.22

Baseline + R

K

55.2 0.24

Baseline + R

C

55.1 0.23

Baseline + R

P

55.8 0.24

Baseline + R

K

+ R

C

56.0 0.26

Baseline + R

K

+ R

P

57.7 0.28

Baseline + R

C

+ R

P

55.9 0.25

Baseline + R

K

+ R

C

+ R

P

58.4 0.33

Table 2: The results of 2-by-2 contingency table from a ran-

dom classifier and our baseline model (R

D

+ BERT

FT

).

Baseline

Correct Incorrect

Random

Guess

Correct 1501 942

Incorrect 1114 1443

Table 3: Results of the McNemar test of our BERT models.

System Accuracy (%) χ

2

p-value

Random Guess 49.8 n/a n/a

(Ding et al., 2016) (event embedding) 56.0 69.05 9.60 × 10

−17

(Hu et al., 2018) (news embedding) 55.8 50.49 1.20 × 10

−12

R

D

52.3 14.39 0.00015

Baseline = R

D

+ BERT

FT

54.9 23.48 1.26 ×10

−6

Baseline + R

K

55.2 28.67 8.58 ×10

−8

Baseline + R

C

55.1 26.52 2.61 × 10

−7

Baseline + R

P

55.8 34.53 4.20 × 10

−9

Baseline + R

K

+ R

C

56.0 42.55 6.89 × 10

−11

Baseline + R

K

+ R

P

57.7 66.31 3.85 × 10

−16

Baseline + R

C

+ R

P

55.9 36.72 1.36 × 10

−9

Baseline + R

K

+ R

C

+ R

P

58.4 74.42 6.32 × 10

−18

and the results are also listed in Table 1, which shows

that our enhancing semantic representations produce

better performance in predicting a pool of individual

stock price trends.

Furthermore, the accuracy of our best model

(Baseline + R

K

+ R

C

+ R

P

) is much higher than

(Peng and Jiang, 2016) (i.e., 2.9%, 58.4% vs 55.5%).

It confirms the effectiveness of representations of fi-

nancial news using BERT.

To verify the significance of different models by

comparing the result of different enhancing represen-

tation combinations with the result of random clas-

sifier (the results are generated by random guess), we

applied the McNemar test (McNemar, 1947), which is

a statistical experiment used on paired nominal data.

McNemar’s test is applied on a 2-by-2 contingency

table, which tabulates the outcomes of two tests on a

KDIR 2020 - 12th International Conference on Knowledge Discovery and Information Retrieval

330

sample of n subjects. In a McNemar test, a null hy-

pothesis is defined such that the marginal probabilities

in the contingency table are the same, whereas an al-

ternative hypothesis is defined such that the marginal

probabilities are not the same.

In particular, we define the null hypothesis as fol-

lows: the predictive performances of our BERT mod-

els with different enhancing representation combina-

tions would be the same as the random classifier. For

the results of each enhancing representation combi-

nation listed in Table 1, we created a 2-by-2 contin-

gency table with the results generated by the random

classifier and our baseline model with solely enhanc-

ing data representation (R

D

), as shown in Table 2.

Each cell in Table 2 shows the matched result counts

of these two classifiers. For instance, the top-left cell

shows the number of results predicted correctly by

both of the random classifier and our baseline model

with solely enhancing data representation (R

D

). The

McNemar test statistic χ

2

value computed using this

table is 14.39 which has a p-value 0.00015. After

constructing such a 2-by-2 contingency table for each

of our BERT models with different enhancing repre-

sentation combinations, we compute their χ

2

and p-

value, results are shown in Table 3. The p-values are

shown in Table 3 are significantly lower than the typ-

ical α value of 0.001, which provides strong evidence

to reject the null hypothesis of a random guess.

4.3 Prediction Results for Unmentioned

Stocks

We use our best model (Baseline + R

K

+ R

C

+ R

P

) to

conduct the experiment in this section. We group all

outputs from that model based on the dates of all sam-

ples on the test set. For each date, we create a vector x

based on the model prediction results for all observed

stocks and zeros for all unmentioned stocks, as de-

scribed in section 3.4. Then, the vector is propagated

through the correlation graph to generate another set

of stock movement prediction. During the propaga-

tion, we compute the results by multiplying the vec-

tor with the correlation matrix. After the propagation

converges, we may apply a threshold (τ ∈ [0, 1]) on the

propagated vector to prune all low-confidence predic-

tions. For example, as shown in Figure 4, we only

keep correlation connections when correlation score

above τ. The prediction of all unmentioned stocks

is compared with the actual stock movement on the

next day. Experimental results are shown in Figure 5,

where the left curve shows the prediction accuracy

and the right curve shows the percentage of unmen-

tioned stocks predicted out of the 5000 stocks per day

under various pruning thresholds. For example, using

a large threshold 0.9, we can predict with an accuracy

of 58.4% the price movements of 441 unmentioned

stocks per day, in addition to 112 reported stocks per

day on the test set.

0.5 0.6 0.7 0.8 0.9

0.44

0.46

0.48

0.50

0.52

0.54

0.56

0.58

0.60

Accuracy

Threshold

Accuracy

(a) Accuracy

0.5 0.6 0.7 0.8 0.9

0.06

0.12

0.18

0.24

0.30

0.36

Percentage of unmentioned prediction

Threshold

Percentage of unmentioned prediction

(b) Percentage of unmentioned stocks predicted

Figure 5: Predicting unmentioned stocks via correlation.

5 CONCLUSION

In this paper, we propose a model using the most re-

cent state-of-the-art language model BERT to predict

moving directions of future stock prices. Moreover,

we incorporate a correlation matrix which makes use

of the underlying relationships among stocks to ex-

pand our predictive results. Experimental results

show that our proposed methods are simple but very

effective, which can significantly improve the stock

prediction accuracy on a standard financial database

over the baseline system and existing work.

It should be noted that being able to predict the

moving direction of stock prices does not necessar-

ily lead to beating the market consistently. First, a

certain type of trading strategy is required to be com-

bined with the predictive results to make meaningful

profit. Second, the amount of price change is another

factor that should be used to compute the return on

investment before making trade decisions. Therefore,

the developments of a set of trading strategies and a

system that predicts the return on investment are po-

tential future research topics.

Stock Trend Prediction using Financial Market News and BERT

331

REFERENCES

(2018). Crsp data description guide for the crsp us stock

database and crsp us indices database. Chicago Booth,

Center for Research in Security Prices, The University

of Chicago Graduate School of Business.

Adya, M. and Collopy, F. (1998). How effective are neural

networks at forecasting and prediction? a review and

evaluation. Journal of Forecasting, 17(5-6):481–495.

Akita, R., Yoshihara, A., Matsubara, T., and Uehara, K.

(2016). Deep learning for stock prediction using nu-

merical and textual information. In 2016 IEEE/ACIS

15th International Conference on Computer and In-

formation Science (ICIS), pages 1–6. IEEE.

Cutler, D. M., Poterba, J. M., and Summers, L. H. (1988).

What moves stock prices?

Devlin, J., Chang, M.-W., Lee, K., and Toutanova, K.

(2019). Bert: Pre-training of deep bidirectional trans-

formers for language understanding. In Proceedings

of the 2019 Conference of the North American Chap-

ter of the Association for Computational Linguistics:

Human Language Technologies, Volume 1 (Long and

Short Papers), pages 4171–4186.

Ding, X., Zhang, Y., Liu, T., and Duan, J. (2016).

Knowledge-driven event embedding for stock predic-

tion. In Proceedings of COLING 2016, the 26th Inter-

national Conference on Computational Linguistics:

Technical Papers, pages 2133–2142.

Fama, E. F. (1965). The behavior of stock-market prices.

The Journal of Business, 38(1):34–105.

Feldman, R., Rosenfeld, B., Bar-Haim, R., and Fresko, M.

(2011). The stock sonar-sentiment analysis of stocks

based on a hybrid approach. In Twenty-Third IAAI

Conference.

Fung, G. P. C., Yu, J. X., and Lam, W. (2002). News

sensitive stock trend prediction. In Pacific-Asia Con-

ference on Knowledge Discovery and Data Mining,

pages 481–493. Springer.

Gao, Q. (2016). Stock market forecasting using recur-

rent neural network. Master’s thesis, University of

Missouri–Columbia.

Hu, Z., Liu, W., Bian, J., Liu, X., and Liu, T.-Y. (2018).

Listening to chaotic whispers: A deep learning frame-

work for news-oriented stock trend prediction. In Pro-

ceedings of the Eleventh ACM International Confer-

ence on Web Search and Data Mining, pages 261–269.

ACM.

Kaastra, I. and Boyd, M. (1996). Designing a neural net-

work for forecasting financial and economic time se-

ries. Neurocomputing, 10(3):215–236.

Keynes, J. M. (1937). The general theory of employment.

The Quarterly Journal of Economics, 51(2):209–223.

Lee, H., Surdeanu, M., MacCartney, B., and Jurafsky, D.

(2014). On the importance of text analysis for stock

price prediction. In LREC, pages 1170–1175.

Loshchilov, I. and Hutter, F. (2018). Decoupled weight de-

cay regularization.

Manning, C. D., Surdeanu, M., Bauer, J., Finkel, J. R.,

Bethard, S., and McClosky, D. (2014). The stanford

corenlp natural language processing toolkit. In Pro-

ceedings of 52nd annual meeting of the association

for computational linguistics: system demonstrations,

pages 55–60.

McNemar, Q. (1947). Note on the sampling error of the

difference between correlated proportions or percent-

ages. Psychometrika, 12(2):153–157.

Nguyen, T. H. and Shirai, K. (2015). Topic modeling based

sentiment analysis on social media for stock market

prediction. In Proceedings of the 53rd Annual Meet-

ing of the Association for Computational Linguistics

and the 7th International Joint Conference on Natural

Language Processing (Volume 1: Long Papers), pages

1354–1364.

Peng, Y. and Jiang, H. (2016). Leverage financial news

to predict stock price movements using word embed-

dings and deep neural networks. In Proceedings of

the 2016 Conference of the North American Chapter

of the Association for Computational Linguistics: Hu-

man Language Technologies, pages 374–379.

Peters, M. E., Neumann, M., Iyyer, M., Gardner, M., Clark,

C., Lee, K., and Zettlemoyer, L. (2018). Deep con-

textualized word representations. In Proceedings of

NAACL-HLT, pages 2227–2237.

Radford, A., Narasimhan, K., Salimans, T., and Sutskever,

I. (2018). Improving language understanding by gen-

erative pre-training.

Si, J., Mukherjee, A., Liu, B., Pan, S. J., Li, Q., and Li,

H. (2014). Exploiting social relations and sentiment

for stock prediction. In Proceedings of the 2014 Con-

ference on Empirical Methods in Natural Language

Processing (EMNLP), pages 1139–1145.

Turney, P. D. and Pantel, P. (2010). From frequency to

meaning: Vector space models of semantics. Journal

of Artificial Intelligence Research, 37:141–188.

Wang, W. Y. and Hua, Z. (2014). A semiparametric gaus-

sian copula regression model for predicting financial

risks from earnings calls. In Proceedings of the 52nd

Annual Meeting of the Association for Computational

Linguistics (Volume 1: Long Papers), pages 1155–

1165.

Xie, B., Passonneau, R., Wu, L., and Creamer, G. G. (2013).

Semantic frames to predict stock price movement. In

Proceedings of the 51st Annual Meeting of the Associ-

ation for Computational Linguistics, pages 873–883.

Xu, Y. and Cohen, S. B. (2018). Stock movement predic-

tion from tweets and historical prices. In Proceed-

ings of the 56th Annual Meeting of the Association for

Computational Linguistics (Volume 1: Long Papers),

pages 1970–1979.

Zhu, X., Wang, H., Xu, L., and Li, H. (2008). Predicting

stock index increments by neural networks: The role

of trading volume under different horizons. Expert

Systems with Applications, 34(4):3043–3054.

KDIR 2020 - 12th International Conference on Knowledge Discovery and Information Retrieval

332