Shared Service Centers as a Tool for Intellectual Capital

Management

Agostinho Sousa Pinto

1a

, Eusébio Costa

2b

and Paulo Alves

3

1

CEOS.PP, ISCAP, Polytechnic of Porto, Rua Jaime Lopes Amorim s/n, S. Mamede de Infesta, Portugal

2

Instituto de Estudos Superiores de Fafe, Fafe, Portugal

3

Instituto Federal Triângulo Mineiro, Brazil

Keywords: Shared Service Center, Organizational Knowledge Management, Intellectual Capital Management,

e-Business.

Abstract: In the search for organizational models to improve quality, efficiency and effectiveness, we are faced with

the paradigm of Shared Service Centers (SSC) and Intellectual Capital Management (ICM). SSC have

demonstrated great success in organizational management and ICM is considered one of the most important

assets for the survival of organizations. In a public administration context, the challenge has been to demonize

- to state that these two realities can bring benefits to the organization and leverage a process of change.The

present study was developed with the objective of recognizing Factors that Benefit and Factors that

Discourage the implementation of a SSC and, in addition, it was studied how the SSC can enhance the ICM

in the analysed institution.

With a positivist epistemological positioning and a quantitative and qualitative methodological approach, the

case study method was applied. Empirical data were collected through document analysis and a questionnaire

survey. From the data collected, the internal consistency of the indices was analysed, using the Cronbach

Alpha coefficient, the absolute and relative frequencies for each indicator, the Level of Concordance of the

statements and the Pearson correlation between the indicators of each group.

This research also demonstrates that the SSC model in public administration enhances the ICM by improving

the quality and gain in efficiency and effectiveness of services provided.

1 INTRODUCTION

Nowadays, when changes occur quickly and

continuously to meet internal and external demands,

managers must be attentive to business models that

produce efficiency and effectiveness in processes.

The institution researched was a Medium and

Higher education institution located in the Mining

Triangle State in Brazil, is a public school of the

Federal Government, linked to the MEC - Ministry of

Education and Culture. This Institution originated

from the fusion of old schools, which became a

Campus of this new one; later, from its enlargement

with the creation of other college campus, linked to a

Rectory.

In the search for organizational models, we come

across the paradigm of Shared Service Centers - SSC,

a

https://orcid.org/0000-0003-1454-030X

b

https://orcid.org/0000-0003-4167-2455

which uses the sharing of support functions. Thus,

this work has investigated whether the

implementation of a SSC can collaborate positively,

directly or indirectly in Intellectual Capital

Management in the context.

Considering the fact that SSC are an emerging

model and still little used, especially in the Brazilian

public administration, this study also aims, besides

the general and specific objectives defined, to

contribute to disseminate this model of service

organization, establishing, in a systematized and

enlightening manner, knowledge on such an

emerging theme, so that public administrators and

managers have subsidies to explore an organizational

model that aims to improve efficiency and

effectiveness in public administration (Pinto, 2015);

Schulman, Harmer, Dunleavy, & Lusk, 2001; Quinn,

Cooke, & Kris, 2000).

Pinto, A., Costa, E. and Alves, P.

Shared Service Centers as a Tool for Intellectual Capital Management.

DOI: 10.5220/0010011201450153

In Proceedings of the 17th International Joint Conference on e-Business and Telecommunications (ICETE 2020) - Volume 3: ICE-B, pages 145-153

ISBN: 978-989-758-447-3

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

145

The present research was developed with the

objective of recognizing Factors that Benefit and

Factors that Disadvantage the implementation of a

SSC, and, additionally, it was studied how the SSC

can enhance the Intellectual Capital Management in

the analysed institution.

With an interpretative epistemological

positioning and quantitative and qualitative

methodological approach, the case study method was

applied. Empirical data were collected using

document analysis and a questionnaire survey. The

questionnaire, in addition to characterizing the

sample, has twenty-nine partial indicators, divided

into three global indicators that evaluated the

Favourable Factors, the Unfavourable Factors and the

Indicators of Intellectual Capital Management.

Thus, the question of investigation to which an

answer was attempted was:

Can the implementation of a Shared Services

Centre collaborate positively, directly or indirectly in

Intellectual Capital Management in the context of the

Institute of High and Higher Education?

Considering the research in question, it is clear

that the implementation of a Shared Services Centre

collaborates positively in Intellectual Capital

Management in the context of the Institute of Higher

Education.

In addition to the introduction presented in the

first section, this paper includes the second section

presenting the purpose of the study and the state of

the art. In the third section the methodological

approach is defined and presented. In the fourth

section the results are presented, analysed and

discussed. In the fifth section the conclusions and

future work are presented.

2 PURPOSE OF STUDY AND

STATE OF THE ART

With the emergence of Systems Theory,

organizations and companies began to be seen

assuming their systemic nature. In this sense, it was

from the study of living beings that the concept of

open systems emerged, extending to other disciplines

and to Administration, so a system is considered: (i)

"a set of elements", which are the components; (ii)

"dynamically interrelated", establishing

communications and relationships of dependence

between them; (iii) "developing an activity or

function", this being the process that transforms

inputs; (iv) "to achieve one or more objectives or

purposes", which constitutes its purpose (Chiavenato,

1994, pp. 58-59).

Being seen as systemic entities but also as open

systems, they influence and are influenced by the

environment in which they are inserted (systems and

microsystems), so it is not indifferent the

management model they adopt.

2.1 Management Models and the

Shared Service Center

For Correia (2003, p. 3), each organization being a

unique business, defining a model in this context is

inevitably complicated. Such models must be

flexible, adaptable and capable of dealing with the

pressures of constant change as well as with the views

of experienced managers on how things should be

done.

In the shared services model, there is management

control in the administration of the business unit, and

there may be some influence from the parent

company. The revenue of the shared services unit is

usually determined by contractual agreements, which

guarantee the supply of goods and services of

specified quality and quantity. In this case, as in an

independent, profit-sharing business operation,

employee rewards are based on customer satisfaction.

In this model, increased efficiency, gain in

economies of scale, standardization of technology

and processes as well as responses to the needs of the

group companies are some advantages. The main

disadvantages are culture changes for business unit

employees, high start-up costs and some duplication

in administrative and managerial effort (Bergeron,

2003, pp. 18-19).

Shared Services is a concept based on a

collaborative strategy in which selected transversal

services, common to several business units of an

organization, are concentrated in business units that

promote efficiency and effectiveness. It is based on

three principles: standardization, consolidation and

reengineering, strongly dependent on Information

and Communication Technologies (Pinto, 2015, p. 3).

2.2 Shared Service Center in Public

Administration

Porter (1992) deals with what he calls the value chain,

distinguishing primary activities from support

activities. He understands that primary activities are

those that are part of the core business of the business,

being unique and carried out by sectors that have the

competence to do so; while support activities can be

standardized, not being unique among business units

E-BDT 2020 - Special Session on E-Business and Digital Transformation

146

and, therefore, can be shared - Porter also called them

support activities. However, according to Pinto

(2015, p. 54), although support or support activities

are basically transferred to the SSC, this transfer does

not rule out the possibility that, in some situations and

if there is interest, main or primary activities may be

carried out in the same way by the SSC. According to

Granjeiro (2000, p. 16), the group of organs and

entities, established by the Public Power, State, for

the attainment of the common good, is what is called

Public Administration.

One of the factors that distinguish private from

public administration is in relation to its principles

and characteristics, since while private administration

is oriented to profit and shareholders' interests, so that

the collective interest is served by the market, public

administration is explicitly and directly supported for

the satisfaction of the public interest.

Public administration is as important as it is

complex, whatever the society. Thus, effective public

administration can determine development for

society; conversely, inefficient or unbalanced public

administration, in a short period of time, leads a

society from decline to destruction (Wiig K. M.,

2000). In this context, the term effectiveness is used

because efficient was no longer enough, and there is

a need to do efficiently what was paramount; thus, the

concept of effectiveness emerges: knowing how to do

the right tasks right (Granjeiro & Castro, 2000).

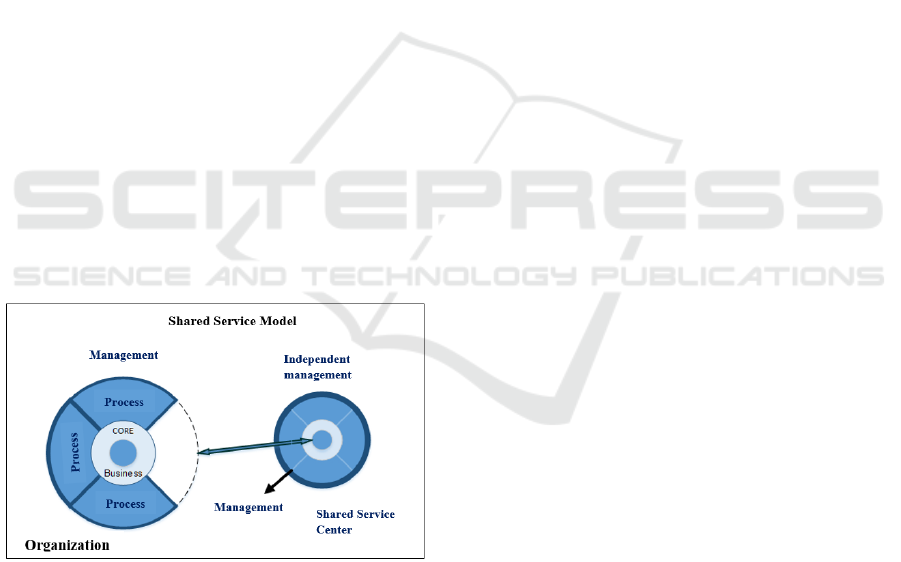

Figure 1 presents the Shared Services

Management Model, based in Bergeron (2003).

Figure 1: Shared Services Model.

For Pereira (1996), the federal public

administration had three moments: until 1930,

Patrimonial State; between 1930 and 1995,

Bureaucratic State; and from 1995, Managerial State.

2.3 Intellectual Capital Management

The term "knowledge society" has been highlighted

by Drucker (1993) since the early 1990s, when

knowledge management gained importance and was

considered a success factor for organizations. The

author highlights that "today the really controlling

resource, the absolutely decisive factor of production,

is not capital, land or labour. It is knowledge" (p. 15).

Drucker recognizes that "today value is created by

productivity and innovation, which are applications

of knowledge to work" (p. 16).

Stewart (1998) corroborates this statement,

highlighting that knowledge is an intangible asset

more important than capital and labour, becoming a

generator of wealth; hence the importance of

identifying, creating, storing, sharing and applying

this good.

Nonaka & Takeuchi (1997, p. 7) explain that

knowledge expressed in a clear and objective manner

is defined as explicit knowledge, which can be easily

communicated in such a way that it can be used

systematically and formally, becoming practical and

useful knowledge.

As for the intellectual capital of organizations,

Edvinsson & Malone (1998) refers to it not only as an

intellectual human activity, but also as a context in

which intellectual property is included as part of their

intangible assets, as well as names, brands, training,

technological leadership and all formal knowledge

about the organization's employees (p. 197). They

also ensure that, for organizations in the knowledge

society, what matters in creating value while keeping

them attractive and sustainable is intellectual capital.

For Hammer & Champy (1994) management

must reinvent itself in order to respond to four

problems: the company's objective, its culture, its

performance problems and resource management.

As for knowledge, it is the information

assimilated by the individual, coming from

experience, research, innovation, that is, it happens

through the process of understanding information.

Davenport (1998, p. 18) states that knowledge is the

precious information of the human mind, comprising

reflection, synthesis and context, being its structuring

and transfer complex.

The other current of literature discusses

knowledge as an organizational asset that must be

managed in a way that improves organizational

performance (Pinto, 2015). A relevant contribution of

this current was the introduction of the concept of

intellectual capital (CI), which corresponds to the

organizational knowledge that was freely applied by

the people in favour of the organizations,

incorporating and increasing the knowledge retained

by them. The objective of supporting managers to

identify and classify the components of an

organization's intellectual capital.

Shared Service Centers as a Tool for Intellectual Capital Management

147

Employee competencies such as their leadership

and change management capabilities determine the

success of the organization's transformation. The

challenge is not only to hire human resources, but also

to manage them in an evolutionary way, in

accordance with the evolution of the organization

itself. Effective HR management has the advantages

of tailoring resources to needs, keeping them up to

date, involved, and motivated. Keeping a motivated

team is one of the key challenges and critical success

factors of a Shared Services Center.

3 METHODOLOGICAL

APPROACH

This section describes the methodology applied to

solve the research question and to achieve the

objectives determined in the research.

According to Descartes, "The method is the art of

guiding reason in the sciences" (Morin, 2005). In this

sense, through scientific methodology, the researcher

seeks to solve the proposed problem and the

objectives of the study, as well as to search for a new

perception or truth in relation to a certain studied

reality.

3.1 Research Objectives

The research question that guides this work is: "Can

the implementation of a Shared Services Center

collaborate positively, directly or indirectly in

Intellectual Capital Management in the context of the

Federal Institute of the Mining Triangle?

This question resulted in the elaboration of the

main objective of the research: "to recognize which

factors benefit the implementation of a SSC, which

factors disfavor this implementation and how the SSC

can potentiate the Intellectual Capital Management

for the Patrimony Management in the Federal

Institute?

3.2 Method

The research question to which this research was

intended to answer is: "Can the implementation of a

Shared Services Centre collaborate positively,

directly or indirectly in Intellectual Capital

Management in the context of the Institute?

This research is based on the taxonomy presented

by Gil (2002) and Vergara (1998), which typifies it in

terms of objectives or ends and procedures or means.

Regarding the objectives, this research is

considered exploratory and descriptive considering

that it intends to describe the perceptions and

understandings of managers and administrators,

regarding the themes under study.

With regard to procedures or means, the research

follows the case study method, supported by

bibliography, documentary analysis and analysis of

data collected using questionnaire survey.

As for the sample, analysing the assumptions of

Lakatos and Marconi (2003) regarding research by

means of questionnaires, we have: "On average, the

questionnaires sent by the researcher reach 25% of

return" (p. 201). Hill & Hill (2002, p. 91) also find it

normal that response rates to a questionnaire do not

exceed 30%.

Through a questionnaire survey, a total of 263

employees were invited to participate, of which 160

responded; this corresponded to 60.8% of the total

number of respondents.

To avoid interference and contact with the

researcher, the survey was applied through Google

Form, an online platform for collecting survey data.

The SPSS Statistics 17.0 software was used for

statistical analysis of the data.

3.3 Data Collection Instruments

After superior authorization, the participants

received, through their institutional e-mail, the link to

answer the online questionnaire through an invitation

letter to participate in the research as well as the Term

of Free and Informed Consent. This document is

required in Brazil in investigations involving people.

A two-part questionnaire was used to carry out the

research. The first identified the profile of the

respondents, gender, age group, schooling, length of

service in the Institution, relationship with the sector

investigated and whether or not he holds a

management position or a gratified position, which

represents who the managers or coordinators of the

Institution are.

The second part of the questionnaire, based on the

existing literature, was divided into three groups of

questions: the first group, composed of 12 questions,

which sought to know the level of agreement

regarding the factors favorable to the creation of an

SSC; the second group, with 8 questions, sought to

verify the factors unfavorable to this creation and the

third group, with 9 questions, sought to identify the

aspects related to the management of Intellectual

Capital.

Cronbach’s Alpha is a coefficient that measures

the internal consistency of a questionnaire. Its

E-BDT 2020 - Special Session on E-Business and Digital Transformation

148

application in the context of Social Sciences, a

coefficient more than 0.90 is considered "very good";

from 0.80 to 0.9 is considered "good"; an internal

consistency coefficient between 0.70 and 0.80 is

considered acceptable. In some studies, internal

consistency values from 0.60 to 0.70 are accepted,

which, according to the literature, is "weak".

Also for the validation of the questionnaire, a pre-

test was applied in order to improve and increase the

reliability and validity of the data collection

instrument. The pre-test questionnaire was answered

by a group of 14 collaborators; it was intended to

evaluate the time for its completion, clarity and

understanding during the response process.

4 ANALYSIS AND DISCUSSION

OF RESULTS

This section presents the results of the research.

Regarding gender, our respondents are 56,9% male

and 43,1% female. In relation to age, the majority of

respondents are between 26 and 35 years old, with a

total of 76.3% until the age of 45. Another interesting

fact is that the participants up to 25 and over 56

represent 10%. As for academic background, it is

evident that 71.9% of the respondents have a

Specialization, MBA or Master degree. Regarding the

length of service, 78.1% of the respondents are up to

9 years old, of which 18.1% have up to 3 years of

service. Regarding the Employees who participated in

the investigation, it should be noted that 45.6% of the

respondents hold a management position or rewarded

position. Inquiring respondents about their

knowledge of the Shared Services Centre, it was

found that 70% of the participants consider it to be the

first time they have had contact with it or have only

heard about it;

4.1 Analysis of the Results of the

Favourable Factors

To check the degree of internal consistency the

coefficient of consistency "Cronbach's alpha " was

applied, which had an internal consistency of 0.927,

according to Table 1. According to the literature it is

considered "good reliability" or "high reliability".

From a more detailed analysis it can be inferred

that, if the indicator "Enables better insertion of

outsourcers." were excluded, the value of Cronbach's

alpha coefficient would increase from 0.927 to 0.929.

As the 12 indicators refer to favourable factors,

the total average of the Concordance Level was

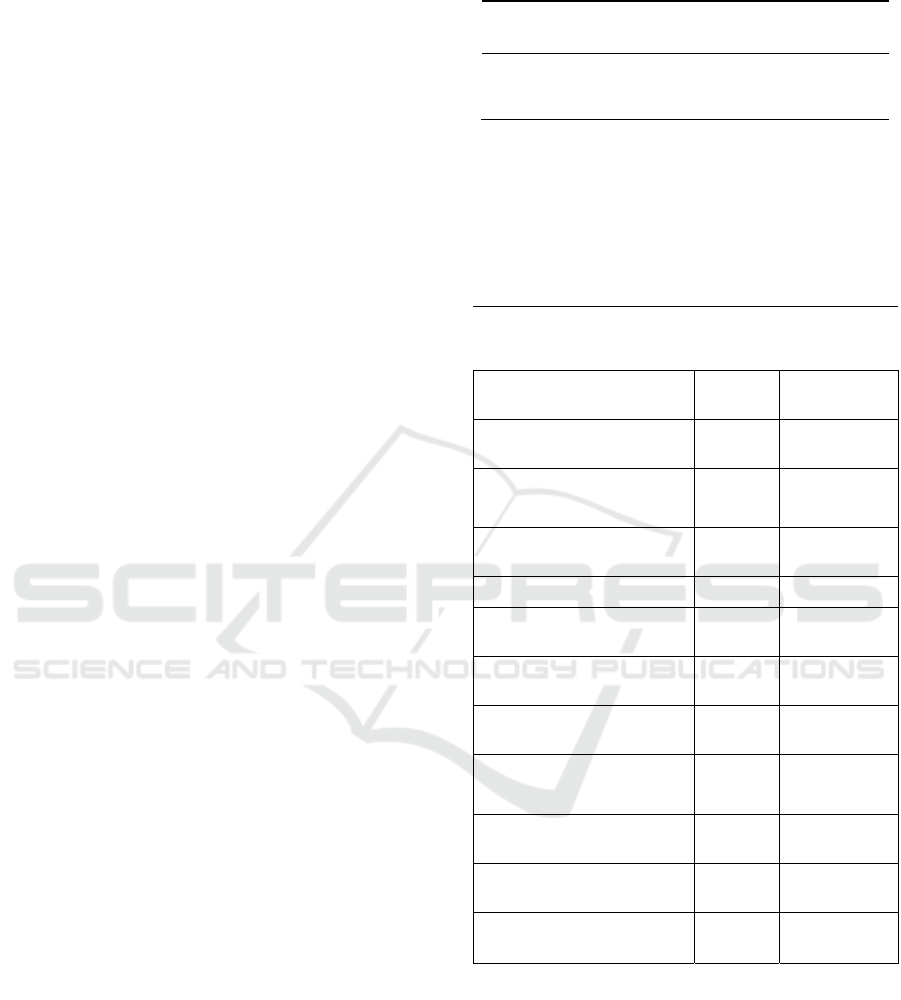

Table 1: Reliability Statistics - Favourable Factors.

Reliability statistics

Cronbach’s Alpha No. Items

0,927 12

calculated, obtaining a value of 3.96; this

demonstrates that the respondents have concordance

(partial or total) for this group of factors. The Table

2 below represents the favourable factors organized

by level of agreement.

Table 2: Favourable Factors in Order of Agreement Level.

Favorable Factors

Level

Concord

ance

Result

Standardizes services 4,4

high

agreement

Opportunities to review how

the service is provided

4,2 agreement

It enables the institution to

improve the allocation of its

resources.

4,1 agreement

Improves control over the

services provided.

4,1 agreement

Reduces operating costs 4,1 agreement

Increases the efficiency of

management related activities

4,1 agreement

It speeds up decisions and

processes

4,0 agreement

Strengthens information

technology tools

4,1 agreement

It contributes to the

qualification of the servers

involve

d

3,9 agreement

Reduces jobs in long-term

asset management.

3,8 agreement

Improves the image in society 3,6 No opinion

Allows better insertion of

outsourcers

3,3 No opinion

The correlation between the favourable factors was

also calculated, from which some conclusions can be

drawn:

it is verified that the correlations present a

degree of significance equal or inferior to 0.01;

this indicates that one can be sure of 99% of the

results;

the correlation is positive among the indicators;

this indicates that the variation among them is

directly proportional.

Shared Service Centers as a Tool for Intellectual Capital Management

149

From the analysis to the data, it can be verified that

the questions that obtained the best correlation

intensity in the results were:

the correlation between the indicator " It

enables the institution to improve the allocation

of its resources " and two indicators " Reduces

operating costs" (0.744) and " Increases the

efficiency of management related activities "

(0.707);

the correlation between the indicator " It speeds

up decisions and processes" and " Increases the

efficiency of management related activities "

(0.735).

4.2 Analysis of the Results of the

Unfavourable Factors

To check the degree of internal consistency the

coefficient of consistency "Cronbach's alpha" was

applied, which had an internal consistency of 0,785,

according to Table 3.

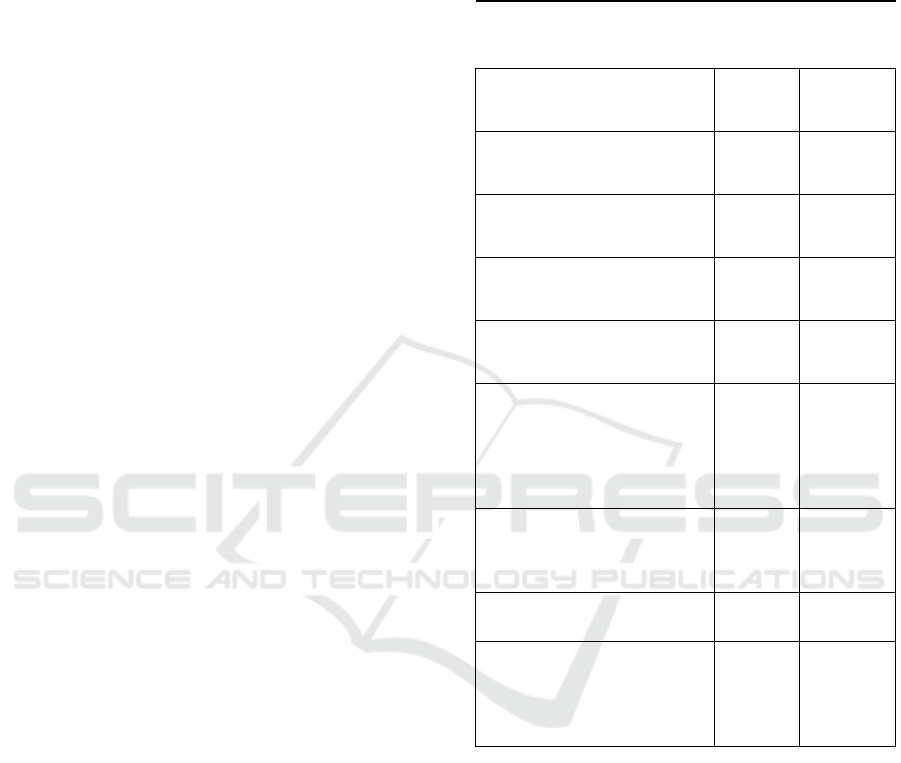

Table 3: Reliability Statistics - Unfavourable Factors.

Reliability statistics

Cronbach’s Alpha No. Items

0,785 8

From the data obtained it can be inferred that if

the indicator "Incompatibility between the

information technology tools used..." were excluded

from the analysis, the value of the total Cronbach Alfa

would increase from 0.785 to 0.789.

The Unfavourable Factors for the creation of a

Shared Services Centre for heritage management

were also tested on the basis of eight piecemeal

indicators that inquired about the level of agreement

or disagreement, with a set of statements relating

essentially to management, cultural and human

aspects, which involve potential risks that should be

managed and minimized.

The correlation between the unfavourable Factors

was also calculated. From the results obtained it is

possible to draw some conclusions:

it was found that, for these indicators, the

correlations can present i) the degree of

significance equal to or less than 0.01, this

indicates that one can be sure of 99% of the

results; ii) the degree of significance equal to or

less than 0.05: this indicates that one can be

sure of 95% of the results;

the correlation is positive between the

indicators; this indicates that the variation

between them is directly proportional.

Table 4: Unfavourable Factors in Order of Agreement

Level.

Unfavourable Factors

Level

Concordance

Results

Managers may want to

avoid taking the risk of

failure

3,4

willingness

to agree

Faces resistance from the

servers involved

3,4

willingness

to agree

Lack of compatibility as to

managers' expectations.

3,3

willingness

to agree

Lack of institutional

support.

3,2

willingness

to agree

Problems due to cultural

differences

3,1

willingness

to disagree

Lack of evidence to justify

the cost vs benefit of

creatin

g

a SSC

3,0

willingness

to disagree

Incompatibility between

the information

technology tools used.

2,9

willingness

to disagree

It makes budgetary control

difficult

2,3

disagree

From the analysis to the data, it can be verified that

the questions that obtained the biggest correlation

intensity in the results were:

the correlation between the indicator

"Managers may not want to assume the risks of

implementation failure" and two indicators

"Lack of compatibility regarding managers'

expectations" (0.689) and "Faces resistance

from the servers involved" (0.669);

the correlation between the indicator "Lack of

institutional support" and "Faces resistance

from the servers involved" (0.508).

4.3 Analysis of the Results of

Intellectual Capital Management

To check the degree of internal consistency the

coefficient of consistency "Cronbach's alpha" was

applied, which had an internal consistency of 0,806,

which is considered "good" or "moderate to high

reliability".

Table 5: Reliability Statistics - Intellectual Capital

Managements.

Reliability statistics

Cronbach’s Alpha No. Items

0,806 9

E-BDT 2020 - Special Session on E-Business and Digital Transformation

150

From the data analysed, it can be inferred that if

the indicators "The institution has specialists to deal

with new and more complex problems" and "All

problems or challenges are first discussed and shared

in the institution, before a solution is proposed and

disclosed" were excluded from the analysis, the value

of the total Cronbach Alfa would increase from 0.806

to 0.823 and 0.816 respectively.

The Intellectual Capital Management of a Shared

Services Center for asset management at the Institute

was also tested on the basis of nine piecemeal

indicators that inquired about the level of agreement

or disagreement, with a set of statements relating

essentially to the relative effectiveness and efficiency

of these indicators.

From the analysis of the results of the Intellectual

Capital Management of a Shared Services Centre

presented, some conclusions can be drawn that seem

relevant to us:

there is homogeneity in the responses to the

indicators under analysis;

approximately 60% of the respondents agree

(partially or totally) with the indicators under

analysis, except for the indicators "All

problems or challenges are first discussed and

shared within the institution, before a solution

is proposed and disclosed", "The institution has

specialists to deal with new and more complex

problems" and "There has been concern in

structuring the knowledge, fostering its sharing

by other sectors of the organization";

the percentage of disagreement (partial or

total) tends towards 10%;

The number of respondents who neither

agree nor disagree tends to be 25%.

The correlation between the indicators relating to the

management of intellectual capital was also

calculated. Some conclusions can be drawn from this:

The correlations were found to be 0.01 or less

significant: this indicates that 99% of the

results can be guaranteed;

the correlation is positive among the indicators;

this indicates that the variation among them is

directly proportional.

From the analysis to the data it is possible to verify

that the questions that obtained the best correlation

intensity in the results were:

the correlation between the indicator "Enables

the institution to capture and retain the

knowledge of its employees" and two

indicators "Allows managing a set of skills

based on theoretical or academic knowledge"

(0.698) and "Manage current problems,

following standards to solve them efficiently"

(0.672);

Table 6: Intellectual Capital Management in order of

agreement level.

Intellectual Capital

Managements

Level

Concordance

Results

Manage current problems by

following standards to solve

them efficiently.

4,0

agreement

Manage a set of capabilities to

be harnessed or disseminated

throughout the organization.

4,0

agreement

It allows managing a set of

skills based on theoretical or

academic knowled

g

e.

3,9

agreement

The production of knowledge

is based on the experience of

the em

p

lo

y

ees.

3,9

agreement

It allows the institution to

capture and retain the

knowled

g

e of its em

p

lo

y

ees.

3,9

agreement

In addition to the work

routines, my sector has the

additional purpose of

supporting other departments

of the organization in its

functional

p

rocess.

3,9

agreement

There has been concern to

structure knowledge, fostering

its sharing by other sectors of

the organization.

3,4

agreement

The institution has specialists

to deal with new problems

3,1

willingness

to agree

All problems or challenges are

first discussed and shared

within the institution, before a

solution is proposed and

disclosed.

2,8

willingness

to agree

the correlation between the indicator "Allows

managing a set of skills based on theoretical or

academic knowledge" and "Manage current

problems, following standards to solve them

efficiently". (0,694).

5 CONCLUSION AND FUTURE

WORK

The focus of this work was on the key question of

investigation:

Can the implementation of a Shared Services

Center collaborate positively, directly or

Shared Service Centers as a Tool for Intellectual Capital Management

151

indirectly in Intellectual Capital Management

in the context of the Federal Institute?

To answer the research question, a synopsis of the

main research evidence was presented.

It was evidenced that there was receptivity of the

subject by the servers in general, which was

characterized by the total of answers obtained to the

questionnaire, 60.8%, being 45.6% of these answers

made by the managers of the Institution; what

demonstrates the interest of the investigation on the

part of these stakeholders.

It is worth mentioning that 70% of the participants

considered it to be the first time they had contact with

this subject or that they had only heard about it; this

lack of knowledge in public service is pointed out, in

the literature, by several authors. In a more critical

analysis, this may also be due to ignorance of the term

SSC.

The sample was characterized in relation to

gender, age, literary qualification, position and

working time in the company.

Additionally, the first analysis to be performed

was related to the quality of the questionnaire

analysed by the Cronbach Alfa Coefficient. The

investigation revealed that for the Favourable Factors,

the internal consistency is 0.927, which is considered

of "high reliability"; for the Unfavourable Factors, the

internal consistency is 0.785, which is considered of

"moderate reliability" and, for the indicators referring

to Intellectual Capital Management, the internal

consistency is 0.806, which is considered of

"moderate to high reliability".

The second analysis was on the level of

agreement. For the Favourable Factors, the value

obtained was 3.96, showing agreement (total or

partial); for the Unfavourable Factors the value

obtained was 3.08 and for Intellectual Capital

Management 3.65.

This indicates that, in the Institution investigated,

there is a higher degree of agreement for the aspects:

Favorable Factors for the creation of a CSC and

Intellectual Capital Management, while for the

Unfavorable Factors, the degree of agreement is

lower. Thus, the CSC model, as a strengthening for

Intellectual Capital Management, can be adopted for

Heritage Management, in the Institute's investigated

units.

Among the Favors that stand out the most, where

there is the greatest agreement, were: Standardization

of services; Opportunity for a review of how the

service is provided today; Enables the institution to

better target its resources and Improves control over

the services provided, which corroborates with the

existing literature. And those that stood out the least

were: It allows for a better insertion of outsourced

personnel and Improves the image of the Institute in

society.

Of the Unfavourable Factors that stood out the

most, in which there is greater agreement, were:

Managers may not want to assume the risks of failure

of the implementation; Faces resistance from the

servers involved and Lack of compatibility as to the

expectations of managers. And the ones that stood out

the least were: Difficult budgetary control and

Incompatibility between the information technology

tools used.

Of the indicators for Intellectual Capital

Management that stood out the most, in which there

is greater agreement, were: Manage current problems,

following rules to solve them efficiently; Manage a

set of capabilities to be used or disseminated

throughout the organization and Allows managing a

set of skills based on theoretical or academic

knowledge. And the ones that stood out the least

were: All the problems or challenges are first

discussed and shared in the institution, before a

solution is proposed and disclosed; The institution has

specialists to deal with new and more complex

problems and There has been concern in structuring

the knowledge, encouraging its sharing by other

sectors of the organization.

As this investigation is carried out under the prism

of the SSC and Intellectual Capital Management, in

the sphere of the Institute's Heritage Sector, as a

proposal for future work, three aspects can be

considered:

Sectoral: expansion of the research to other

sectors of the Institute;

geographical: expansion of the geographical

area of research to other organizations of the

Institute.

institutional: extension of this research to other

institutions in the Brazilian federal education

network.

ACKNOWLEDGEMENTS

"This work is financed by portuguese national funds

through FCT - Fundação para a Ciência e Tecnologia,

under the project UIDB/05422/2020".

REFERENCES

Bergeron, B. P. (2003). Essential of Shared Services. New

Jersey: John Wiley & Sons, Inc.

E-BDT 2020 - Special Session on E-Business and Digital Transformation

152

Chiavenato, I. (1994). Administração Teoria, Processo e

Prática. (2ª ed.). São Paulo: Makron Books

Correia, A. R., & Mesquita, A. (2014). Mestrados &

Doutoramentos - Estratégias para a elaboração de

trabalhos científicos: o desafio da excelência (2ª ed.).

Porto, Portugal: Vida Económica - Editorial, SA.

Davenport, T. H., & Prusak, L. (1998). Conhecimento

empresarial: como as organizações gerenciam seu

capital intelectual. Rio de Janeiro: Campus.

Drucker, P. (1993). A sociedade pós-capitalista. São Paulo:

Pioneira

Edvinsson, L., & Malone, M. S. (1998). Capital intelectual:

descobrindo o valor real de sua empresa pela

identificação de seus valores internos. São Paulo:

Makron Books.

Ferreira, C. (2010). Centros de Serviços Compartilhados

como Instrumento de Gestão Regional no Setor

Público. Dissertação, (Dissertação de Mestrado em

Administração) - Universidade Municipal de São

Caetano do Sul - USCS, São Paulo.

Gil, A. C. (2008). Métodos e técnicas de pesquisa social. (6ª

ed.). São Paulo: Editora Atlas S.A.

Granjeiro, J. W., & Castro, R. G. (2000). Administração

pública (5 ed.). Brasília: Vestcon.

Hammer, M. & Champy, J., Reengineering:

Revolutionizing the company in function of clients,

competition and major management changes, Editora

Campus, 1994.

Lakatos, E. M., & Marconi, M. A. (2003). Fundamentos de

metodologia científica (5ª ed.). São Paulo: Editora Atlas

S.A.

Morin, E. (2005). Ciência com consciência (8ª ed.). (M. D.

Alexandre, & M. S. Dória, Trads.) Rio de Janeiro:

Bertrand Brasil

Nonaka, I., & Takeuchi, H. (1997). Criação de

Conhecimento na Empresa: como as empresas

japonesas geram a dinâmica da inovação. Rio de

Janeiro: Campus.

Oliveira, E. R. (2013). Compartilhamento de serviços na

Administração Pública Federal: análise dis fatores de

aplicabilidade na autarquia federal. (Dissertação de

Mestrado em Sistemas de Gestão) - Universidade

Federal Fluminense - UFF, Niterói

Pereira, L. B. (1996). Da Administração Pública

Burocrática à Gerencial. Revista do Serviço Público

Brasileiro, V. 1.

Pinto, A. (2015). Um modelo para a Gestão do

Conhecimento Organizacional no contexto dos

Serviços Partilhados com recurso à utilização do e-

Learning. Tese, (Tese de Doutoramento em

Tecnologias e Sistemas de Informação) - Universidade

do Minho.

Porter, M. E. (1992). Vantagem Competitiva: Criando e

sustentando um desempenho superior (5a ed.). (E. M.

Pinho Braga, Trad.) Rio de Janeiro: Campus

Quinn, B. E., Cooke, R. S., & Kris, A. (2000). Shared

Services: Mining for Corporate Gold. Great Britain:

Pearson Education Limited.

Schulman, D. S., Harmer, M. J., Dunleavy, J. R., & Lusk,

J. S. (2001). Serviços Compartilhados: Agregando

valor às unidades de negócios. (M. J. Roque, Trad.) São

Paulo: Makron Books.

Stewart, T. A. (1998). Capital intelectual: a nova vantagem

competitiva das empresas. (11 ed.). Rio de Janeiro:

Campus

Terra, J. C. (2000). Gestão do conhecimento: o grande

desafio empresarial. São Paulo: Negócio Editora.

Vergara, S. C. (1998). Projetos e Relatórios de Pesquisa em

Administração. (2ª ed.). São Paulo: Editora Atlas S.A.

Wiig, K. M. (1997). Integrating Intellectual Capital and

Knowledge Management. Long Range Planning, 30,

pp. 399-405.

Shared Service Centers as a Tool for Intellectual Capital Management

153