R

eform and Development of Basic Telecom Service Industry in China

and Its Evaluation: A Perspective of Technological Progress

Xuchen Lin

1

, Tingjie Lu

2

and Xia Chen

3

School of Economics and Management, Beijing University of Posts and Telecommunications, 10 Xi Tu Cheng Road,

Beijing, China

1

xuchenlin19@163.com,

2

lutingjie@buptsem.cn,

3

cxbupt@263.net

Keywords: Telecom Service Industry, Reform, Evaluation.

Abstract: Basic telecommunications service industry has become one of the most essential basic industries, it reflects

a country’s competitiveness and innovative capacity. China has the largest telecommunications market over

the world, but compared with the development level of the telecommunications industry in most other

countries, China’s telecommunications technologies are relatively low and the comprehensive development

level of Chinese basic telecommunications service industry is also relatively poor. The purpose of this paper

is to carry on a comprehensive combing to the reform and development of the basic telecom service industry

in China, and evaluate the results of the reforms from a perspective of technological progress. In the last

part of this paper, we provide several policy suggestions to the next step of telecommunications regulation

in China.

1 INTRODUCTION

With the strategic significance and natural

monopoly, the basic telecommunications service

industry has been subject to strict regulations by

nearly all the countries in the world since its initial

formation. However, as the telecommunications

technologies have advanced significantly in recent

decades, basic telecom service industry has been

integrated into the daily life of the public nowadays,

and its natural monopoly is disappearing gradually

(Crawford, 2013). Therefore, since the 1980s, the

world has started an upsurge of regulation reforms in

the telecom industry.

Since the Reform and Opening-up in 1978,

China has actively seized the opportunities brought

by emerging technologies, which made China

achieve outstanding economic performance in the

past three decades. China's annual per capita GDP

increase rate achieved more than 8% in the past 38

years (1978-2015), it has transformed itself from a

backward agricultural country into the world's

second largest economy. In the year of 2014, the

total volume of telecommunications service of

Chinese basic telecommunications industry achieved

1814.95 billion RMB (Association, 2015). However,

the informatization index of China was only 0.4351

in 2014, it was ranked 88th in the world and below

the average value of 0.5494, which is in marked

contrast to China’s economic status in the

international community (Zhang, 2015). Starting

from 2014, the basic telecom service industry in

China has happened a series of regulation events,

including the introduction of virtual telecom

operators, the intention of the fourth restructuring

and further relaxing price regulation. All of which

indicate that Chinese government has formed the

idea of relaxing regulations in the telecom industry.

However, the gap between Chinese telecom industry

and that of developed countries is still wide, based

on this, this paper carries on a comprehensive

combing to the reform and development of the basic

telecom service industry in China, especially the

industry restructuring of telecom business, then

summarize current situation of the basic telecom

service industry in China and evaluate the results of

the reforms from a perspective of technological

progress, finally provides several policy suggestions

to the next step of telecommunications regulation.

Since 1994 when China Unicom was founded,

the structural regulations have been the seemingly

effective regulatory means of Chinese telecom

regulators. Under the infulence of structuralism and

overseas telecom restructuring experience, the

development and reform of the basic telecom

58

58

Lin X., Chen X. and Lu T.

Reform and Development of Basic Telecom Service Industry in China and Its Evaluation: A Perspective of Technological Progress.

DOI: 10.5220/0006443700580062

In ISME 2016 - Information Science and Management Engineering IV (ISME 2016), pages 58-62

ISBN: 978-989-758-208-0

Copyright

c

2016 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

industry in China mainly depend on introducing

market rivals by splitting and restructuring the

telecom operators expecting to form a marketing

structure of effective competition. The changes of

Chinese basic telecom service industy have attracted

many researchers’ attention. Gao and Lyytinen

studied the evolution of the regulation reform of

Chinese telecom industry, and discovered that

China’s telecom reform was a “try firstly and

implement afterwards” reform which was carried out

in the macro background of Chinese economic

reform, while other countries carried out regulation

reform firstly and then the regulations guided the

market reform. China’s telecom regulation was

relatively poor, which put a restriction on the

development of the telecom market development

(Gao and Lyytinen, 2000). Loo also studied the

development of the telecom industry in China, and

indicated the reform of Chinese telecom industry

was the result of the balance between various factors

(Loo, 2004). Li did a research on the regulation

situation of Chinese telecom industry and its efforts

on anti-monopoly, by analysing the difference of the

modes of telecom industry regulation between China

and OECD countries, he indicated independent

regulation institution plays a critical role in the

regulation reforms (Li, 2011).

2 DEVELOPMENT AND

RUGULAITON REFORM

PROCESS OF CHINESE

TELECOM INDUSTRY

2.1 Natural Monopoly Regulation

Period (before 1994)

Before 1994, China’s basic telecom service industry

was in the condition of “integrated government

function and enterprise management”, Chinese

government was not only the operator of the telecom

industry, but also the manager of the industry. In the

early formation of Chinese telecom industry, the

investment was totally from the government, so the

industry form a monopoly condition which

integrated with natural monopoly and administrative

monopoly. In fact, the posts and telecommunications

industry during this period had not formed the

marketing management, the posts and

telecommunications services were just national

facilities which served the information transmission

between party, government, and military institutions

at all levels, there was little opportunity for

individual consumers to have direct access to

telecom services. After the Reform and Opening-up

in 1978, Chinese economy developed rapidly, while

the low telecom technologies and the poor service

level became the bottleneck of restricting economic

growth. Therefore, Chinese government set out

policies of giving priority of developing telecom

industry. According to the characteristics of the

high-tech, high input for telecom industry,

government carry out diversified investment,

surrendering part of the profits to the telecom

industry, higher prices and other policies to make

sure the financial support for the telecom

infrastructure construction and technical upgrading.

However, the rapid development of Chinese

telecom industry over this period was not a benign

process of economic growth, but seizing high profits

to obtain high development speed using monopoly

position, which could not be persistent in the market

economy. With the notable expansion of market and

huge increase of demand, the inherent problems of

“integrated government function and enterprise

management” became increasingly serious, the

operational efficiency of telecom industry during

this period was quite low and its technical progress

rate did not improve notably.

2.2 Introduction of Preliminary

Competition, Separation of

Government and Enterprise (1994-

1998)

For a long time, the poor quality of telecom services

and high price were complained by consumers, and

the constraint of telecom industry on economic

development failed to be mitigated, Chinese

government started to carry out real implementation

of structural adjustment measures on the

telecommunications market. In July 1994, China

Unicom was founded, and it was the second telecom

operator which ran basic telecom services. After

China Unicom participated in the competition of

basic telecom service industry, the pace of technical

progress was accelerated, and the efficiency of the

telecom market was improved, primarily manifested

as: (1) the price level of telecommunication services

dropped sharply; (2) because the telecom industry

was no longer an absolute monopoly business

structure, telecom operators were forced to

continuously improve their service level; (3)

technological progress made terminal and phone

number separated, the sale of telecom terminals no

longer needed to bundle with network resources.

Reform and Development of Basic Telecom Service Industry in China and Its Evaluation: A Perspective of Technological

Progress

59

Reform and Development of Basic Telecom Service Industry in China and Its Evaluation: A Perspective of Technological Progress

59

The foundation of China Unicom made Chinese

basic telecom service industry transform from

monopoly to preliminary competition. However,

“integrated government function and enterprise

management” hampered the industry development,

so separating government function and enterprise

management became an inevitable choice. In 1998,

Chinese telecom industry separated government

function and enterprise management and lifted

restrictions gradually. During this period, although

the industry developed rapidly through introducing

competition, China Unicom was not comparable

with China Telecom in terms of the size of assets

and market share, the market structure and nature of

monopoly of telecom industry did not changed

essentially. Specifically, the paging service and

mobile communication developed rapidly in China

over this period, but the development of China

Unicom’s mobile service was relatively slow, the

market share of China Unicom only accounted for

5% of the whole mobile communication market,

which means it could not pose a credible threat on

China Telecom. So it was inevitable to plan to split

and restructure the telecom operators.

2.3 First Splitting and Restructuring,

Monopoly to Competition

Transformation (1999-2001)

In 1999, Chinese Ministry of Information Industry

decided to implement the splitting and restructuring

of Chinese telecom operators. The original China

Telecom was split into China Telecom, China

Mobile and China Satcom. And the splitting was a

kind of services splitting, the paging service of

original China Telecom was integrated into China

Unicom, the mobile communication and satellite

communication services left in charge of China

Mobile and China Satcom respectively. Besides,

China Netcom, China Railcom, China Jicom entered

the telecom market one after another. Chinese

telecom industry formed the competitive situation of

seven telecom operators. The business focus of all

operators during this period are listed in Table 1.

Table 1: The business distribution of telecom operators

Telecom operator

Business focus

China Telecom

Fixed networks and personal

handyphone system (PHS)

China Mobile GSM network

China Unicom

Full-service (fixed networks,

GSM, CDMA, etc.)

China Netcom

Fixed networks and personal

handyphone system (PHS)

China Jicom Fixed networks

China Railcom

Communication service along the

national railway network

China Satcom

Communication and broadcasting

services in satellite space segment

2.4 Second Splitting and Restructuring,

Further Breaking the Monopoly

(2002-2007)

The purpose of the first splitting and restructuring in

1999 is to carry out fair competition between

multiple operators in Chinese telecom market, but

China Telecom still had absolute advantage in the

services of fixed line telephone, long-distance

telephone and internet. So in order to form effective

market structure, Chinese government split China

Telecom again in 2002, this time the splitting was a

kind of region splitting, namely, China Telecom was

north-south split into new China Telecom and China

Netcom (Netcom serving the Northern provinces;

Telecom serving the southern provinces).

After this splitting and restructuring, there were

at least two operators in the basic telecom services

of international, long-distance, local, mobile, data

and line rental, forming the duopoly market

structure.

However, the splitting and restructuring this time

left large problems, which foreshadowed the

unbalanced market development in a few years.

There were two main reasons: (1) the splitting this

time was a restructuring that is according to the

scope of region, it was still service exclusive

operation or region exclusive operation in main

telecom areas including long-distance telephone,

fixed line telephone and mobile telephone services,

which meant that it did not form effective

competition essentially; (2) the policymakers

neglected the factor of technological progress, and

did not consider the rapid expansion of the scale of

mobile communication market, which leaded to the

unique outshining and market dominance of China

Mobile in the next few years.

ISME 2016 - Information Science and Management Engineering IV

60

ISME 2016 - International Conference on Information System and Management Engineering

60

2.5 Third Splitting and Restructuring,

Three Islands of Stability (After

2008)

With the rapid development and popularity of

mobile communication technologies, and due to the

factor of the issuance of third-generation mobile

licenses, the original telecom market structure was

forced to make new adjustments. In 2008, the

operating revenue of China Mobile accounted for

nearly 50% of the whole market, and the net profit

of China Mobile was almost twice the sum of the

figure for China Unicom, China Netcom and China

Telecom. In order to break the imbalance of market

due to the dominance of China Mobile, making use

of the opportunity of issuing third-generation mobile

licenses, Chinese government restructured the

telecom market once again. China Telecom acquired

the CDMA network of China Unicom, China

Unicom merged with China Netcom to form the new

China Unicom, the basic telecom service of China

Satcom was incorporated into China Telecom, China

Railcom was incorporated into China Mobile. Six

telecom operators were restructured into three

operators, namely China Mobile, China Telecom

and China Unicom. Each operator got one 3G

license, each one adopted different 3G technologies,

and full-service operation mode was carried out.

This new kind of splitting and restructuring and full-

service operation mode is to strengthen the

competition and avoid the continuation of the market

dominance of China Mobile. However, eight years

has passed so far, there is no essential change in the

competition structure in terms of market share.

China Mobile still command a strong dominance in

terms of the number of new users and total revenue.

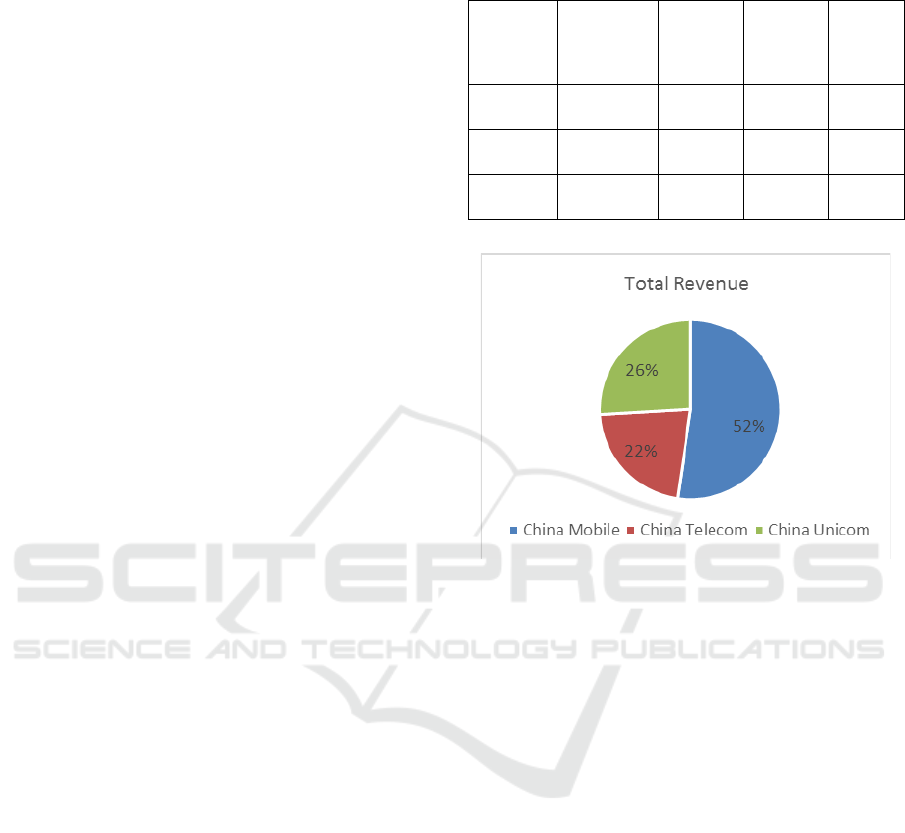

As is shown in Table 2 and Figure 1, the total

revenue and EBITDA profit of China Mobile are

both exceed the sum of the figure for China Telecom

and China Unicom, the number of 4G users of China

Mobile is approximately three times the sum of

other two operators.

Table 2: The comparison of three telecom operators in

terms of the state of operation in 2015

Telecom

operator

4G

technology

Total

Revenue

(billion

RMB)

EBITDA

Profit

(billion

RMB)

4G user

(million)

China

Mobile

TD-LTE

668.34

240.03 312

China

Telecom

FDD-LTE

277.05

94.11 58.5

China

Unicom

FDD-LTE

331.2

87.78 44.16

Data source: the annual reports of three operators in 2015

Figure 1: The comparison of three telecom operators in

terms of the total revenue in 2015

3 CONCLUSIONS AND POLICY

SUGGESTIONS

This paper analyses the development process of

Chinese basic telecom service industry, studies the

evolution route of regulation of Chinese telecom

industry, and comments on the structural regulations

of the industry. Through summarizing the reform

process of Chinese telecom industry, it is easy to

discover that until 2008 when the third splitting and

restructuring was implemented, the main tool of

market regulation is directly changing the industry

structure by administrative means, in the hope of

creating a balanced market competition structure and

realizing effective competition. We believe all

previous regulations of Chinese basic telecom

service industry is a kind of structural regulation

with the following characteristics: (1) telecom

enterprises maintain state-owned enterprise

character all the time; (2) the regulation institution

of telecom industry is non-independent, the

regulation system is multiparty regulation; (3) the

Reform and Development of Basic Telecom Service Industry in China and Its Evaluation: A Perspective of Technological

Progress

61

Reform and Development of Basic Telecom Service Industry in China and Its Evaluation: A Perspective of Technological Progress

61

incentive regulation adopted is price-cap regulation

which is the single incentive regulation; (4) strictly

limiting private capital to enter the telecom industry,

there is no real withdrawal mechanism; (5) lacking

endogenous technological innovation incentive.

In fact, the adjustment of market industry is not

only the only means of creating effective

competition. Government can improve and create a

favourable regulatory environment to encourage

technological innovation. Through technological

innovation, the costs of telecom services can be

decreased, and the telecom industry can be boosted

to develop in the direction of the higher level of

technologies. Based on this, from the perspective of

latest theory of government regulation, we propose

several policy suggestions to the next step of

telecommunications regulation in China:

y Set up perfect legal system of telecom industry.

During the reform of telecom industry

regulations, China has not promulgated

specialized telecom laws for so long, it is

difficult to adapt to the rapidly ever-changing

industrial environment by still using the

“Telecommunications Regulations” issued in

2000.

y Set up independent regulation institution.

Establishing independent regulation institution

is the main method of telecom regulation in

most countries. Independent regulation

institution has stronger specialized knowledge,

which can be beneficial to maintaining fair and

independent regulatory status and reducing the

transaction costs.

y Carry out the separation of network

management and service provision. The

separation of network management and service

provision is the development trend boosted by

technological innovation and economic law, it

can promote competition, avoid excessive

investment and repeated construction.

y Propel the reform on the mixed ownership of

Chinese state-owned telecom enterprises,

introduce the multiple capitals. The three

telecom operators in China at present have

gone public, but they still maintain the

dominance of state-owned shares, and still

adopt the state-owned management pattern now.

The basic telecom service industry has the

industrial characteristic of technology-driven

and innovation-driven, but the nature of state-

owned enterprise is the main reason for

restricting the technological innovation of

telecom enterprises.

ACKNOWLEDGEMENTS

This paper was supported by Major Program of the

National Social Science Foundation of China under

Grant No.15ZDB154.

REFERENCES

ASSOCIATION, C. C. 2015. 2014~2015 Analysis Report

on the Development of Chinese Communication

Industry, Posts & Telecom Press.

CRAWFORD, S. P. 2013. Captive audience: The telecom

industry and monopoly power in the new gilded age,

Yale University Press.

GAO, P. & LYYTINEN, K. 2000. Transformation of

China's telecommunications sector: a macro

perspective. Telecommunications Policy, 24, 719-730.

LI, Y. 2011. The competitive landscape of China’s

telecommunications industry: Is there a need for

further regulatory reform? Utilities Policy, 19, 125-

133.

LOO, B. P. 2004. Telecommunications reforms in China:

towards an analytical framework. Telecommunications

Policy, 28, 697-714.

ZHANG, X. 2015. The Development Report of Global

Information Society 2015. Electronic Government, 2-

19.

ISME 2016 - Information Science and Management Engineering IV

62

ISME 2016 - International Conference on Information System and Management Engineering

62