Empowering Services based Software in the Digital Single Market to

Foster an Ecosystem of Trusted, Interoperable and Legally

Compliant Cloud-Services

Juncal Alonso Ibarra, Leire Orue-Echevarria, Marisa Escalante and Gorka Benguria

Tecnalia Research and Innovation, Parque Científico y Tecnológico de Bizkaia, Edificio 700, 48160 Derio, Bizkaia, Spain

Keywords: SLA, QoS, Cloud Services, Cloud Service Broker, Digital Single Market, Services Aggregation,

Cloud Service Intermediator.

Abstract: The software industry has evolved from software on the shelf based applications deployed in dedicated

servers , to Software as a service based components running on public or private Clouds and now to Cloud

Service Brokers . So, Cloud service brokerages have emerged as digital intermediaries in the information

technology (IT) services market (Shang, 2013), creating value for cloud computing clients and vendors

alike. This paper presents an approach to foster next generation cloud service brokers through an ecosystem

of trusted, interoperable and legally compliant cloud services through an added value Cloud Services

intermediator. This ecosystem will offer, create, consume and assess trusted, interoperable, and standard

Cloud Services, where to (semi-)automatically deploy the next generation service based software

applications.

1 INTRODUCTION

The transformation from product to a service based

economy means that companies need to become

software service providers as well as consumers. In

this context, cloud enables greater business agility

by making IT infrastructure more flexible.

Cloud services have already caused a major

transformation in technologies and a paradigm shift

in business operations focus that has affected

everything from ERP to datacenter planning

(Markets 2014). Next phases in the Cloud Services

evolution include the incorporation of many

supplier/customer relationships, and their correlative

data exchange and transactions.

The software industry has evolved from software

on the shelf based applications deployed in dedicated

servers , to Software as a service based components

running on public or private Clouds and now to Cloud

Service Brokers (CSB). The fundamental CSB

functions are (Markets, 2014) to aggregate, simplify,

secure, and integrate data, communications, and

commerce between vendors. These functions are

often referred to as Cloud Intermediation services and

include both technical and business process mediation

on a cloud-to-cloud basis.

Cloud service brokerages have emerged as

digital intermediaries in the information technology

(IT) services market, creating value for cloud

computing clients and vendors alike (Shang, 2013).

According to Gartner Inc (Gartner, 2016) and

Oracle (Oracle, 2014), a cloud services brokerage

offers three capabilities:

Cloud Service Intermediation: An

intermediation broker provides value added

services on top of existing cloud platforms,

such as identity or access management

capabilities. Aggregation: An aggregation

broker provides the “glue” to bring together

multiple services and ensure the interoperability

and security of data between systems.

Cloud Service Arbitrage: A cloud service

arbitrage provides flexibility and “opportunistic

choices” by offering multiple similar services

to select from.

The next generation of Cloud Services Brokers

need to go one step beyond. Aggregation of Cloud

Services is not enough as Cloud Services users are

experiencing new challenges such as :

Vendor lock-in: once a company uses a service

offered by a cloud provider or deploys an

application on a certain cloud provider, it is

very likely that the company will be greatly

dependent on the platform or services of a

Ibarra, J., Orue-Echevarria, L., Escalante, M. and Benguria, G.

Empowering Services based Software in the Digital Single Market to Foster an Ecosystem of Trusted, Interoperable and Legally Compliant Cloud-Services.

In Proceedings of the 6th International Conference on Cloud Computing and Services Science (CLOSER 2016) - Volume 1, pages 283-288

ISBN: 978-989-758-182-3

Copyright

c

2016 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

283

cloud provider (e.g. while using their

virtualized infrastructure), making it harder to

port the application to another cloud provider or

use another service offered by another provider.

Lack of compliance of legislation: the use of

cross-border services is currently limited

because most of existing cloud services do not

comply fully with EU28 legislation and

regulations. EU harmonization of legislation in,

i.e. data protection, is a recurring barrier.

However, cloud computing will only be

uptaken when cloud services comply with or

aware of EU28 legislation.

Interoperability: data portability and seamless

use of applications that can interoperate with

each other are key challenges for cloud

consumers. Interoperability among cloud

service providers is also an unsolved challenge,

especially when using cross-border cloud

services.

SLA assessment: when aggregating cloud

services from different cloud providers, SLAs

must also be consequently aggregated.

However, currenly, SLAs, SLOs and SLA

metrics are not standardized making this SLA

composition, assessment and monitoring very

difficult. Several initiatives in this direction of

SLA metrics and SLOs have been launched

and are currently on-going.(SLALOM,2015)

(Timelex, 2015).

This paper presents an approach to foster an

ecosystem of trusted, interoperable and legally

compliant cloud services through an added value

Cloud Services intermediator. This ecosystem will

offer, create, consume and assess trusted,

interoperable, and standard Cloud Services, where to

(semi-)automatically deploy the next generation

service based software applications. The paper is

organized as follows. First, an introduction to the

cloud services ecosystems and their situation is

provided. Next the existing solutions in the area are

presented. Then the proposed solution is explained

in detail, including an overview of the approach as

well as the description of the modules composing

the solution. The paper finishes with a set of

conclusions and next steps to follow.

2 CLOUD SERVICES

ECOSYSTEMS

Working with many cloud service providers means

managing multiple relationships. Most enterprises

are already negotiating on a one-to-one-basis

multiple contracts with multiple cloud service

providers. Multiple contracts mean multiple

communication channels, payments, multiple

passwords, multiple data streams, multiple interfaces

and multiple providers to check up on. That derives

on questions about how to make those services work

together, how to interact with all of them or how to

unify all the efforts so maximum effectiveness and

efficiency can be obtained. This is when a Cloud

Service Broker (CSB) comes into play. As defined

by Plummer (Daryl, 2012) a cloud services

brokerage is a third-party software that adds value to

cloud services on behalf of cloud service consumers.

Their goal is to make the service more specific to a

company, or to integrate or aggregate added value

services, to enhance their non-functional properties

such as security, or to do anything which adds a

significant layer of value (i.e. capabilities) to the

original cloud services being offered. Consumers

can leverage solutions offered by CSBs that allow

organizations to focus on other business needs

instead. A viable CSB provider can make it less

expensive, less complex, less risky (also in legal

terms), interoperable and more effective for

companies to discover, aggregate, consume and

extend cloud services, particularly when they span

multiple, diverse cloud services providers in

different EU Member States.

Some of the key vendors currently occupying the

Cloud service brokerage market are Accenture, HP,

NEC Corporation, Jamcracker, Gravitant,

ComputeNext, Cloud Sherpas, Arrow Electronics,

and Capgemini. However, none of these are

currently compliant with EU28 legislation nor

contain certified services or foster interoperability or

avoid vendor lock-in. According to Markets and

Markets (Markets, 2014), the global Cloud Service

Brokerage Market is expected to grow from $5.24

Billion in 2015 to $19.16 Billion by 2020, at a

Compound Annual Growth Rate (CAGR) of 29.6%

from 2015 to 2020.

2.1 Current Situation and Challenges

With the evolution of cloud computing towards

XAAS (Anything as a service), today’s

organisations have on their hand a plethora of

alternatives to fulfil their information technology’s

needs. For example, while developing or migrating a

web site, an organisation can decide to build it in a

dedicated internal computer, build it as an instance

in a shared internal computer, build it in a dedicated

external computer, or even build it as an instance in

CLOSER 2016 - 6th International Conference on Cloud Computing and Services Science

284

a shared external. The decision on using one,

another, or several approaches simultaneously is

driven by certain evaluation criteria (e.g.

profitability, reliability, performance, and security,

legal or even ecological aspects).

“It is not the strongest of the species that

survives, nor the most intelligent, but the one most

responsive to change.” L.C. Megginson

This quote, often assigned to Charles Darwin,

has been frequently used in other domains,

Economics, Education, of course Information

Technologies (IT). Changes in IT-systems are

initiated starting from user requests, monitoring

activities or modernization initiatives.

As stated by several Cloud stakeholders, such as

Forbes, Cloud enables greater business agility by

making IT infrastructure more flexible. It provides

software vendors the needed means to enhance their

relationship with their customers.. Whether an

organization runs a company’s applications on data

centre hardware, or on a private or public cloud, it

still needs to align itself with the business’ needs,

rather than forcing the business to align itself with

IT’s. Complex software applications need context

aware computing resources ready to react to a

changeable environment.

Existing cloud services shall be made available

dynamically, broadly and cross border, so that

software providers can re-use and combine cloud

services, assembling a dynamic and re-configurable

network of interoperable, legal compliant, quality

assessed (against SLAs) single and composite cloud

services.

With so much activity implementing front-end

and back-end applications in public and private

clouds, complexity has grown at every level

(business, application, transaction and regulatory)

(Oracle, 2014).

Business transactions span multiple clouds and

therefore it is necessary to integrate clouds at the

transaction level.

To generate meaningful results, Oracle envisions

that enterprises need to address key challenges in the

next years (Oracle, 2014):

1. Governance: Ensuring that services deployed

in the cloud are protected is critical. Sharing can

create leaks that cannot be tolerated. Fostering

strong governance programs in place will protect

enterprises and their data.

2. Risk tolerance. Every enterprise should assess

their tolerance for pitfalls such as lost data and

application outages. As Information as a Service and

Integration as a Service evolve, enterprises will see

risks reduced.

3.Regulations. Lobbying for regulations and

standards are predicted to be a key step to ensure

cloud integration.

4. Cross border interoperability: The resulting

service intermediator shall support intelligent

discovery, context-aware service management and

fluid service integration, assuring data portability in

such a federated ecosystem, while guaranteeing

proper identity propagation with service-specific

granularity level of information.

5. Matching customer requirements with cloud

service specifications: customers in any EU country

should be provided with a guarantee of security,

legislation awareness and other non-functional

requirements when using any cross-border service

within heterogeneous environment. This implies that

the selected service offerings must match with all

functional and non-functional requirements coming

from the customers.

6. Legislation compliance, defining means of

assuring service compliance with legislation of EU

countries: a service is legislation aware when the

services are constrained by legal requirements, such

as data privacy, data protection, data security and

data location. Moreover, a big challenge in this

concern is to develop the methods and interfaces for

securing legislation compliance and easy legislation

change propagation through the cross-bordered and

composite services in a legislation heterogeneous

environment.

7. Cloud service SLA assessment and

monitoring: monitor and control the diverse

properties of utilized services, composite or stand-

alone, at real-time, while also being able to provide

all the critical information for the appropriate

reactions when necessary, especially when SLA

conditions are not fulfilled (e.g. elasticity, data

localisation).

8. Seamless change of provider: enable to

seamlessly change the service provider including all

services, dependencies and associated data to avoid

vendor lock-in and to be able to quickly react in

situations like bankruptcy of the cloud provider or

any other cases which causes outage of the service.

2.2 Existing Solutions

According to MarketsandMarkets (Markets, 2014),

the Cloud Brokerage Enablement market will grow

from $225.42 million in 2013 to $2.03 billion by

2018, at a CAGR of 55.3 percent. Cloud Brokerage

Enablers are software platforms that enable such

services. The overall, global Cloud Brokerage

market will grow from $1.57 billion in 2013 to $10.5

Empowering Services based Software in the Digital Single Market to Foster an Ecosystem of Trusted, Interoperable and Legally Compliant

Cloud-Services

285

billion by 2018. This represents a CAGR of 46.2

percent from 2013 to 2018.

Several private Cloud Service Brokers have been

active known players in this market (Gartner, 2012)

(Jamcracker, Gravitant, Computenext, HP, Dell,

Nephos Technologies, NEC, Cloud Sherpas and

Capgemini). Competition may also intensify with an

influx of new players, like CompatibleOne,

Gravitant or CloudSelect.

All of these are mostly focused on providing

service brokerage of Cloud Service Providers,

mainly VM’s and virtualized resources, but not of

other services offered (e.g. Data Processing as a

Service) or SaaS applications which are certified and

legally compliant.

Currently, according to the European

Commission and their report of the Digital Single

Market (European Commission, 2015) only 4% of

the services offered are cross-border, while 42% are

national and 54% are US-based.

The proposed solution aims to increase the

provisioning and consumption of legally compliant,

cross – border services.

3 ADDED VALUE CLOUD

SERVICE INTERMEDIATOR

3.1 Presented Approach

The proposed cloud service metaintermediator is an

intermediate layer that will ease the discovery and

adoption of Cloud services, single services

discovered from a cloud service provider or

composite ones coming from running CSB, in which

to deploy service based software and the creation of

a sustainable ecosystem of certified, accredited and

trustworthy applications. Some modules or

functionalities that will include the service

metaintermediator are: service discovery, service

composition, legislation awareness, interoperability,

identity propagation, monitoring, billing, SLA

assessment, service registry, legislation databases,

among others.

3.2 Proposed Solution

In the following section, an overview of the modules

and functionalities of the proposed solution is

presented:

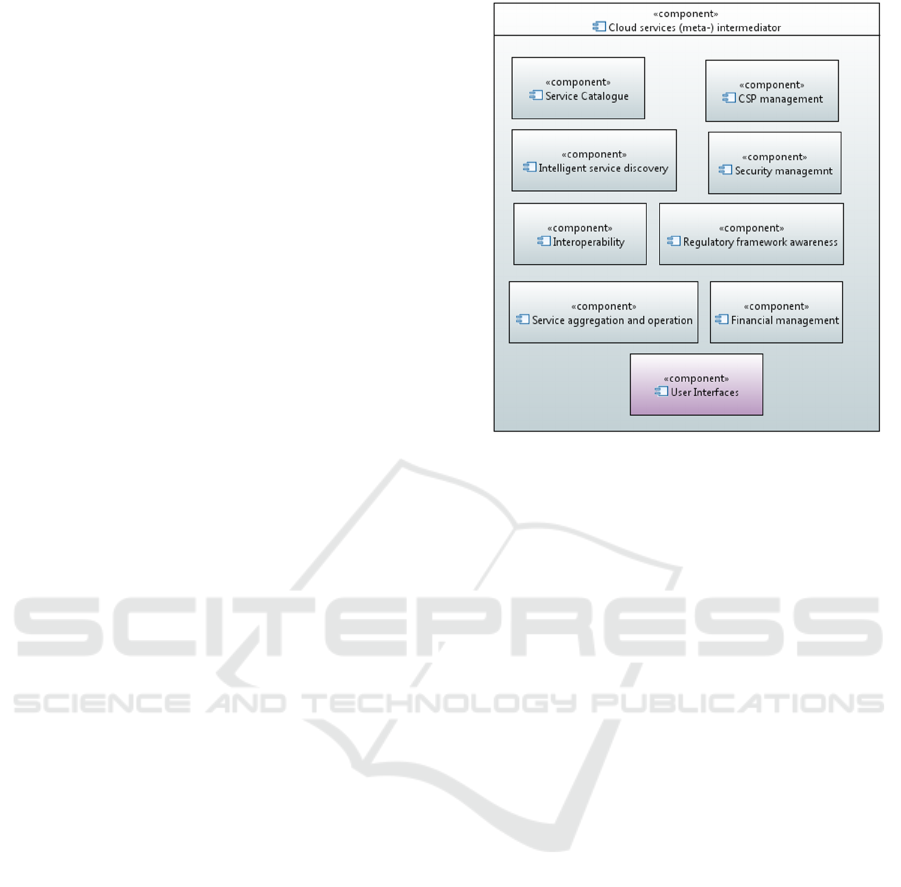

Figure 1: Cloud service (meta-) intermediator architecture

overview.

Service catalogue: This component will include

the required functional components for

cataloguing the services to be included in the in

the service intermediator:

Service registry: The service registry will

follow a declarative service configuration

template and will include information

about CSLA of the service, service life-

cycle status, service consumers or service

category among others.

Service registry governance & follow up:

These modules are in charge of governing

the service registration process, service

deletion, etc.

Intelligent service discovery: Automatic

identification of service and service

benchmarking based on the needs and

requirements with respect to different criteria

(non-functional properties, legislation

compliance, prize, etc.) stablished by the user.

Service aggregation and operation: The

framework will provide the required modules

to provide composite (aggregated) services

formed of unitary services from the same or

different Cloud Service Providers able to meet

users’ functional and non-functional

requirements.

CSP management: This module is in charge of

controlling the relationships with the Cloud

Service Provider including the management of

SLA of their provided Cloud Services. The

submodules envisioned are:

CLOSER 2016 - 6th International Conference on Cloud Computing and Services Science

286

CSLA assessment of the service in

operation, i.e., the assessment of whether

the non-functional properties are within

both the thresholds specified by the

legislation as well as the thresholds

specified in the contract. Properties such

as performance, availability and

resilience, etc. will be monitored and

assessed.

CSLA monitoring: This module also

includes the monitoring of the CSLA. The

continuous real-time monitoring of the

non-functional properties specified in the

CSLA will be done through a set of

components one for each property. These

modules are in charge of measuring the

values of the metrics of the SLOs in the

contract, be them related to QoS or

QoSec. The modules work in a non-

intrusive way in form of testing the cloud

services as an independent party.

CSLA Definition: this module is in charge

of the transformation of National CSP

offers into standard CSLAs (included

standard metrics).

Security Management module which includes

different sub-modules for assessing the secure

operation of the framework and the different

services provided. The sub-modules to be

included are:

Access and rights management: These

modules will uniquely identify and

authenticate the users ecosystem. The

module will also be in charge of the

internal identification and authentication

of the modules in operation.

Identity Management: This module is in

charge of managing the identity

propagation in the (meta) service

intermediator following a distributed

architecture approach.

Anonymization: This sub-module will be

in charge of anonymizing the data of the

service users when needed.

Regulatory framework awareness: This module

will contain European and Member states

legislations in a structured data format based in

a standardized data model. The relevant

provisions in each legislation will be linked to

non-functional service level metrics and their

acceptable thresholds, so the legislation

compliance of the services can be checked

against these predefined metrics. Once

established the service level metrics and

thresholds related to legislative provisions, this

module will evaluate even before service

operation starts if the service is compliant with

European and National regulations. These

module will include at least the following sub-

modules to perform the described legislation

awareness process:

Standards and EU and MMSS legislation

database

Regulation compliance assessment

Standards and EU and MMSS sources

management

Regulations change history

Regulations compliance monitoring

Interoperability: This module is responsible of

being the data transfer mechanism between

different cloud services. This module will

make it possible for services using non-

standard and proprietary data formats and

protocols to communicate with the bus through

specific connectors for each type of service and

as a result it will execute the migration process

necessary for seamlessly data portability. This

module will also include the connector

management for the different Cloud Service

Providers, so they can offer their services

through the intermediator.

Financial management: This module includes

the standard functions of a cloud service broker

such as accounting, metering and billing of

service instances in operation.

Service intermediator user interfaces: The

framework will include the user interfaces for

the different users. Here, we distinguish

between users that are using different services

of the intermediator, administration users and

CSPs users of the framework The different user

interfaces envisaged as user console,

administration console and CSP console will

include sub-modules such as, dashboards,

notification and alert managements, as well as

others personalized for each type of user.

4 CONCLUSIONS

As stated by the European Commission, the internet

and digital technologies are transforming our world.

But existing barriers online mean citizens miss out

on goods and services, internet companies and start-

ups have their horizons limited, and businesses and

governments cannot fully benefit from digital tools.

It is time to make the EU's single market fit for

the digital age – tearing down regulatory walls and

Empowering Services based Software in the Digital Single Market to Foster an Ecosystem of Trusted, Interoperable and Legally Compliant

Cloud-Services

287

moving from 28 national markets to a single one.

This could contribute €415 billion per year to our

economy and create hundreds of thousands of new

jobs.

Cloud Service Brokers are much like any other

type of broker in this case, acting on behalf of

customers to aggregate, integrate and customize

cloud offerings by multitudes of providers.

This paper proposes a solution to implement the

next generation of Cloud Service Brokers, providing

an intermediate layer that will ease the federation of

Cloud Service Brokers, as well as the discovery and

adoption of Cloud services on which to deploy

service based software and the creation of a

sustainable ecosystem of certified, accredited and

trustworthy applications.

Next steps include the actual implementation of

the design presented in this paper and the validation

in real life industrial and/or public administration

scenarios.

ACKNOWLEDGEMENTS

This work has been partially funded by the European

project Cloud for Europe (Seventh Framework

Programme for research,

technological development and demonstration under

grant agreement no 610650) and OPERANDO

(Horizon 2020 Programme, under grant agreement

no 653704).

REFERENCES

Slalom, 2015. http://slalom-project.eu/

Timelex, 2015. “Standards terms and performance

criteria in service level agreements for cloud

computing services” https://ec.europa.eu/digital-

agenda/en/news/study-report-standards-terms-and-

performances-criteria-service-level-agreements-cloud-

computing.

Markets, 2014. “Cloud Services Brokerage: Technology

and Market Assessment 2014 – 2019”

https://www.reportbuyer.com/product/2589608/cloud-

services-brokerage-technology-and-market-assessment

-2014-2019.html.

Oracle, 2014. “Making waves, Cloud brokerage and

integration”.

http://www.oracle.com/us/solutions/cloud/managed-cloud-

services/makingwaves-final-2162934.pdf.

Gartner, 2012. “Predicts 2013: Cloud Services

Brokerage”, Gartner Research Report, ID Number:

G00239877.

https://www.gartner.com/doc/2985118?srcId=1-28190065

90&pcp=itg.

European Commission, 2015. “A digital single market for

Europe”. http://ec.europa.eu/priorities/digital-single-

market/docs/dsm-1-year_en.pdf.

Shang, 2013. “Analyzing the impact of brokered services

on the Cloud Computing Market”,

http://docplayer.net/2008961-Analyzing-the-impact-of

-brokered-services-on-the-cloud-computing-market.ht

ml.

Gartner, 2016. http://www.gartner.com/technology/home.j

sp.

Daryl, P., 2012. “Cloud Services Brokerage: A Must-Have

for Most Organizations” http://www.forbes.com/site

s/gartnergroup/2012/03/22/cloud-services-brokerage-

a-must-have-for-most-organizations/#2715e4857a0b1

2e1dd5252aa.

CLOSER 2016 - 6th International Conference on Cloud Computing and Services Science

288