Profitability of Food & Beverages Industry Sector in IDX: The

Impact of Working Capital Turnover

Ghazali Syamni

1*

, Ichsan

1

, Rasyimah

1

, Aiyub

1

, Husaini

1

1*

Faculty of Economics and Business, Universitas Malikussaleh, Banda Aceh, Indonesia

Keywords: The

working capital, profitability, turnover, IDX

Abstract: The purpose of this study is to examine effect of working capital on profitability of food and beverage

companies in Indonesia Stock Exchange. The data used in this study is secondary data from the

documentation of financial statements of food and beverages and the like companies during the period

2012-2016. This study differs from previous research since it applies all the variables of profitability ratios

generally applied. The results of the study find that independent variables of cash turnover, receivable

turnover and inventory turnoverall have their significant effect on the profitability ratios of the company

including ratios of return on asset, return on equity, net profit margin and gross profit margin. The model

chosen in this research is Random Effect Model. Statistically this study finds that the working capital

turnover negatively affect the return on equity partially or completely. However, working capital turnover

significantly affects overall ROA, NPM and GPM. Partially, turnover circulation affects return on assets and

receivable turnover affects gross profit margin. Both turnovers affect net profit margin. Lastly, no cash

turnover affects the profitability of food companies and beverages in the Indonesia Stock Exchange.

1 INTRODUCTION

Companies are commonly established with a goal of

achieving profitability. Any company will strive to

achieve optimum level of profit and maintain the

level of profit it has achieved. One of the ways in

which managers of the company perform in order to

keep the level of profit steady is to manage the

company's working capital. Hanafi (2004) claimed

nearly 60 per cent of managers prepare time in

managing working capital in a company despite their

work in cash planning, receivable and supplies.

Thus, it was necessary for a company to plan a

rational and efficient working capital management,

not vice versa, Zeidan and Shapir (2017).

Working capital policy is an important policy

needed to be done by company managers in addition

to funding decisions, investment and dividend pay-

out (Masri and Abdulla (2017). Mun and Jang

(2015)

Mentioned that working capital as one of the factors

that influence Food Company’s value.

Several previous studies on relations of working

capital with profitability in industrial and enterprise

sectors have been conducted providing various

results. Baños-Caballero et al. (2014)study on non-

financial firms in the UK stated that the optimal

working capital level for finite-financed firms was to

have lower working capital. In Finland, Enqvist et

al. (2014)disclosed working capital management

was problematic if not efficiently done in corporate

financial planning in accordance with environmental

conditions. In Norway,Hakim and Terje (2016)

mentioned that there was a relationship between

working capital of SMEs with profitability

particularly when cash cycles were accelerated.Mun

and Jang (2015). In American restaurant companies

and Anna-Maria et al. (2016) in Helsinki disclosed

working capital related to profitability but highly

dependent on the use and various strategies in

improving the company's profitability by managers

on the company.

Various researches in Asia and Africa (Egypt,

Kenya, Nigeria and South Africa) on working

capital have also been done with different results. In

India, Bhatia and Srivastava (2016) research in 179

companies, including the Bombay 500, displayed a

negative relationship between working capital and

profitability.

Altaf and Shah (2017) proved a relationship

between working capital and profitability even

though U is inverted. Companies with limited

Syamni, G., Ichsan, ., Rasyimah, ., Aiyub, . and Husaini, .

Profitability of Food Beverages Industry Sector in IDX: The Impact of Working Capital Turnover.

DOI: 10.5220/0009899400002480

In Proceedings of the International Conference on Natural Resources and Sustainable Development (ICNRSD 2018), pages 153-157

ISBN: 978-989-758-543-2

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

153

financial capital employed lower working capital as

optimal as possible. Madhou et al. (2015)claimed

that working capital affect the profitability of the

company but highly dependent on the company's

characteristic’s, sometimes adjustment for more or

less capital needed to be made. Öztürk and Vergili

(2018) said that sales growths as well as collection

period affect return on assets while company size

has negative effect. Meanwhile, debt, cash cycle,

receivable period places no effect on profitability of

mining companies in Turkey.

Research in Pakistan by Tahir and Anuar (2016)

on textile companies found that working capital had

the most effect on the profitability of the company,

but in its implementation effectiveness was required

in order to achieve profitability. Research in Africa;

Ukaegbu (2014) showed working capital was

negatively related to profitability due to industrial

typology where cash cycle cash conversion cycle

increases hence lower the profitability. While in

Egypt, Eldomiaty et al. (2016) focusing on

nonfinancial firms explained that cash conversion as

the most important working capital variable to

improve profitability.

In Iran, Jamalinesari and Soheili (2015) claimed

that in planning an efficient working capital, the

role of good corporate governance was important in

order to achieve profitability. In Malaysia, Kasiran

et al. (2016) said that SMEs in Malaysia were still

less efficient in managing working capital.

Wasiuzzaman (2015) supported that the value of

limited capital companies would increase by

managing working capital efficiently, however, this

was not the case for larger financial capital

companies. And, Zariyawati et al. (2016) proposed a

need for corporate managers to take a smart decision

in managing the company by considering the

condition of the company. But Shaista (2015)

working capital was negative impact to profitability.

In Indonesia, Adam and Shauki (2014) research

in food and beverage companies stated that working

capital affected the value of investment. Sari (2018)

mentioned that working capital had not effectively

affected the return on investment in plantation

companies.Ramadhan et al. (2018) claimed that

working capital affected return on assets in mining

companies. While Dewi and Prasetyo (2017)

working capital inventory affected return on assets

in e textile and sharia garment companies. In the

fertilizer company by Mulyono et al. (2018) stated

that all working capital components affect the

fertilizer company's return asset. WhileWijaya and

Tjun (2018) showed not all components of working

capital, i.e., cash and inventory turnover affecting

return on assets in food and beverage companies.

The same is true for pharmaceutical companies,

Wau (2017) that cash turnover and receivable did

not affect return on assets. Inventory turnover

influenced return on assets.

Having discussed several researches, it could be

stated that inefficiency in managing working capital

affects profitability in certain industrial sectors. In

fact, there were also results of research that found no

effect of working capital variables on profitability.

Therefore, this study was conducted with the

purpose of testing the effect of working capital

turnover on the profitability of food, beverage and

other similar companies. However, this study differs

by using four dependent variables as proxy of

profitability, i.e. return on asset, and return on

equity, net profit margin and gross profit margin.

The use of the four proxies of profitability ratios was

applied as a form to complement the previous

research deficiencies which use only one or two

dependent variables as profitability variables. In

addition, variable net profit margin and gross profit

margin were included since food and beverages

companies generally prioritize sales.

2 METHOD

The data used in this study is the documentation data

from the financial statements of Food & Beverages

industry in Indonesian Stock Exchange in the period

2012-2016. In that period, there were 11 Food &

Beverages industry companies that provided data

qualified to be used in this research. From the data,

fifty five observations were made consisting of 5

years and 11 companies. Thus, the model in this

study is a panel regression model. Thus, the research

model is:

ROA

it

= β0+ β1Cash

it

+ Β2 Receivable

it

+

β3Inventory

it

+ ε

it

ROE

it

= β0+ β1Cashit + Β2 Receivable

it

+

β3Inventory

it+

εit

GPM

it

=β0+ β1Cash

it

+Β2 Receivable

it

+

β3Inventory

it

+εi

NPM

it

= β0 + β1Cash

it

+ Β2

Receivable

it

+β3Inventory

it

+εit

Where, ROA, ROE, NPM and GPM are return

on assets, return on equity, net profit margin and

gross profit margin. β is the coefficient, Cash,

Receivable and Inventory are (cash turnover,

receivable turnover, inventory turnover), i is the

company name and t is the period of time.

Furthermore, having used panel regression, this

study selected model of Common Effect Model

ICNRSD 2018 - International Conference on Natural Resources and Sustainable Development

154

(CEM), Fixed Effect Model (FEM) and Random

Effect Model (REM). The best model selection is

determined by doing Chow test, Hausman test.

Chow test is performed to select CEM with FEM.

The best model is determined by the probability

significance of chi square, if the significance value is

<0.05 then the best model is FEM, otherwise if the

significance value is> 0.05 then the best model is

CEM and no need to proceed with Hausman test.

Hausman test is performed with the aim of selecting

FEM with REM. If the value of chi square is

significant <0.05, then the best model is FEM,

otherwise if not significant 0.05 then the best model

is REM, Baltagi et al. (2003) and Zariyawati et al.

(2016).

3 RESULT

Prior to the discussion of panel regression results,

the selection of models used in this study would be

explained, CEM, FEM and REM. The testing result

of the influence of working capital turnover on

profitability in food and Beverages Company in

Indonesia Stock Exchange can be seen in Table 1a

and 1b below.

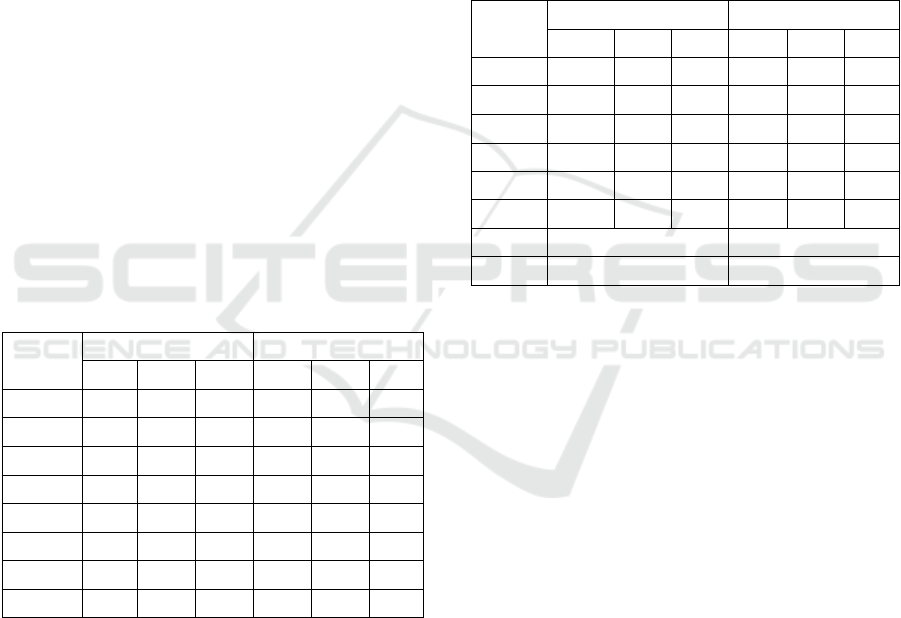

Table 1a: Influence of working capital turnover to

profitability (Cont'd)

Coefficient

NPM GPM

CEM FEM REM CEM FEM REM

C

16.347

***

10.215

***

12.387

***

40.508

***

37.492

***

37.487

***

Cash

Turnover

-0.065

***

0.195 00.31

-0.154

***

-0.023 -0.039

Receivable

Turnover

-0.623

**

-0.704

***

-0.690

***

-1.427

***

-1.155

***

-1.154

***

Inventory

Turn over

-0.018

0.5177

**

0.315

*

0.548

*

1.441 1.809

R2 1.897 5.973 1.239 2.088 6.525 1.726

F-Statistic 63.966

19.405

***

3.694

**

7.313

***

49.161

***

5.626

***

Chow test

0.000

***

0.000

***

Hausman

test

0.872

4.572

Note: *** as significant 1 %, ** as significant 5% and *

significant 10%.

As mentioned earlier in the research method,

Chow Test and Hausman Test were conducted in

choosing the research model is done whether in

equation 1.2.3 and 4. In the Chow Test stage, in all

models of panel regression, whether equations 1, 2,

3 and 4, showed that probability value significant chi

square <0.05 i.e. 0.000. It can be explained that all

models 1, 2, 3 and 4 selected the model of fixed

effect model equation. Since Chow test value is

significantly below 0.05 or 0.000, a further testing

step is necessary Hausman test. The Hausman test is

performed aiming to select fixed effect and random

effect model in each 1, 2, 3 and 4 model. Based on

Hausman test it is found that in the first model the

chi square probability value is not significant at the

5% level i. e. 0.0799. From equation models 2, 3 and

4 significance probability values were found of

0.7419, 0.1257 and 0.7419 or all at a significance

level of 10% meaning not significant 5%. Thus, the

best model of this research is random effects model

Baltagi et al. (2003).

Table 1b: Influence of working capital turnover to

profitability

Coefficient

NPM GPM

CEM FEM REM CEM FEM REM

C

16.347

***

10.215

***

12.387

***

40.508

***

37.492

***

37.487

***

Cash

Turnover

-0.065

***

0.195 0.31

-0.154

***

-0.023 -0.039

Receiveble

Turnover

-0.623

**

-0.704

***

-0.690

***

-1.427

***

-1.155

***

-1.154

***

Inventory

Turn over

-0.018

0.517

**

0.315

*

0.548

*

1.441 1.809

R

2

1.897 5.973 1.239 2.088 6.525 1.726

F_Statistic 63.966

19.405

***

3.694

**

7.313

***

49.161

***

5.626

***

Chow test 0.000*** 0.000***

Hausman

test

0.872 4.572

Note: *** as significant 1 %, ** as significant 5% and *

significant 10%.

Having selected the models, it is decided to

apply REM which result the equations as follows:

ROA= 5.676*- 0.011Cash–0.119 Receivable+ 0.612

Inventory***

ROE=11.885**-0.010Cash+0.195Receivable+ 0.223

Inventory

NPM=12.387***+0.003Cash-0.690

Receivable***+0.315Inventory*

GPM=37.487***-0.039Cash–1.154Receivable***+ 0.260

Inventory

Based on Tables 1a and 1b it can be explained,

except for ROE, other dependent variables, ROA,

NPM and GPM can be explained by other

independent variables such as cash turnover,

receivable turnover and inventory turnover which is

strikingly low. This is reflected in the value of

coefficient of determination, each at 18.44 per cent,

17,85 per cent and 24,86 per cent. However, the

ability of variable cash turnover, receivable turnover

and inventory turnover in explaining their effects on

return on equity is also at the low level i.e. 22.35 per

cent.

The results of panel regression equation in table

1a and 1b explain how the profitability of food

Profitability of Food Beverages Industry Sector in IDX: The Impact of Working Capital Turnover

155

companies and beverages in Indonesia Stock

Exchange is more determined by the turnover of

working capital, especially receivable turnover and

inventory turnover in raising profitability. It can be

concluded from variables that have significance to

return on asset is inventory turnover. The variables

affecting net profit margin are receivable turnover

and inventory turnover while gross profit margin is

more determined by receivable turnover.

The first variable affecting ROA is inventory

turnover with coefficient value of 0.6127. This

means that if the inventory turnover is accelerated

10 points it will raise the profit advantage amounted

to 6.127 points. This finding is consistent with

Mulyono et al. (2018) who stated a need to

accelerate inventory and accelerate payments. All

acceleration of working capital management should

lead to improved profitability (Tahir and Anuar,

2016). The two variables affecting NPM are the

receivable turnover and inventory turnover

respectively with coefficient values -0.6902 and

0.3156, while the variables affecting GPM are

receivable turnover with coefficient - 1.1541. This

figure can be interpreted that if the turnover of

accounts receivable is conducted by 10 points faster

than corporate profits will be decreased by 6,902

points. Meanwhile, if the company can increase its

inventory turnover by 10 points, the company's

profit will rise by 3,156 points.

The same thing happened to GPM in which if the

receivable turnover increase by 10 points then it can

lower the profit rate by 11,541 points. This finding is

consistent with that of Baños-Caballero et al. (2014)

which mentioned that it was advisable that the

company manager avoid sales loss and discounted

policies if early repayments were made to maintain

corporate performance. Enqvist et al. (2014)

explained a need for efficient inventory and

inventory management to improve the profitability

of the company. In addition, the results of this study

are in accordance with Wasiuzzaman (2015) who

claimed existence of negative effects of all

components of working capital on profitability.

Nevertheless, the above equation models explain

that among the components of working capital

turnover, only cash turnover that have no effect on

profitability in food companies and beverages in the

Indonesia Stock Exchange. According toHakim and

Terje (2016), this proved that the cash conversion

cycle was not in a good condition which causes no

impact on profitability. These findings indicate that

cash turnover is still inefficiently managed by the

management of food and beverages companies in the

Indonesia Stock Exchange. However, Eldomiaty et

al. (2016) proposed different result. The cash

turnover was claimed as most important in working

capital management in improving profitability.

Another finding in this research is that the working

capital turnover component is not related to return

on equity in food companies and beverages in

Indonesia Stock Exchange. This is clearly seen in

the results of panel regression where the two

components displayed insignificant value both

partially and simultaneously. These findings indicate

that investors are negligent on the management of

their working capital and handing over the

management of working capital entirely to the

management of the company.

4 CONCLUSIONS

The findings of this study indicate that corporate

governance mechanisms play an essential role in

improving working capital efficiency in companies

including food companies and beverages. This is in

line with what is revealed by Jamalinesari and

Soheili (2015) that good corporate governance

provides efficiency for the company which will

contribute better returns. On the contrary, the results

of this study explain that all variables of working

capital turnover both cash turnover, receivable

turnover and inventory turnover used in this study

place no significant effect on the dependent variable

return on asset.

These findings indicate that investors

acknowledge that working capital turnover is

inseparable from food and beverages industry.

Working capital turnover is performed with the aim

of avoiding occurrences of food or drink

accumulation thus resulting in profits loss. Hence,

the investors are not anticipating a profit from this

working capital turnover despite, theoretically,

working capital turns profit at other ratios. In

general, not all working capital turnover variables

affect other profitability variables whether return on

asset, net profit margin and gross profit margin.

ACKNOWLEDGEMENTS

Thanks to the post-graduate program faculty of

economics and business Malikussaleh University on

the registration fee for proceedings in ICNSRD

ICNRSD 2018 - International Conference on Natural Resources and Sustainable Development

156

REFERENCES

Adam, A.A., Shauki, E.R., 2014. Socially responsible

investment in Malaysia: behavioral framework in

evaluating investors' decision making process. Journal

of Cleaner Production 80: 224-240.

Altaf, N., Shah, F., 2017. Working capital management,

firm performance and financial constraints: Empirical

evidence from India. Asia-Pacific Journal of Business

Administration 9: 206-219.

Anna-Maria, T., Timo, K., Miia, P., Sari, M., 2016.

Defined strategies for financial working capital

management. International Journal of Managerial

Finance 12: 277-294.

Baltagi, B.H., Bresson, G., Pirotte, A., 2003. Fixed effects,

random effects or Hausman–Taylor?: A pretest

estimator. Economics letters 79: 361-369.

Baños-Caballero, S., García-Teruel, P.J., Martínez-Solano,

P. 2014. Working capital management, corporate

performance, and financial constraints. Journal of

Business Research 67: 332-338.

Bhatia, S., Srivastava, A., 2016. Working Capital

Management and Firm Performance in Emerging

Economies: Evidence from India. Management and

Labour Studies 41: 71-87.

Dewi, R. A. K., Prasetyo, A., 2017. DAR dan perputaran

persediaan serta pengaruhnya terhadap profitabilitas

perusahaan tekstil dan garmen yang terdaftar di Indeks

Saham Syariah Indonesia. Jurnal Ekonomi Syariah

Teori dan Terapan, 3, 520.

Eldomiaty, T.I., Rashwan, M.H., Bahaa el Din, M., Tayel,

W., 2016. Firm, industry and economic determinants

of working capital at risk. International Journal of

Financial Engineering 03, 1650031.

Enqvist, J., Graham, M., Nikkinen, J., 2014. The impact of

working capital management on firm profitability in

different business cycles: Evidence from Finland.

Research in International Business and Finance 32:

36-49.

Hakim, L., Terje, B., 2016. Working capital management:

evidence from Norway. International Journal of

Managerial Finance, 12: 295-313.

Hanafi, M.M., 2004. Manajemen keuangan, BPFE.

Yogyakarta.

Jamalinesari, S., Soheili, H., 2015. The Relationship

between the Efficiency of Working Capital

Management Companies and Corporate Rule in

Tehran Stock Exchange. Procedia - Social and

Behavioral Sciences 205: 499-504.

Kasiran, F.W., Mohamad, N.A., Chin, O., 2016. Working

Capital Management Efficiency: A Study on the Small

Medium Enterprise in Malaysia. Procedia Economics

and Finance, 35: 297-303.

Madhou, A., Moosa, I., Ramiah, V., 2015. Working

Capital as a Determinant of Corporate Profitability.

Review of Pacific Basin Financial Markets and

Policies 18, 1550024.

Masri, H., Abdulla, Y., 2017. A multiple objective

stochastic programming model for working capital

management. Technological Forecasting and Social

Change.

Mulyono, S., Djumahir, D., Ratnawati, K., 2018. The

effect of capital working management on the

profitability. Jurnal Keuangan dan Perbankan 22: 94-

102.

Mun, S.G., Jang, S.C., 2015. Working capital, cash

holding, and profitability of restaurant firms.

International Journal of Hospitality Management 48:

1-11.

Öztürk, M. B., Vergili, G., 2018. The Effects of Working

Capital Management on Mining Firm’s Profitability:

Empirical Evidence from an Emerging Market.

In:Kucukkocaoglu, G. & Gokten, S. (eds.) Financial

Management from an Emerging Market Perspective.

Rijeka: InTech.

Ramadhan, R.R., Hasan, A., Efni, Y., 2018. Pengaruh

working capital management terhadap profitabilitas

pada perusahaan dengan firm size, operating leverage,

dan current ratio sebagai variabel kontrol (studi pada

perusahaan sektor pertambangan di Bursa Efek

Indonesia). Jurnal Tepak Manajemen Bisnis 9: 122-

137.

Sari, R.A. 2018. Analisis manajemen modal kerja dalam

meningkatkan profitabilitas pada PT. Perkebunan

nusantara III (Persero). Jurnal Riset Akuntansi dan

Bisnis 17: 33-45.

Shaista, W., 2015. Working capital and firm value in an

emerging market. International Journal of Managerial

Finance 11: 60-79.

Tahir, M., Anuar, M.B.A., 2016. The determinants of

working capital management and firms performance of

textile sector in pakistan. Quality & Quantity 50: 605-

618.

Ukaegbu, B., 2014. The significance of working capital

management in determining firm profitability:

Evidence from developing economies in Africa.

Research in International Business and Finance 31: 1-

16.

Wasiuzzaman, S., 2015. Working Capital and Profitability

in Manufacturing Firms in Malaysia: An Empirical

Study. Global Business Review 16: 545-556.

Wau, R., 2017. Analisis efektifitas modal kerj a dan

pengaruhnya terhadap profitabilitas. Journal of

Business Studies 2: 61-74.

Wijaya, L.V., Tjun, L.T., 2018. Pengaruh cash turnover,

receivable turnover, dan inventory turnover terhadap

return on asset perusahaan sektor makanan dan

minuman yang terdaftar di Bursa Efek Indonesia

Periode 2013–20155. Jurnal Akuntansi Maranatha 9:

74-82.

Zariyawati, M., Annuar, M., Pui-San, N., 2016. Working

capital management determinants of small and large

firms in Malaysia. International Journal of Economics

& Management 10: 365-377.

Zeidan, R., Shapir, O.M., 2017. Cash conversion cycle and

value-enhancing operations: Theory and evidence for a

free lunch. Journal of Corporate Finance 45: 203-219.

Profitability of Food Beverages Industry Sector in IDX: The Impact of Working Capital Turnover

157