The Determinants of Accounting Information Systems’ Quality and

Its Implication on the Quality of Accounting Information

Lambok Vera Riama Pangaribuan

1

, Sri Hartaty

1

, Anggeraini Oktarida

1

and Eka Jumarni Fithri

1

1

Department of Accounting, State Polytechnic of Sriwijaya, Palembang, Indonesia

Keywords: Organizational culture, leadership style, internal control system, the quality of the accounting information

systems

Abstract: This research aims to analyze the impact of the organizational culture, leadership style, internal control

system on the quality of the accounting information systems and its implication on the quality of the

accounting information at BPKAD in the province of South Sumatra. The unit of analysis in this study is the

individuals or people who work in BPKAD of South Sumatra province. This research is an explanatory

research in which data are collected through a mail survey. To see the relationship between the latent

variable with a manifest variable as well as to see the relationship between exogenous with endogenous

variables, this research used a structural equation modelling by using PLS software. The result showed that

the the organizational culture, leadership style, internal control system and the quality of the accounting

information systems significantly affect the quality of the accounting information. Limitation of this study is

the small value of the loading factor of each of the variables examined. This is an opportunity for

subsequent researchers to investigate other variables that affect the quality of accounting information.

1 INTRODUCTION

All forms of business and non-profit organizations

present accounting information to help stakeholders

both within the company such as managers and from

the outside of the company such as investors,

government institutions, banks and others for the

purpose of making economic decisions (Hansen &

Mowen, 2013). Accounting information helps the

external parties of company to make investment

decisions, evaluate performance, monitor activities,

and as regulatory measures (Hansen and Mowen,

2013). By using accounting information, internal

parties of the company will obtain information

related to the past and the future, such as forecasting

which includes annual plans, strategic, and several

alternative decisions (Susanto, 2008), determination

of cost ofgoods product/cost of goods service and

etc. (Hansen & Mowen, 2013). Utilization of

accounting information as the basis for making

various types of decisions as mentioned above

because stakeholders understand well that the

essence of accounting information has met the

criteria as decision-useful-information, which means

information that is useful for decision making (Kieso

et al, 2012).

The development of regional autonomy in

Indonesia in accordance to the applicable regulations

brought changes to the system of politic, social,

community and economy which led to various

demands on good governance.

For reporting and accountability of financial

statements, standards and default accounting

systems are required to be applied consistently so

that the financial statements can be presented

completely and on time. Based on Government

Regulation Number 71 of 2010, government

accounting standards are defined as accounting

principles in the preparation and presentation of

government financial statements in the form of

Government Accounting Standards (PSAP), and are

prepared with reference to the Government

Accounting Conceptual Framework. A government

that applies good and right Government Accounting

Standards will produce qualified financial

statements.

The regional government of South Sumatra has

attempted to compile reports based on government

accounting standards and regional financial

accounting systems, so that the quality generated

from the regional financial statements can be

increased and qualified. This can be seen in the

22

Pangaribuan, L., Hartaty, S., Oktarida, A. and Fithri, E.

The Determinants of Accounting Information Systems’ Quality and Its Implication on the Quality of Accounting Information.

DOI: 10.5220/0009151900002500

In Proceedings of the 2nd Forum in Research, Science, and Technology (FIRST 2018), pages 22-29

ISBN: 978-989-758-574-6; ISSN: 2461-0739

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

Results of Examination Summary (IHPS) Iin 2016

(IHPS BPK RI for the period 2011-2015) Regional

Government Financial Statements (LKPD) of the

South Sumatra Province from 2011 to 2013

describing the results of opinions as Qualified

Opinions (WDP). Whereas in 2014 described the

results of opinion as Modify Unqualified Opinions

(WTPDPP) and in 2015 the government of South

Sumatra province received the opinion of the

Supreme Audit Institution (BPK) as Unqualified

Opinions (WTP).

The results of the evaluation by the BPK show

that the Regional Government Financial Statements

that obtain WTP opinions generally have

implemented SAP and SAKD well and properly as

well as having adequate internal controls.

Meanwhile, WDP opinions in general are due to the

existence of SAP implementation that has not been

fully implemented and LKPDs that obtain

Unqualified Opinions and Disclaimer of Opinions

(TMP) still need a lot of good improvements and

perfection in terms of the right and correct

application of government accounting standards, the

effectiveness of regional government information

reporting system optimally and improvement of

internal control in terms of the reliability of the

information presented in the financial statements.

In general, organizational culture within

government institution is still characterized by

various problems, such as: the weakness of

consistency and continuity of the state apparatus

towards the organization's vision and mission, low

integrity, loyalty and professionalism, the state

apparatus is not creative, and individualism is more

prominent than togetherness (Ministry The

Enforcement of the State Apparatus of the Republic

of Indonesia, 2012). Susanto, 2008 revealed that

related to accounting information systems,

organizational culture is related to the mental

problems of human resources (system users) in the

organization. According to (Susanto, 2008), the

presence of computer technology as part of the

accounting information system component brings

change from the previous culture to the new culture.

So that any changes in the information system as

something new and positive have forced each

member of the organization to do something

different than usual. Many people feel disappointed

because they are doing something positive, and seek

any effort to encourage the old accounting

information system to survive.

Based on the phenomenon and gap research that

has been explained, the purpose of this study is to

analyze the influence of organizational culture,

leadership style and internal control system partially

and simultaneously towards the quality of

accounting information systems in the South

Sumatra provincial government and the influence of

the quality of accounting information systems

towards the quality of accounting information in the

provincial government of South Sumatra.

2 LITERATURE REVIEW

In general organizational culture has a positive

influence on organizational effectiveness when

organizational culture can give support for

organizational goals, share widely and deeply

embedded in each member of the organization

(Bartol & Martin, 1998)

According to (Indetje & Qin, 2010),

organizational culture has a strong influence on the

application of financial information systems.

Identifying and understanding meanings, norms, and

power in an organization is an important

consideration when implementing a system. Hirsch

(1994) also stated that organizational culture has a

very strong influence on the behaviour of individuals

and organizations as a whole. The information

system is the main component of the organization,

so that the information system can be influenced

substantially by the organizational culture. Many

information systems fail, in simple term, the cause is

the information system does not match the

organizational culture in which the information

system is designed.

Just like the statements above (Claver et al,

2001) stated that in organizations that have a strong

culture, that is when beliefs have been widely shared

throughout the organization and values have been

accepted by each particular group, then the system

information will become a very important factor in

its competitiveness. Therefore, according to (Loudon

& Loudon, 2012) organizational culture is included

as one of the central organizational factors when

planning a new system.

Loudon & Loudon (2012) explained that

leadership style is one of the factors that must be

considered in planning a new (information) system.

By using one of the leadership styles as intended in

the path-goal-theory of leadership, leaders try to

influence perceptions and motivate their

subordinates (Luthan, 2008)

Transformational leaders inspire values and ideal

follower sand ultimately motivate followers to do

more than what is expected of them. By using the

analogy of the definition of transformational

The Determinants of Accounting Information Systems’ Quality and Its Implication on the Quality of Accounting Information

23

leadership, (Cho et al, 2011) tried to translate the

meaning of a positive relationship between

transformational leadership and the success of

system information.

Cho (2011), then asserted, that by carrying out

the four behaviors above can ensure that

transformational leadership will be able to play an

important role in the success of the information

system user.

The information quality of accounting

information systems is influenced by internal control

factors (Elder et al, 2010). The management reason

for designing an effective internal control system is

to achieve three general objectives, namely: (a)

reliability of financial reporting, (b) effectiveness

and efficiency of corporation’s operation, and (c)

compliance with laws and regulations (Messier et al,

2006).

Internal controls are designed to ensure the

accuracy of data entry, processing techniques,

storage methods and accuracy of results

(information). In other words, the internal control

system is designed to monitor and maintain the

quality and security of accounting information

system activities in carrying out input, process and

output activities (O Brien and Marakas, 2010). By

building internal control in a computer-based

accounting information system, it will help

management's efforts to protect company assets

from loss and embezzlement and to maintain the

accuracy of the company's financial data (Jones and

Rama, 2003: 7).

Internal control is needed to ensure that the

accounting information system works as expected so

that the risk of deviations from the pre-determined

goals may be avoided (Susanto, 2008). Companies

are required to develop internal controls with the

aim of providing reasonable certainty that the

financial report has been presented qualifiedly

(Arens et al, 2008), while according to (Mill Champ

and Taylor, 2012) accounting information systems

and score keeping systems will not successfully

carry out the processing of accounting transactions

completely and accurately unless control is carried

out which is known as internal control.

Over all, an accounting information system

carries out four main functions, which are: data

preparation, data entry, transaction processing, and

report production and distribution (appendix 9A:

2014) The accounting information system processes

financial transactions, then records the transactions

in journal books and ledgers (both based on manual

and computerized) and procedures without requiring

guarantee of accuracy. However, accounting policies

and procedures often contain basic elements of

internal control

O'Brien (2010) stated that information systems

can help managers by providing necessary

information to carry out every managerial function.

Scott (1986) also stated that the accounting

information system aims to present financial

statements designed for external users and internal

users. Similarly (Hall, 2011) stated that

fundamentally, the purposes of accounting

information systems are: (1) to provide information

about the organizational resources used, (2) to

provide information related to management decision

making, and (3) to provide information for personnel

operations to assist them in carrying out their tasks

efficiently and effectively.

In addition to the above statement (Susanto,

2009) stated that for a company, accounting

information systems are built with the main purpose

to process accounting data from various sources into

accounting information needed by various users to

reduce risk in making decisions. Romney & Paul JS

(2006) also stated that the basic function of the

accounting information system is to provide useful

information for decision making. Furthermore,

according to (Romney & Paul JS, 2006), to be useful

accounting information generated by accounting

information systems, such as financial statements

and various types of statements, must present an

accurate, complete, and timely description of

company activities.

Whereas according to (Pornpandejwittaja &

Pairat, 2012) that the effectiveness of information

systems relates to collecting, entering, processing,

storing data, managing, controlling reporting of

accounting information so that organizations can

obtain qualified financial statements.

Proof of the theoretical concepts above related to

the influence of the quality of the Accounting

Information Systemson the quality of accounting

information empirically shows the following results:

The study of (Salehi et al, 2011), about the success

of information systems in economic revival in Iran,

shows that accounting information systems can

repair the validity of the financial statements and

financial reporting

.

3 RESEARCH METHODOLOGY

This study uses a quantitative research approach.

The research method used by the author is an

explanatory research method. The selected unit of

analysis is BPKAD of South Sumatra province with

FIRST 2018 - 2nd Forum in Research, Science, and Technology (FIRST) – International Conference

24

the observation unit (respondent) are employees who

work at the BPKAD of South Sumatra province

which are related to the preparation of the financial

statements of the province of South Sumatra

Data needed from the two types of data are

collected by questionnaire technique and observation

technique. Before the questionnaire was distributed

to the respondents, several tests were carried out

first, namely validity and reliability test.

The population of this research is all employees

who work in BPKAD in South Sumatra Province

which are related to the preparation of financial

statements as many as 90 people. From those 90

employees, the questionaire that returned and can

only be processed are only 46 questionnaires, so that

the author uses saturated samples. Data processing

research is using SEM-PLS

.

4 RESULT AND DISCUSSION

4.1 Result

4.1.1 Result of the Measurement Model

(Outer Model)

The criteria used in assessing the outer 'model are

convergent validity, discriminant validity and

composite reliability. Because the model of the

Structural Equation Modelling (SEM) used is an

approach model with the Second Order, so the

Measurement Model has two stages namely

Indicators of Dimensions and Dimensions of

Variables.

The calculation result of loading factor for 4

manifest variables of the latent variable of

Organizational Culture ranged from 0.7 to 0.9 is

already above the average for loading factor of 0.5.

The results of calculating the value of the outer

model or correlation between constructs with

variables (loading factor) have fulfilled the

Convergent Validity. The loading factor value is

above the recommended value of 0.50. The t test

value shows that the indicator is significant (because

the t value is more than 1.96), so that the construct

(manifest variables) for organizational culture is not

eliminated from the model.

Leadership style consists of dimensions of

directive, supportive, participative and achievement

oriented. The calculation results of loading factor for

the 4 manifest variables of the latent variable

leadership style ranged from 0,8 to 0.9 is already

above the average for loading factor of 0.5.

Calculation of the value of the outer model or

correlation between constructs with variables

(loading factor) has fulfilled the Convergent

Validity. The loading factor value is above the

recommended value of 0.50. The t test value shows

that the indicator is significant (because the t value is

more than 1.96), so that the construct (manifest

variable) for the Leadership Style is not eliminated

from the model.

The Internal control system consists of general

control and special control dimensions. The

calculation result of loading factor for 2 manifest

variables of the internal control system latent

variable ranges from 0.8 – 0.9 is already above the

average for loading factor of 0,5. Calculation of the

value of the outer model or correlation between

constructs with variables (loading factor) has

fulfilled the convergent validity. The loading factor

value is above the recommended value of 0.50. The t

test value shows that the indicator is significant

(because the t value is more than 1.96), so that no

construct (manifest variables) for the internal control

system is eliminated from the model.

The quality of the Accounting Information

System consists of the dimensions of Ease, Usability

and the Actual Usage. The calculation results of

loading factor for the 3 manifest variables of the

latent variable the quality of the Accounting

Information System (Y) ranges from 0,8 to 0,9 is

above the average for a factor of 0,5. The results of

calculating the value of the outer model or

correlation between constructs with variables

(loading factor) have fulfilled the Convergent

Validity. The loading factor value is above the

recommended value of 0.50. The t test value shows

that the indicator is significant (because the t value is

more than 1.96), so that the construct (manifest

variable) for the quality of the Accounting

Information System is not eliminated from the

model.

The Quality of Accounting Information consists

of the dimensions of Relevance, Accuracy,

Completeness and Timeliness. The calculation

results of loading factor for 4 manifest variables of

latent variables the quality of accounting

information ranges from 0.8 – 0.9 is above the

average for loading factor of 0.5. The results of

calculating the value of the outer model or

correlation between constructs with variables

(loading factor) have fulfilled the convergent

validity. The loading factor value is above the

recommended value of 0.50. The t test value shows

that the indicator is significant (because the t value is

more than 1.96), so that the construct (manifest

The Determinants of Accounting Information Systems’ Quality and Its Implication on the Quality of Accounting Information

25

variable) for the quality of accounting information is

not eliminated from the model.

4.1.2 Testing Results of the Structural

Model (Inner Model)

PLS explained that the R

2

value is equal to 0.25

which has a weak effect, 0.5 has a moderate effect

and 0.75 has substantial effect (Chin, 2010). R

2

values indicate the accuracy of predictions from the

model (Hair, 2014). So the research model using the

accuracy of the model in predicting the Quality of

the Accounting Information System (Y1) of 0.823

has a substantial (strong) effect and the accuracy of

the model in predicting the Quality of Accounting

Information (Y2) of 0.881 has a substantial (strong)

effect.

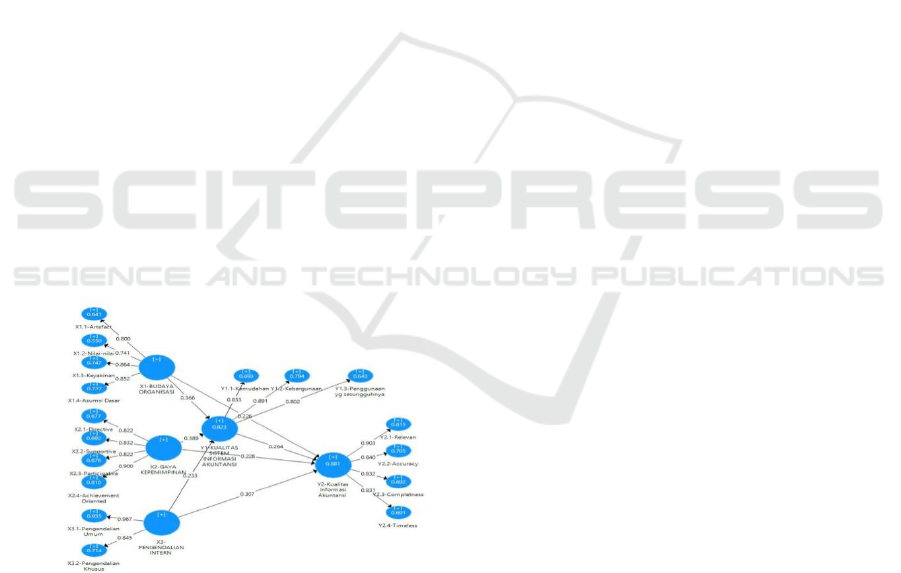

4.1.3 Full Analysis Model of SEM

Based on the research data calculated using the SEM

approach of Partial Least Square (PLS), the

structural model is shown in Figure 1.

Based on the research data and calculated using

SEM the PLS approach was obtained by the

structural equation sub-model for this study as

follows:

1

= 0.366

1

+ 0.389

2

+ 0.233

3

+ 0.177

2

= 0.226

1

+ 0.228

2

+ 0.307

3

+ 0.264

1

+ 0.119

Figure 1: Structural model

4.2 Discussion

4.2.1 The Effect of Organizational Culture

(OC) towards the Quality of

Accounting Information Systems (AIS)

The results of testing of the first hypothesis

regarding the influence of OC towards the quality of

the AIS shown in Figure 1 shows that the path

coefficient value is 0.366 with a t count of 2.141

with a significance value (p-value) of 0,038. The

value of the t-statistics obtained (2.141) is greater

than the t-critical (1.960) and when viewed from the

test significance value of 0.038 < 0.05, it is

concluded that it is significant. This result means

that OC has an effect towards the quality of the AIS

which is meaningful in accordance with the

hypotheses that are suspected. This provides

information that the increasing intensification of

organizational culture socialization to expand the

spread of OC values so that they are understood and

believed then applied by BPKAD employees in

South Sumatra province that will have a significant

influence on improving the quality of AIS.

The results are in line with the research

conducted by (Carolina and Rapina, 2015) regarding

the influence of OC, organizational structure on the

Quality of AIS and their implications for the Quality

of Accounting Information on manufacturing

companies in Bandung which show the influence of

OC towards the Quality of AIS; (Napitupulu, 2015)

with the results of OC influencing the Quality of

AIS; and (Nusa, 2015), that there is a significant

influence of OC towards the quality of AIS.

The most dominant dimension of OC variables

on the confidence dimension with indicators of

seriousness in carrying out the task in the best way

and sincerity in completing the work tasks and

objectives, while the dominant AIS quality variable

is formed by the usability dimension with indicators

of task completion speed, performance, achievement

of goals work and ease of doing work. This makes

the findings in this study that if the belief to carry

out the tasks and objectives of the job is high, then

the AIS will have a high value of use/increase.

4.2.2 The Effect of Leadership Style (LS)

towards the Quality of AIS

The results of the second hypothesis testing show

that the path coefficient value is 0.389 with a t count

of 2.751 with a significance value (p-value) of 0.09.

The value of the t-statistics obtained (2.751) is

greater than that of t-critical (1.960) and when

viewed from the test significance value of 0.009 <

0.05, a significant test is concluded. This result

means that the LS is effect towards the quality of the

AIS which means that it is in accordance with the

hypothesis that is suspected. Thus it can be

interpreted, that the increasing effectiveness of LS in

the BPKAD of South Sumatra Province will have a

significant effect on improving the quality of AIS.

FIRST 2018 - 2nd Forum in Research, Science, and Technology (FIRST) – International Conference

26

The results of this study support the theoretical

statement about the effect of LS towards the quality

of AIS (Eom, 2005), (Ghandour et al, 2007),

(Tajuddin et al, 2012), (Cho, 2011). Based on the

description above that it can be concluded that

leadership affects the success/effectiveness/quality

of AIS.

The dominant dimensions of LS variables are

oriented achievement dimensions with leader

indicators providing opportunities for subordinates,

subordinate awareness to use their best abilities

while the dominant accounting information system

quality variable is formed by usability dimensions

with indicators of task completion speed,

performance, achievement of work goals and ease of

doing work

.

4.2.3 The Effect of Internal Control System

(ICS) towards the Quality of AIS

The results of the third hypothesis testing indicate

that the path coefficient value is 0.233 with a t-count

of 2.644 with a significance value (p-value) of

0.011. The value of the t-statistics obtained (2.644)

is greater than that of t-critical (1.960) and when

viewed from the test significance value of 0.011 <

0.05, a significant test is concluded.

This result means that the ICS affects towards

the quality of the AIS, which means that it is in

accordance with the hypotheses that are suspected.

Thus, the more effective the ICS is, the quality of

the AIS Province BPKAD will have a high quality.

The dominant dimensions of ICS variables are

general control dimensions with indicators of

implementation of control organizational structure,

implementation of general operating procedures,

implementation of equipment control features and

implementation of data access control, while the

variable quality of AIS is predominantly shaped by

usability dimensions with speed indicators

performance, achievement of work goals and ease of

doing work.

4.2.4 The Effect of OC, LS and ICS

Simultaneous towards the Quality of

AIS

The results of the effect of OC, LS and ICS towards

the quality of the AIS is 82.3% and the effect of

factors outside the OC, LS and ICS is 17.7%. The

most dominant variable affects the variable quality

of the AIS is the LS variable with the most reflecting

dimensions, namely achievement oriented

dimension, while the most reflecting variable is the

quality of AIS dominantly formed by usability

dimensions.

4.2.5 The Effect of OC towards the Quality

of Accounting Information (AI)

The fifth hypotheses testing results show that the

path coefficient value is 0.226 with a t-count of

2.609 with a significance value (p-value) of 0.013.

The value of the t-statistics obtained (2.609) is

greater than that t-critical (1.960) and when viewed

from the significance value of 0.013 < 0.05, a

significant test is concluded. This result means that

OC affects the quality of AI that is meaningful in

accordance with the hypotheses that are suspected.

This provides information that the increasing

intensification of socialization of OC to expand the

spread of OC values so that they are understood and

believed then applied by BPKAD employees in

South Sumatra province that will have a significant

effect on improving the quality of AI. The most

dominant dimensions of OC variables in the

dimension of belief, while the quality variables of AI

in the relevant dimensions.

4.2.6 The Effect of LS towards the Quality

of AI

The results of the first hypothesis testing show that

the path coefficient value is 0.228 with a t-count of

2.802 with a significance value (p-value) of 0.008.

The value of the t-statistics obtained (2.802) is

greater than that t-critical (1.960) and when viewed

from the significance value of the test 0.008 < 0.05,

a significant test is concluded. This result means that

the LS affect the quality of AI that is meaningful in

accordance with the hypothesis that is suspected.

Thus it can be interpreted, that the increasing

effectiveness of LS in the BPKAD of South Sumatra

Province will have a significant effect on improving

the quality of AI. The dominant dimension of LS

variables is achievement-oriented, while the quality

of AI quality is relevant.

4.2.7 The Effect of ICS towards the Quality

of AI

The seventh hypothesis testing result show that the

path coefficient value is 0.307 with a t-count of

3.362 with a significance value (p-value) of 0.002.

The value of the t-statistics obtained (3.362) is

greater than that t-critical (1.960) and when viewed

from the test significance value of 0.002 < 0.05, a

significant test is concluded. This result means that

the ICS affects the quality of AI that is meaningful

The Determinants of Accounting Information Systems’ Quality and Its Implication on the Quality of Accounting Information

27

in accordance with the hypotheses that are

suspected. The dominant dimension of ICS variables

is the general control dimension, while the dominant

AI quality variable is formed by the relevant

dimensions.

4.2.8 Effect of AIS Quality on AI Quality

The testing results of the eighth hypothesis indicate

that the path coefficient value is 0.264 with a t-count

of 2.177 with a significance value (p-value) of

0,035. The value of the t-statistics obtained (2.177)

is greater than that t-critical (1.960) and when

viewed from the significance value of 0.035 < 0.05,

a significant test is concluded.

These results mean that the quality of the AI

system affects the quality of AI that is meaningful in

accordance with the hypotheses that are suspected.

To improve the quality of AI in the BPKAD of

South Sumatra province, it requires an improvement

in the quality of the AIS, because with the increasing

quality of the AIS, the quality of AIS significantly.

4.2.9 The Effect of OC, LS, ICS and Quality

of AIS Simultaneously towards the

Quality of AI

The results of effect of OC, LS, ICS and quality of

AIS towards the quality of AI obtained by 88.1%

and the effect of factors outside OC, LS, ICS and

AIS quality of 11.9%.

5 CONCLUSIONS

OC has proven to have a positive and significant

effect on the quality of the AIS. The most dominant

dimension of OC variable in the dimension of belief,

while the variable quality of AI systems is

predominantly shaped by the dimensions of

usefulness.

The LS has proven to have a positive and

significant effect on the quality of the AIS. The

dominant dimension of LS variables is the

achievement-oriented dimension, while the variable

quality of the AIS is predominantly shaped by the

usability dimension.

The ICS has proven to have a positive and

significant effect on the quality of the AIS. The

dominant dimension of ICS variable is the general

control dimension, while the AIS quality variable is

predominantly shaped by the usability dimension.

OC, LS and ICS are simultaneously proven to

have a positive and significant effect on the quality

of the AIS with a contribution of 82.3%. The most

dominant variable influencing the variable quality of

the AIS is the LS variable with the most reflecting

dimensions, namely achievement oriented

dimension, while the most reflecting variable is the

quality of AIS quality dominantly formed by

usability dimensions.

OC has a positive and significant effect on the

quality of AI. The most dominant dimensions of OC

variables in the dimension of belief, while the

quality variables of AI in the relevant dimensions.

The LS has proven to have a positive and significant

influence on the quality of AI. The dominant

dimension of LS variables is achievement-oriented,

while the quality of AI quality is relevant. The ICS

has proven to have a positive and significant effect

on the quality of the AIS. The dominant dimension

of ICS variables is the general control dimension,

while the dominant AI quality variable is formed by

the relevant dimensions.

The quality of AIS has proven to have a positive

and significant effect on the quality of AI. The

variable quality of the AIS is formed by the usability

dimension, while the AI quality variable is on the

dimensions of revelation.

OC, LS, ICS and the quality of AIS are jointly

proven to have a positive and significant effect on

the quality of AI with a contribution of 88,1%. The

most dominant variables affecting the quality of AI

variables are internal control system variables, with

the most reflecting dimensions, namely dimensions:

general control, while the dimensions that most

reflect the quality variables of AI, are the relevant

dimensions.

ACKNOWLEDGEMENTS

This research is based on work supported by State

Polytechnic of Sriwijaya, Indonesia. The author

thankfully acknowledges scientific discussion with

our colleagues from State Polytechnic of Sriwijaya,

Indonesia.

REFERENCES

Arens, Alvin A, Randal J. Elder, Mark S Beasley. 2012.

Auditing and Assurance Service. 14 th edition. Pearson

Bartol, K. M., & Martin, D. C. 1998. Management.

Mcgraw-Hill College.

Carolina, Yenni Carolina dan Rapina. 2015. Pengaruh

Budaya Organisasi dan Struktur Organisasi terhadap

Kualitas Sistem Informasi Akuntansi serta

FIRST 2018 - 2nd Forum in Research, Science, and Technology (FIRST) – International Conference

28

Implikasinya pada Kualitas Informasi Akuntansi.

Fakultas Ekonomi Universitas Kristen Maranatha

Bandung.

Claver, Enrique et al. 2001. Information Technology and

People. 14 (3). 247-260

Cho, Jeewonet al. 2011. How Leadership Affect

Information Systems Success? The Role of

Transformational Leadership. Information &

Management. 48 (7). 270-277

Elder, Randal J., Mark S. Beasley, & Alvin A. Arens.

2010. Auditing and Assurance Sevices An Integrated

Approach. NJ: Prentice-Hall

Ghandour, Ahmad, George Benwell, & Kenneth R Deans.

2007. The Impact of Leadership on Commerce System

Success in Small and Medium Enterprise Context.

New Zeland: Small Enterprise Conference.

Hall, James A. 2011. Accounting Information System.7

th

Edition: South-Western Publishing Co

Hansen, Don R. & Maryanne M. Mowen. 2103. Cost

Management Accounting and Control. South Western

College Publishing.

Hirsch, Jr. Maurice L. 1994. Advanced Management

Accounting, 2

nd

: South Western Publishing Co.

Indeje W. G., Zheng Q. 2010. Organizational Culture and

Information Systems Implementation: A Structuration

Theory Perspective. Sprouts: Working Papers on

Information Systems, 10 (27).

http://sprouts.aisnet.org/10-27

Jones, FL & Dasaratha V. Rama. 2003. Accounting

Information Systems: A Business Process Approach,

Thompson South Western.

Kieso, D. E., Weygandt, J. J., & Warfield, T. D. 2011.

Intermediate Accounting. IFRS Edition, John Wiley &

Sons.

Loudon, Kenneth C. & Jane P. Laudon. 2012. Manajemen

Information System: Managing The Digital Firm.12

Th

Edition. NJ: Prentice-Hall.

Luthans, F. 2008. Organizational Behavior, 11

th

Edition.

Mc Graw-Hill

International Edition.

Messier, Glover & Prawitt. 2006. Auditing and Assurance

Services: A Systematic Approach. 4th Edition. NY:

McGraw-Hill.

Millichamp, Alan& Taylor John, 2012. Auditing. Tenth

edition

Napitupulu, Ilham Hidayah. 2015. Pengaruh Budaya

Organisasi, Efektivitas Pengendalian Internal dan

Kompetensi Pengguna Sistem Informasi terhadap

Kualitas sistem informasi akuntansi manajemen serta

dampaknya pada kepuasan pengguna sistem informasi.

Disertasi Program Doktor Ilmu Akuntansi Fakultas

Ekonomi dan Bisnis Universitas Padjadjaran

(unpublish).

O’Brien, James A.& George M. Marakas. 2010.

Management information systems: managing

information technology in the business enterprise.

15th Edition. NY: McGraw-Hill.

Pornpan Dejwittaya & Pairat. 2012. Effectiveness of AIS:

Effect on Performance of Thai-Listed Firms In

Thailand, International Journal of Business Research,

July, 2012. 12 (3).

Romney. Marshal B. & Paul John Steinbart. 2009.

Accounting Information Systems. Eleventh Edition:

New Jersey: Pearson-Prentice-Hall

Salehi, M. & Abdipour A. 2011. A study of the barriers of

implementation of accounting information system:

Case of listed companies in Tehran Stock Exchange.

Journal of Economics and Behavioral Studies. 2 (2).

76-85.

Scott, George M. 1986. Principles of Management

Information Systems. NY: Mc-Graw-Hill.

Susanto, Azhar. 2009. Sistem Informasi Manajemen:

Pendekatan Terstruktur Resiko Pengembangan. Edisi

Perdana: Lingga Jaya

The Determinants of Accounting Information Systems’ Quality and Its Implication on the Quality of Accounting Information

29