Pitfalls When Solving Eigenproblems

With Applications in Control Engineering

Vasile Sima

1

and Peter Benner

2

1

National Institute for Research & Development in Informatics, Bd. Mares¸al Averescu, Nr. 8–10, Bucharest, Romania

2

Max Planck Institute for Dynamics of Complex Technical Systems, Sandtorstraße 1, 39106, Magdeburg, Germany

Keywords:

Deflating Subspaces, Eigenvalue Reordering, Generalized Eigenvalues, Generalized Schur Form, Numerical

Methods, Skew-Hamiltonian/Hamiltonian Matrix Pencil, Software, Structure-preservation.

Abstract:

There is a continuous research effort worldwide to improve the reliability, efficiency, and accuracy of numeri-

cal computations in various domains. One of the most promising research avenues is to exploit the structural

properties of the mathematical problems to be solved. This paper investigates some numerical algorithms for

the solution of common and structured eigenproblems, which have many applications in automatic control

(e.g., linear-quadratic optimization and H

∞

-optimization), but also in various areas of applied mathematics,

physics, and computational chemistry. Of much interest is to find the eigenvalues and certain deflating sub-

spaces, mainly those associated to the stable eigenvalues. Several simple examples are used to highlight the

pitfalls which may appear in such numerical computations, using state-of-the-art solvers. Balancing the ma-

trices and the use of condition numbers for eigenvalues are shown to be essential options in investigating the

behavior of the solvers and problem sensitivity.

1 INTRODUCTION

Many control system analysis and design numeri-

cal techniques and procedures require the compu-

tation of eigenvalues and bases of certain invari-

ant or deflating subspaces. Often, the correspond-

ing eigenproblems have special structure, which im-

plies structural properties of their spectra. Com-

mon structures are Hamiltonian and symplectic ma-

trices or matrix pencils. One relevant computational

problem in control theory and its applications is the

evaluation of the H

∞

- and L

∞

-norms of linear dy-

namic systems, which are used, e.g., to quantify the

trade-off between performance and robust stability.

State-of-the-art quadratically convergent algorithms

for the calculation of these norms use the purely

imaginary eigenvalues of a matrix or matrix pencil

at each iteration. This matrix (pencil) is Hamilto-

nian or symplectic, in the continuous- and discrete-

time case, respectively. (Actually, the pencils arising

in the continuous-time descriptor case can be put in

a skew-Hamiltonian/Hamiltonian form (Benner et al.,

2012a).) Another fundamental computation in con-

trol systems analysis and design is the solution of

continuous-time and discrete-time algebraic Riccati

equations (CAREs and DAREs). CAREs and DAREs

arise in many applications, such as factorization tech-

niques for transfer functions matrices, model reduc-

tion procedures based on stochastic bounded- or pos-

itive real balancing, stabilization and linear-quadratic

regulator problems, Kalman filtering, linear-quadratic

Gaussian (H

2

-)optimal control problems, computa-

tion of (sub)optimal H

∞

controllers, etc. Usually, the

stabilizing solution is required, which can be used

to stabilize the closed-loop system matrix or matrix

pencil. State-of-the-art CARE/DARE solvers (Laub,

1979; Mehrmann, 1991; Sima, 1996; Benner, 1999;

MathWorks, 2014) rely on computing stable invariant

or deflating subspaces of some Hamiltonian or sym-

plectic matrices or pencils. Finding such subspaces

involves eigenvalue reordering.

Recently, structure-exploiting techniques have

been investigated for solving (skew-)Hamiltonian and

skew-Hamiltonian/Hamiltonian eigenproblems, see,

e.g., (Benner et al., 2002; Benner and Kressner, 2006;

Benner et al., 2007), and the references therein. These

algorithms are more involved than those used in the

non-structured case. The initial reduction step is more

complicated, since the structure should be exploited.

Moreover, the standard QR or QZ algorithm (Golub

and Van Loan, 1996) for matrices or pencils is re-

placed by the periodic QR/QZ algorithm, see (Bo-

171

Sima V. and Benner P..

Pitfalls When Solving Eigenproblems - With Applications in Control Engineering.

DOI: 10.5220/0005533301710178

In Proceedings of the 12th International Conference on Informatics in Control, Automation and Robotics (ICINCO-2015), pages 171-178

ISBN: 978-989-758-122-9

Copyright

c

2015 SCITEPRESS (Science and Technology Publications, Lda.)

janczyk et al., 1992; Granat et al., 2007) and the refer-

ences inside. The periodic QR/QZ algorithm operates

on formal matrix products Π

p

i=1

A

s

i

i

, where s

i

= 1 or

s

i

= −1, with possibly singular factors in the pencil

case. The number of factors p to process (the “pe-

riod”) is two, four or six (Benner et al., 2002; Ben-

ner and Kressner, 2006; Benner et al., 2007). Eigen-

value reordering is also performed on these formal

matrix products. The main difference to the standard

reordering procedures implemented in the LAPACK

package (Anderson et al., 1999) is in the algorithm for

swapping two adjacent sequences of diagonal blocks,

involving the solution of periodic Sylvester-like equa-

tions. Details are given, e.g., in (Granat et al., 2007;

Sima, 2010) and the references therein.

Advanced structure-exploiting solvers have

been incorporated in the SLICOT Library

(www.slicot.org), see (Benner et al., 1999; Van Huf-

fel et al., 2004; Benner et al., 2010; Sima et al.,

2012; Benner et al., 2013a; Benner et al., 2013b).

Fortran and MATLAB software for eigenvalues and

invariant or deflating subspaces has been developed,

for both real and complex matrices. Versions with a

factored or not factored skew-Hamiltonian matrix S

in a pencil are covered. Some performance results

for computing the eigenvalues or eigenvalues and

stable deflating subspaces for real or complex matrix

pencils, with factored or not factored matrix S are

given in (Sima, 2011a; Sima, 2011b; Sima et al.,

2012; Benner et al., 2012b; Benner et al., 2013b).

The results have shown that these solvers provide

reliable and accurate solutions, and are often faster

than the state-of-the-art tools.

This paper addresses the numerical difficulties in

computations with structured solvers, mainly for the

periodic QR/QZ steps involved, e.g., difficulties as-

sociated to multiple or close eigenvalues. Small ex-

amples, including standard eigenproblems and stan-

dard products of 2-by-2 matrices, illustrating the nu-

merical behavior, are analyzed based on experimen-

tal evidence. Our examples show the need to use

specialized measures, such as (reciprocal) condition

numbers, and special techniques, like balancing, even

when solving or analyzing small eigenproblems.

2 ACCURACY OF COMPUTED

EIGENVALUES

Several kinds of n ×n matrix pencils A −λB are con-

sidered in this paper. The eigenvalues of A − λB

are the complex numbers λ

i

, i = 1 : n (multiplici-

ties counted), satisfying the relations Ax

i

= λBx

i

, with

x

i

6= 0, i = 1 : n. The vector x

i

is a right eigenvector

corresponding to the eigenvalue λ

i

; a vector y

i

6= 0 sat-

isfying y

H

i

A = λ

i

y

H

i

B is a left eigenvector correspond-

ing to λ

i

, where y

H

i

is the conjugate-transpose of y

i

.

Finding the eigenvalues and eigenvectors of A −λB

is the generalized eigenvalue problem. A standard

eigenvalue problem is obtained for B = I

n

, the iden-

tity matrix of order n. Simple eigenvalues (i.e., with

multiplicity 1) can be computed accurately, if well-

conditioned. Multiple eigenvalues are inherently ill-

conditioned, and so they cannot generally be found

with high accuracy, even for standard small order

eigenproblems. Briefly speaking, an eigenvalue λ

i

is

well-conditioned if small perturbations in the matrix

A or matrix pair (A, B) produce small changes in the

corresponding computed eigenvalue,

b

λ

i

. Eigenvalue

condition numbers are used to assess the condition-

ing, or, equivalently, the sensitivity to perturbations

in the data. Since condition numbers can be infinite,

their reciprocals are used in practical calculations.

LAPACK driver routines compute estimates of the

reciprocal condition numbers for individual or clus-

ters of eigenvalues and eigenvectors. We will denote

these estimates by rcond(λ

i

) and rcond(x

i

), respec-

tively. A balancing option allows to perform initial

row and column permutations (to isolate the eigen-

values available by inspection in the leading/trailing

parts of A and B), scale the matrices to make the 1-

norms of rows and corresponding columns as close as

possible, or to both permute and scale. Balancing of-

ten increases the accuracy of computed eigenvalues.

An approximate error bound on the chordal distance

between the computed generalized eigenvalue

b

λ

i

and

the corresponding exact eigenvalue λ

i

is

χ(

b

λ

i

,λ

i

) ≤ ε

M

k[kAk, kBk]k/rcond(λ

i

),

where ε

M

is the relative machine accuracy, and the

norms are for the matrices after balancing, if applied.

(The 1-norm is used in LAPACK routines for A and

B, but 2-norm for the vector of norms in square brack-

ets.) This means that perturbations in the elements of

A and B can be amplified by 1/rcond(λ

i

) in the com-

puted eigenvalue

b

λ

i

. The chordal distance between

two points (

b

α,

b

β) and (α,β) is defined by

χ([

b

α,

b

β],[α, β]) =

|

b

αβ −α

b

β|

q

|

b

α|

2

+ |

b

β|

2

p

|α|

2

+ |β|

2

.

An approximate error bound for the acute angle be-

tween the computed left or right eigenvectors

b

y

i

or

b

x

i

, and the true eigenvectors y

i

or x

i

, respectively, is

given by ε

M

k[ kAk, kBk] k/rcond(x

i

). See (Anderson

et al., 1999) for further details, where tighter bounds

are also given. A very simple example illustrates what

can be expected in eigenvalue computations using nu-

merical algorithms.

ICINCO2015-12thInternationalConferenceonInformaticsinControl,AutomationandRobotics

172

Example 1. Consider a stable linear system with

transfer-function

H(s) =

1

(s + 1)

2

(s + 2)

,

hence with a double pole at −1, and another pole at

−2. A state-space matrix for this system is

A =

−4 −5 −2

1 0 0

0 1 0

.

Indeed, this is the companion matrix of the polyno-

mial z

3

+4z

2

+5z +2, which has exact roots −1, with

multiplicity 2, and −2. The eigenvalues of A should

coincide with the system poles. However, the eigen-

values corresponding to the double pole cannot gen-

erally be computed accurately. Indeed, the MATLAB

R2014b (MathWorks, 2014) function eig, based on

the state-of-the-art LAPACK routines, returns in dou-

ble precision arithmetic

−2

−0.9999999999999997 ±2.83263461777919·10

−8

ı

.

when using the command eig(A). The pole at −2 is

computed to full accuracy, but the double pole at −1

became a pair of complex conjugate values. The (ab-

solute and relative) errors of the eigenvalues of this

pair are about 2.83·10

−8

, slightly smaller than 2

√

ε

M

,

i.e., twice the square root of the relative machine ac-

curacy, hence more than half of the accuracy, has been

lost. Calling the function eig with no optional argu-

ment, as above, computes the eigenvalues after a pre-

liminary scaling of matrix A with a diagonal matrix D,

i.e., the iterative QR algorithm is applied to the ma-

trix D

−1

AD, with D = diag(2,1, 1) for this example.

Optionally, the LAPACK driver DGEESX also returns

the reciprocal condition numbers for eigenvalues and

eigenvectors, which in this case are

rcond(λ

1:3

) = [0.11111, 9.1602·10

−9

,9.1602·10

−9

],

rcond(x

1:3

) = [0.26087, 1.0950·10

−8

,1.0950·10

−8

],

respectively (rounded to 5 significant digits). The

transformed matrix A returned by DGEESX is block di-

agonal with diagonal blocks of order 1 and 2, and the

second block is

−0.9999999999999997 −2.833333333333334

2.831936074532138·10

−16

−0.9999999999999997

.

The small, but nonzero value of the subdiagonal ele-

ment is responsible for getting a pair of complex con-

jugate eigenvalues. Without balancing (e.g., using the

command eig(A,’nobalance’)), the last two eigen-

values are even less accurate,

−0.9999999999999986 ±3.817602171155931·10

−8

ı,

with errors of about 3.82·10

−8

, and the nonzero subdi-

agonal entry of the transformed matrix A is −4.7705·

10

−16

. The reciprocal condition numbers for eigen-

values and eigenvectors are

rcond(λ

1:3

) = [8.9087·10

−2

,1.1781·10

−8

,1.1781·10

−8

],

rcond(x

1:3

) = [0.24661,1.3038·10

−8

,1.3038·10

−8

].

Consider now a perturbation in the system poles.

Specifically, replacing the double pole by −1 −ε and

−1 + ε, the characteristic polynomial becomes

z

3

+ (4 +ε)z

2

+ (5 +2ε −ε

2

)z + 2 + ε −2ε

2

−ε

3

,

and the eigenvalues of the associated companion ma-

trix have been computed for values of ε set to

√

ε

M

,

10

√

ε

M

, and ε

1/4

M

. Three real eigenvalues have been

obtained for all tried parameter values, but just one

real eigenvalue for ε =

√

ε

M

when balancing was

used. The first eigenvalue was always accurately

computed, with errors of about 5.33·10

−15

or less,

with or without balancing. On the other hand, the

other two eigenvalues had errors of about 3.87·10

−8

or smaller. Specifically, for ε = 10ε

M

the errors were

about 5.45·10

−10

without balancing, and for ε =

√

ε

M

,

the errors were 6.75·10

−13

and 5.14·10

−12

, with and

without balancing, respectively. The reciprocal condi-

tion numbers have been comparable with their values

in the unperturbed case for ε set to

√

ε

M

or 10

√

ε

M

,

but increased to over 3.7·10

−5

for λ

2:3

and ε

1/4

M

. Note

that the error bounds given by the formulas above are

quite tight for all the investigated cases. The better ac-

curacy for the computed eigenvalues

b

λ

2:3

correspond-

ing to −1 −ε and −1 + ε when ε = ε

1/4

M

is due to the

bigger gap, 2ε

1/4

M

, between the true eigenvalues than

in the other cases. When this gap is zero, about half of

the accuracy is lost for this example. For a third order

system with a triple pole, about two thirds of accu-

racy (about 12 significant digits in double precision

computations) might be lost for each

b

λ

i

.

3 ACCURACY OF EIGENVALUES

FOR MATRIX PRODUCTS

Numerical difficulties appear also when computing

the periodic Schur decomposition of a matrix prod-

uct, Π

p

i=1

A

i

. This may happen even for 2 ×2 matrices

and p = 2. Such a decomposition is used, e.g., for

computing the eigenvalues and invariant subspaces of

Hamiltonian matrices (Benner and Kressner, 2006).

When A

i

are general matrices, the algorithm first re-

duces the matrix sequence to the periodic Hessenberg

PitfallsWhenSolvingEigenproblems-WithApplicationsinControlEngineering

173

form, using unitary transformations so that the eigen-

values of the product are preserved. In this form,

one matrix, usually the first one, is upper Hessen-

berg (i.e., all elements below the first subdiagonal are

zero), and all other factors are upper triangular. Then,

the sequence is further transformed similarly to one

in which the Hessenberg matrix is reduced to Schur

form, while the other matrices remain upper triangu-

lar. For complex matrices, the Schur form is also up-

per triangular, while in the real case, it is block up-

per triangular with diagonal blocks of order 1 or 2,

corresponding to real or complex conjugate eigenval-

ues, respectively. The real case only will be consid-

ered in the sequel, for convenience. As suggested by

the above presentation, the matrix product itself is not

evaluated, since forming it may yield large errors, de-

pending on its conditioning. However, the algorithm

computes some products of elements on the diagonals

(and uses sums with other products involving subdi-

agonal or superdiagonal elements), after the prelimi-

nary reduction to the Hessenberg-triangular form. If

some factors are ill-conditioned, it is possible that in-

accuracies in the intermediate results be strongly am-

plified in the computed decomposition. Nevertheless,

the returned eigenvalues are usually highly accurate.

The periodic Schur algorithm finds orthogonal

transformation matrices, Z

i

, i = 1 : p, such that the

transformed matrices,

e

A

i

= Z

T

i

A

i

Z

mod (i,p)+1

, i = 1 : p, (1)

have the required structure, i.e.,

e

A

1

is in upper real

Schur form, and

e

A

j

, j = 2 : p, are upper triangu-

lar. The eigenvalues are then readily obtained. Note

that (1) performs a similarity transformation, since

Π

p

i=1

e

A

i

= Z

T

1

(Π

p

i=1

A

i

)Z

1

, hence the eigenvalues are

theoretically preserved. The algorithm delivers the

eigenvalues and the matrices Z

i

and

e

A

i

, i = 1 : p.

Simple and well separated eigenvalues are accurately

computed; moreover, the formulas (1) are satisfied

with (high) precision for i > 1, but sometimes this is

not the case for i = 1, i.e., the obtained Schur form

may not be close to the true real Schur form. Also,

the eigenvalues of the matrix product Π

p

i=1

e

A

i

may dif-

fer from the computed eigenvalues, as shown by nu-

merical experiments. In some applications it is im-

portant to have accurate matrices

e

A

i

, i = 1 : p. Let

R

i

= Z

T

i

A

i

Z

mod (i,p)+1

−

e

A

i

, i = 1 : p, be the residuals

of the computed transformed matrices. Large norms

of some of these residuals indicate an inaccurate pe-

riodic Schur decomposition. The accuracy can be in-

creased by an iterative refinement process. Specif-

ically, another algorithm iteration (called sweep be-

low) is applied to the sequence

e

A

i

+ R

i

, i = 1 : p, and

the process continues similarly till the residual norms

Table 1: Absolute difference between the returned (2,1) el-

ement of

e

A

1

and its value computed using (1) for various

number of factors, p.

p (2,1)-element error p (2,1)-element error

10 7.78·10

−11

26 3.65·10

−2

11 7.43·10

−10

28 0.7068

16 8.66·10

−7

29 0.7743

19 1.52·10

−4

30 0.7163

22 1.85·10

−3

31 0.7205

25 4.98·10

−2

32 0.5688

are smaller than a given tolerance, or a specified num-

ber of iterations is exhausted. Often, one additional

sweep ensures acceptable accuracy, and sometimes it

is enough to update the matrix

e

A

1

only. If the transfor-

mations used in the additional sweep(s) are denoted

by Y

i

, then Z

i

Y

i

, i = 1 : p, usually transform the orig-

inal problem to one having the right structure and ac-

curate eigenvalues.

In a series of tests, the periodic Schur solver im-

plementation in the SLICOT Library has been applied

to several products of 2 ×2 real matrices. All values

of p from 2 to 32 have been tried. Since the inves-

tigated examples had real eigenvalues only, all fac-

tors

e

A

i

, i ≥ 1, are upper triangular. The computed

eigenvalues have been compared to those obtained

using the MATLAB functions eig and its symbolic

counterpart, symbolic/eig, applied to the product

of factors, Π

p

i=1

A

i

, the symbolic product of symbolic

factors, Π

p

i=1

A

i

, the product of transformed factors,

Π

p

i=1

e

A

i

, and the symbolic product of symbolic trans-

formed factors, Π

p

i=1

e

A

i

. The eigenvalues of all these

products agreed well. The difference between the

computed periodic matrix and the transformed orig-

inal periodic matrix, obtained using (1), has also been

computed. For several values of p, the (2,1) element

of the factor

e

A

1

from (1) differed significantly from its

zero value returned by the solver. All other elements

for all factors agreed very well to the returned values.

Table 1 gives the absolute value of the difference for

various p and one series of factor matrices.

The reciprocal condition numbers of the eigenval-

ues and eigenvectors of the matrix product have also

been computed, and their values have usually been

quite close to 1, agreeing with the eigenvalues’ good

observed accuracy. However, the conditioning for the

product of the transformed factors has been several

orders of magnitude worse. The computed eigen-

values most often correspond accurately to those of

Π

p

i=1

A

i

, but not to those of Π

p

i=1

e

A

i

. Using one ad-

ditional sweep, after updating the factor

e

A

1

only, the

absolute difference was of the order 10

−15

or less, for

the values p in Table 1. Moreover, the eigenvalues

ICINCO2015-12thInternationalConferenceonInformaticsinControl,AutomationandRobotics

174

have usually been more accurate.

The results for several other series of tests with

some mildly ill-conditioned factors have been similar,

but with different values of p and of the absolute dif-

ference. Actually, the numerical difficulties described

above can be encountered even for a product of two

2 ×2 matrices, as illustrated by the example below.

Example 2. Let

A

1

=

1.237 2.058

2.058 3.425

, A

2

=

16.825 13.890

13.890 11.467

,

be exact representations of the two matrices. Note

that the condition numbers for A

1

, A

2

, and A

1

A

2

are

about 1.5967·10

4

, 4.5739·10

6

, and 6.4931·10

10

, re-

spectively. There is an absolute error (in the (2,1)

element only) of order 10

−14

between the product

A

1

A

2

computed in double precision arithmetic and

that computed using symbolic calculations, via the

MATLAB command double(sym(A

1)*sym(A 2)).

The eigenvalues obtained using symbolic calculations

and conversion to double precision numbers, are

λ = [2.031200536560380·10

−9

;1.172582399979688·10

2

];

the SLICOT periodic Schur eigensolver returned

b

λ = [2.031200097007968·10

−9

;1.172582399979688·10

2

],

and the transformed matrices

e

A

1

and

e

A

2

−3.096329932867903·10

−4

1.552701519915428

0 −4.395524985047830

−6.560024032069280·10

−6

−9.422786660123904

0 −26.67673153813540

respectively. Therefore, the eigenvalues of the prod-

uct of the transformed matrices, computed as products

of the corresponding diagonal elements are

e

λ = [2.031199877082891·10

−9

;1.172582399952876·10

2

].

The element-wise absolute and relative errors be-

tween

b

λ and λ are about 4.40·10

−16

and 4.26·10

−14

,

and 2.16·10

−7

and 3.64·10

−16

, respectively. The last

value is also the approximate global relative error, i.e.,

k

b

λ −λk/kλk, using Euclidean norm. On the other

hand, the element-wise absolute and relative errors

between

e

λ and λ are about 6.59·10

−16

and 2.68·10

−9

,

and 3.25·10

−7

and 2.29·10

−11

; the last value is the

approximate global relative error of

e

λ compared to λ.

Clearly, although obtained using orthogonal trans-

formations only, the transformed matrices

e

A

i

, i = 1,2,

are inaccurate, and therefore

e

λ

i

are less accurate than

b

λ

i

. The inaccuracy of

e

A

i

is due to the ill-conditioning

of the matrix product A

1

A

2

, and the way the periodic

Schur algorithm works. The residual matrices of

e

A

i

,

i = 1, 2, have the following approximate values

R

1

=

0 4.44·10

−16

2.85·10

−10

0

,

R

2

=

5.26·10

−16

1.78·10

−15

1.78·10

−15

0

.

The largest residual appears in the (2,1) element of

R

1

. While this element should be zero, and numeri-

cally its magnitude should be of the order of ε

M

, in

the best case, the ill-conditioning of the matrix prod-

uct has determined its increase by six orders of mag-

nitude.

After updating the computed matrix

e

A

1

only and

using an additional sweep on the matrix sequence,

which is now in periodic Hessenberg-triangular form,

the new residuals have all elements equal to 0, except

for the (2,1) element of the new residual R

2

, which has

a value about 4.25·10

−16

. Moreover, the global resid-

uals, given by the difference between the matrices re-

turned by the additional sweep and those obtained us-

ing (1) with Z

i

replaced by Z

i

Y

i

, have all values with

magnitude comparable to ε

M

. The largest residual el-

ement is now the (1,2) element in the second residual

matrix, whose value is about 3.55·10

−15

. Also, the

eigenvalues of the matrix sequence returned after the

additional sweep coincide to those of

e

A

1

1

e

A

1

2

and are

b

λ

1

= [2.031200536459228·10

−9

;1.172582399979688·10

2

].

The second eigenvalue,

b

λ

1

2

, practically coincides to

λ

2

and

b

λ

2

, and the first 10 digits of

b

λ

1

1

coincide to

those of λ

1

, hence it has three additional correct dig-

its compared to

b

λ

1

. The element-wise absolute and

relative errors between

b

λ

1

and λ are about 1.01·10

−19

and 4.42·10

−14

, and 4.98·10

−11

and 1.21·10

−16

, re-

spectively, hence there is an improvement of 4 and 5

orders of magnitude compared to

e

λ. If

e

A

2

is also up-

dated as

e

A

1

, there is no noticeable improvement.

Many other 2 ×2 examples with a similar or even

worse behaviour have been found. In one case, the

(2,1) entry of R

1

had a value of order 10

−6

, but one ad-

ditional sweep reduced its magnitude to about 10

−22

.

Larger order examples have also been tried, and be-

haved better than the 2 ×2 case. For instance, for an

example with four 10 ×10 factors, the relative error

between

b

λ and λ (obtained with symbolic computa-

tions) has been 6.46·10

−16

, and the Frobenius norm

of the stacked residuals was 5.56·10

−12

.

The experiments have also shown that the eigen-

values conditioning does not depend on the condition-

ing of the matrix product.

PitfallsWhenSolvingEigenproblems-WithApplicationsinControlEngineering

175

4 ACCURACY OF EIGENVALUES

FOR SKEW-HAMILTONIAN/

HAMILTONIAN PROBLEMS

Often, badly scaled matrices or matrix pencils have

eigenvalues with magnitudes covering a large inter-

val. A structured matrix pencil example will be

discussed below. Consider a real 2m × 2m skew-

Hamiltonian/ Hamiltonian pencil αS −βH , with

S =

A D

E A

T

, H =

C V

W −C

T

, (2)

where D and E are skew-symmetric (D = −D

T

, E =

−E

T

), V and W are symmetric, and define J as

J =

0 I

m

−I

m

0

.

The eigenvalues for the real pencil αS −βH in (2)

are symmetric with respect to both real and imaginary

axes of the complex plane. Real or purely imaginary

eigenvalues appear in pairs λ, −λ (or λ,

¯

λ, in the sec-

ond case), while complex conjugate eigenvalues ap-

pear in quadruples, λ, −λ,

¯

λ, and −

¯

λ. Using two

orthogonal transformations, Q

1

and Q

2

, the structure-

exploiting algorithm computes the transformed matri-

ces

e

S,

e

T , and

e

H , so that

Q

T

1

SJ Q

1

J

T

=

e

A

e

D

0

e

A

T

:=

e

S,

J

T

Q

T

2

J SQ

2

=

e

B

e

F

0

e

B

T

:=

e

T ,

Q

T

1

H Q

2

=

e

C

1

e

V

0

e

C

T

2

:=

e

H , (3)

where

e

A,

e

B,

e

C

1

are upper triangular,

e

C

2

is upper

quasi-triangular (i.e., block upper triangular with 1 ×

1 or 2 × 2 diagonal blocks) and

e

D,

e

F are skew-

symmetric. Specifically, the first step reduces S to

skew-Hamiltonian triangular form, using Givens rota-

tions and Householder reflections, and updates A and

D in S, as well as C, V , and W in H correspond-

ingly, producing A

1

, ..., W

1

, respectively. Let S

1

and

H

1

be the obtained matrices, where the two diago-

nal blocks of H

1

are C

1

= C

1

and C

2

= −C

1

. A

skew-Hamiltonian block upper triangular matrix T

1

is built using B

1

= A

1

and F

1

= D

1

. Then, addi-

tional transformations are used to reduce the matrix

H

1

to a block upper triangular form, while updating

A

1

, D

1

, B

1

and F

1

to preserve their form or struc-

ture. Let

b

A,

b

D,

b

B,

b

F,

b

C

1

,

b

V , and

b

C

2

be the obtained

matrices, and

b

S,

b

T , and

b

H the block matrices built

from them, where

b

A,

b

B, and

b

C

1

are upper triangular,

b

D and

b

F are skew-symmetric, and

b

C

2

is upper Hes-

senberg. Finally, the periodic QZ algorithm is applied

to transform

b

C

2

to upper quasi-triangular form, while

preserving the upper triangular form of

b

A,

b

B, and

b

C

1

.

Specifically, the formal matrix product

b

C

2

b

A

−1

b

C

1

b

B

−1

is transformed without using matrix products and in-

verses. (Actually,

b

A and

b

B may be singular.) The

eigenvalues of the pencil αS −βH are the positive

and negative square roots of the eigenvalues of the

formal matrix product −

b

C

2

b

A

−1

b

C

1

b

B

−1

.

Example 3. In the computation of the H

∞

-norm

of a linear control system, an 18 × 18 skew-

Hamiltonian/Hamiltonian pencil was found for which

changes in scaling led to one small imaginary eigen-

value becoming real. The case with changes in scal-

ing will be referred to as Test 1 below, while the case

without changes will be referred to as Test 2. Specif-

ically, the two smallest eigenvalues were about 2.52·

10

−5

ı and 8.66·10

−4

ı for Test 2 data, but 2.30·10

−3

ı

and 1.83·10

−5

for Test 1 data. The final effect was

obtaining a wrong H

∞

-norm in the Test 1 case. A de-

tailed investigation of the associated numerical issue

has been performed.

Our specific example has m = 9 and a simple

structure. Specifically, A is diagonal with a

ii

= a

11

,

i = 2 : 7, a

j j

= 0, j = 8 : 9, C is almost upper triangu-

lar, with c

:,9

= 0, but c

i,i−1

, i = 3 : 7, c

8,1:2

and c

9,2:7

are nonzero; moreover, D = E = 0 and V and W are

diagonal, with v

ii

= w

ii

= 0, i = 1 : 7, v

j j

= −1 and

w

j j

= 1, j = 8 : 9; all other elements are 0. There

are four infinite eigenvalues. The only differences be-

tween Test 1 and Test 2 data are in the nonzero ele-

ments of A and C.

The first idea was to suspect an error in the SLI-

COT Library (Benner et al., 1999; Van Huffel et al.,

2004; Benner et al., 2013a; Benner et al., 2013b) rou-

tines used, i.e., in subroutine MB04BD or in one of the

routines it calls, e.g., a wrong decision test. But a step

by step analysis of the intermediate results proved

their correctness. Indeed, the transformed matrices

computed from the Test 1 data, including

b

A,

b

D,

b

B,

b

F,

b

C

1

,

b

V , and

b

C

2

(obtained in MB04BD just before call-

ing the periodic QZ algorithm), satisfy the required

structure and the needed relationships with the ini-

tial skew-Hamiltonian/Hamiltonian pencil. The max-

imum relative error is 2.42·10

−16

. The finite and

“positive” eigenvalues of the reduced problem, com-

puted using symbolic calculations, immediately after

the infinite part has been deflated, agree in position,

and within a relative error of about ε

1/2

M

, to those re-

turned by MB04BD.

The deflation which separated the finite and infi-

nite spectra has been produced at the end of the sec-

ICINCO2015-12thInternationalConferenceonInformaticsinControl,AutomationandRobotics

176

ond iteration of the periodic QZ algorithm, hence few

more operations were applied on copies of

b

C

1

,

b

A,

b

C

2

,

and

b

B; moreover, the orthogonal matrices used, Z

1

,

..., Z

4

, have a very simple structure (slightly modified

identity matrices). Also, the transformed matrices,

denoted with check accent, satisfy the needed trans-

formation rules, i.e.,

ˇ

C

2

= Z

T

1

b

C

2

Z

2

,

ˇ

A = Z

T

3

b

AZ

2

,

ˇ

C

1

=

Z

T

3

b

C

1

Z

4

,

ˇ

B = Z

T

1

b

BZ

4

, so that the resulting formal

matrix product is

ˇ

C

2

ˇ

A

−1

ˇ

C

1

ˇ

B

−1

= Z

T

1

b

C

2

b

A

−1

b

C

1

b

B

−1

Z

1

.

The maximum relative error is about 2.25 ·10

−15

.

Moreover, the 7 ×7 trailing submatrices of

b

A and

b

B,

used as coefficient matrices in the two linear systems

corresponding to the finite spectrum, solved for ob-

taining the true matrix product using symbolic cal-

culations, have quite small condition numbers, about

9.36·10

3

and 3.39, respectively.

In addition to the analysis above, the reciprocal

condition numbers for eigenvalues and eigenvectors

for both Test 1 and Test 2 eigenproblems, with or

without balancing, have been computed. It was found

that the small eigenvalues for the Test 1 data are more

ill-conditioned than those for the Test 2 data. Omit-

ting the eigenvalues larger than 10

5

, including the in-

finite ones, the LAPACK driver DGGEVX without bal-

ancing returned the “small” eigenvalues and associ-

ated approximate condition information shown in Ta-

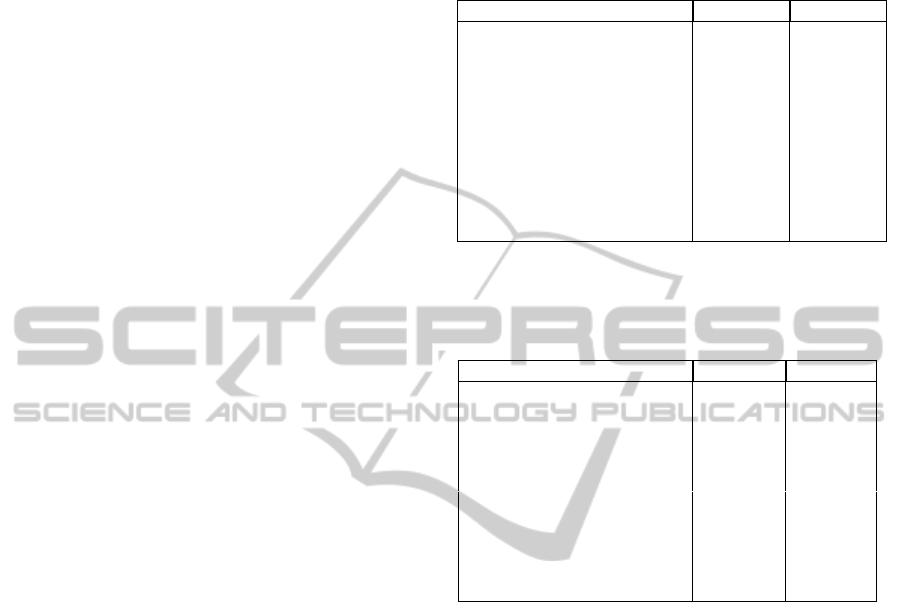

ble 2 for the Test 1 data. Note that there is just one

pair of complex conjugate eigenvalues instead of two.

Pairing is not as needed, and the eigenvalues which

should be paired do not agree well. The last eigen-

value should be paired to the third one above it (i.e.,

to 9.0169···73·10

−6

). There are at most eight iden-

tical significant digits in the paired eigenvalues. The

complex pair and the real pair of eigenvalues men-

tioned above have the smallest reciprocal condition

numbers (of order 10

−15

), hence they are very sensi-

tive. The one-norms of the matrices S and H were

about 2.3842·10

−7

and 7.3736, respectively.

Using instead DGGEVX with balancing (permuta-

tions and scaling), returned good results, as shown

in Table 3. Note that the pairing is much better than

in Table 2, and the eigenvalues are closer to their re-

quired position. The accuracy increased to at most

12 identical significant digits in the paired eigenval-

ues. Also, the conditioning has been significantly

improved for all eigenvalues. The one-norms of the

balanced skew-Hamiltonian and Hamiltonian matri-

ces were about 2.3842 and 4287.7. With scaling only,

the results are similar, so we omit them.

Using the scaling factors returned by DGGEVX

to scale the input matrices for a MEX-file based

on SLICOT subroutine MB04BD, the following finite

eigenvalues (including the “large” ones) have been

obtained:

Table 2: The small eigenvalues and associated approxi-

mate condition numbers for eigenvalues, rcond(λ

i

), and for

eigenvectors, rcond(x

i

), computed using DGGEVX without

balancing for the Test 1 data.

λ

i

rcond(λ

i

) rcond(x

i

)

7.982789077728958·10

2

4.5·10

−9

1.4·10

−11

−7.982789039705131·10

2

4.5·10

−9

4.6·10

−11

−2.258073833805364·10

1

5.1·10

−12

5.9·10

−11

2.258073628829316·10

1

5.1·10

−12

2.8·10

−11

6.345831704138784·10

−6

±1.654595668192905·10

−3

ı 3.4·10

−15

8.4·10

−14

9.016920132336973·10

−6

2.0·10

−15

1.8·10

−18

−5.180515230574346 1.0·10

−13

1.7·10

−11

5.180514112635106 1.0·10

−13

1.5·10

−11

−2.180898342048099·10

−5

3.0·10

−15

1.8·10

−18

Table 3: The small eigenvalues and associated approxi-

mate condition numbers for eigenvalues, rcond(λ

i

), and for

eigenvectors, rcond(x

i

), computed using DGGEVX with bal-

ancing for the Test 1 data.

λ

i

rcond(λ

i

) rcond(x

i

)

7.982789076557393·10

2

4.1·10

−3

3.1·10

−5

−7.982789076562744·10

2

4.1·10

−3

5.5·10

−5

−2.258073819582842·10

1

2.3·10

−2

2.7·10

−4

2.258073819581395·10

1

2.3·10

−2

1.5·10

−4

−5.180514839367283 5.6·10

−3

9.9·10

−5

5.180514839369767 5.6·10

−3

1.0·10

−4

2.631383527274714·10

−9

±8.649722516061533·10

−4

ı 2.3·10

−8

1.6·10

−7

−2.631570224527866·10

−9

±2.522221870167959·10

−5

ı 1.0·10

−7

1.6·10

−5

λ =

8.860295592973415·10

6

ı

1.009148542240609·10

5

ı

7.982789076561136·10

2

2.258073819582885·10

1

5.180514839373116

2.521340745136690·10

−5

ı

8.652245367690063·10

−4

ı

.

This is the expected result for this data, but it was not

returned as such by MB04BD with no scaling. Note that

only the eigenvalues with positive real parts and, for

purely imaginary eigenvalues, only those with posi-

tive imaginary parts are listed. The other half of the

spectrum is obtained by symmetry.

All calculations above have been repeated for the

Test 2 data, and similar results have been obtained.

This problem is less sensitive. Better conditioning

than for the Test 1 data has been obtained for all bal-

ancing options. Indeed, the reciprocal condition num-

bers for the small eigenvalues are about one order of

magnitude larger than for the Test 1 data eigenprob-

lem, hence the condition numbers are smaller.

The analysis in Example 3 suggests that it would

be useful to include in the computational solver an op-

PitfallsWhenSolvingEigenproblems-WithApplicationsinControlEngineering

177

tion for balancing the skew-Hamiltonian/Hamiltonian

eigenproblem data, preserving the structure.

5 CONCLUSIONS

Numerical algorithms for the solution of common and

structured eigenproblems, encountered in many con-

trol theory applications and in other domains, have

been investigated. Eigenvalue computations for stan-

dard as well as formal matrix products have been

considered, and their accuracy and conditioning has

been discussed. Simple examples highlight the pit-

falls which may appear in such numerical computa-

tions, using state-of-the-art solvers. An iterative re-

finement process for the periodic Schur decomposi-

tion (not yet offered by software packages) is pro-

posed, and the improvement of the results is illus-

trated. Balancing the matrices or matrix pencils and

the use of condition number estimates for eigenvalues

are shown to be essential options in investigating the

behavior of the solvers and problem sensitivity.

REFERENCES

Anderson, E., Bai, Z., Bischof, C., Blackford, S., Demmel,

J., Dongarra, J., Du Croz, J., Greenbaum, A., Ham-

marling, S., McKenney, A., and Sorensen, D. (1999).

LAPACK Users’ Guide. SIAM, Philadelphia, third

edition.

Benner, P. (1999). Computational methods for linear-

quadratic optimization. Supplemento ai Rendiconti

del Circolo Matematico di Palermo, II, (58):21–56.

Benner, P., Byers, R., Losse, P., Mehrmann, V., and

Xu, H. (2007). Numerical solution of real skew-

Hamiltonian/Hamiltonian eigenproblems. Technical

report, Technische Universit

¨

at Chemnitz, Chemnitz.

Benner, P., Byers, R., Mehrmann, V., and Xu, H. (2002).

Numerical computation of deflating subspaces of

skew Hamiltonian/Hamiltonian pencils. SIAM J. Ma-

trix Anal. Appl., 24(1):165–190.

Benner, P. and Kressner, D. (2006). Fortran 77 subroutines

for computing the eigenvalues of Hamiltonian matri-

ces II. ACM Trans. Math. Softw., 32(2):352–373.

Benner, P., Kressner, D., Sima, V., and Varga, A.

(2010). Die SLICOT-Toolboxen f

¨

ur Matlab. at—

Automatisierungstechnik, 58(1):15–25.

Benner, P., Mehrmann, V., Sima, V., Van Huffel, S., and

Varga, A. (1999). SLICOT — A subroutine library

in systems and control theory. In Applied and Com-

putational Control, Signals, and Circuits, 1, ch. 10,

pp. 499–539. Birkh

¨

auser, Boston.

Benner, P., Sima, V., and Voigt, M. (2012a). L

∞

-norm com-

putation for continuous-time descriptor systems us-

ing structured matrix pencils. IEEE Trans. Automat.

Contr., AC-57(1):233–238.

Benner, P., Sima, V., and Voigt, M. (2012b). Robust and

efficient algorithms for L

∞

-norm computations for de-

scriptor systems. In 7th IFAC Symposium on Robust

Control Design, pp. 189–194.

Benner, P., Sima, V., and Voigt, M. (2013a). FOR-

TRAN 77 subroutines for the solution of skew-

Hamiltonian/Hamiltonian eigenproblems. Part I: Al-

gorithms and applications. www.slicot.org.

Benner, P., Sima, V., and Voigt, M. (2013b). FOR-

TRAN 77 subroutines for the solution of skew-

Hamiltonian/Hamiltonian eigenproblems. Part II: Im-

plementation and numerical results. www.slicot.

org.

Bojanczyk, A. W., Golub, G., and Van Dooren, P. (1992).

The periodic Schur decomposition: algorithms and

applications. In SPIE Conference Advanced Signal

Processing Algorithms, Architectures, and Implemen-

tations III, 1770, pp. 31–42.

Golub, G. H. and Van Loan, C. F. (1996). Matrix Computa-

tions. The Johns Hopkins University Press, Baltimore,

Maryland, third edition.

Granat, R., K

˚

agstr

¨

om, B., and Kressner, D. (2007). Com-

puting periodic deflating subspaces associated with a

specified set of eigenvalues. BIT Numerical Mathe-

matics, 47(4):763–791.

Laub, A. J. (1979). A Schur method for solving algebraic

Riccati equations. IEEE Trans. Automat. Contr., AC–

24(6):913–921.

MathWorks (2014). MATLAB

R

: The Language of Techni-

cal Computing. R2014b. The MathWorks, Inc.

Mehrmann, V. (1991). The Autonomous Linear Quadratic

Control Problem. Theory and Numerical Solution.

Springer-Verlag, Berlin.

Sima, V. (1996). Algorithms for Linear-Quadratic Opti-

mization. Marcel Dekker, Inc., New York.

Sima, V. (2010). Structure-preserving computation of stable

deflating subspaces. In 10th IFAC Workshop “Adapta-

tion and Learning in Control and Signal Processing”.

Sima, V. (2011a). Computational experience with structure-

preserving Hamiltonian solvers in optimal control. In

8th International Conference on Informatics in Con-

trol, Automation and Robotics, vol. 1, pp. 91–96.

SCITEPRESS.

Sima, V. (2011b). Computational experience with structure-

preserving Hamiltonian solvers in complex spaces. In

5th International Scientific Conference on Physics and

Control.

Sima, V., Benner, P., and Kressner, D. (2012). New SLI-

COT routines based on structured eigensolvers. In

2012 IEEE International Conference on Control Ap-

plications, pp. 640–645. Omnipress.

Van Huffel, S., Sima, V., Varga, A., Hammarling, S., and

Delebecque, F. (2004). High-performance numeri-

cal software for control. IEEE Control Syst. Mag.,

24(1):60–76.

ICINCO2015-12thInternationalConferenceonInformaticsinControl,AutomationandRobotics

178