KNOWLEDGE REPRESENTATION AND COST MANAGEMENT

FOR SUPPLY CHAINS

K. Donald Tham

Dept. of Mechanical and Industrial Engineering, Ryerson University, Toronto, Ontario, M5B2K3, Canada

Keywords: SCEM, SCM, enterprise model, ontology, knowledge representation, Temporal-ABC, resource cost units,

cost fluents, period overhead costs, non-period overhead costs.

Abstract: The intent of this research is to make a contribution to SCEM (supply chain event management) and SCM

(supply chain management) systems. nowledge representation (KR) of a supply chain is modelled by the

“linking” of activity-state-resource clusters that represent activities of the supply chain. A formalization of

the costs of resources (i.e., resource cost units) is presented. Traditional overhead costs entities are

represented as period and non-period cost resources that may be deployed consistently, unambiguously and

with high traceability in Temporal-ABC

TM

(registered trademark of Nulogy Corporation). KR and cost

management enhances the effectiveness and efficiency of SCEM and SCM systems.

1 INTRODUCTION

Supply chains “link” enterprises together locally

and/or across the globe. SCEM is an application that

supports control processes for managing events

within and amongst companies. It consists of

integrated software functionality that supports five

business processes: monitor, notify, simulate,

control and measure supply chain activities. SCM is

an integrating function with primary responsibility

for linking major business functions and business

processes within and across companies into a

cohesive and high-performing business model. To

improve SCEM and SCM systems, this research puts

forth:- (i) a KR for supply chains; (ii) a

formalization of resource costs units and overheads

for Temporal-ABC so that activity costs are

consistent, unambiguous, accurate and traceable

throughout the supply chain.

The basic or primitive cost value of 1 unit of a

resource consumed or used by the enabling state of

an activity is defined as the resource cost unit of the

resource for the activity. Overheads are comprised

of the more "nebulous entities" of traditional

overhead and indirect costs such as depreciation of

factory/office buildings and equipment, taxes on real

estate, rent, insurance on factory building and

equipment, supplementary employee benefits for

management and unionized personnel, salaried and

non-salaried personnel, and similar expenses that are

incurred by enterprises.

2 TOVE, RESOURCE COST

UNITS, TIME

AND COST BEHAVIOUR IN

TEMPORAL-ABC

Supply chains link different enterprises together

based upon various activities performed by each of

the enterprises. Enterprises are action oriented, and

therefore, the ability to represent action lies at the

heart of representing a supply chain through the

activities of these linked enterprises. At the

Enterprise Integration Laboratory (EIL) of the

University of Toronto, a formal approach is taken to

the modeling of enterprises. Formal models do not

refer to analytical models as found in Operations

Research, but to logical models as found in

Computer Science. The TOVE (TOronto Virtual

Enterprise) Project at EIL includes two major

undertakings: the development of an Enterprise

Ontology and a Testbed (Fox et al., 1993).

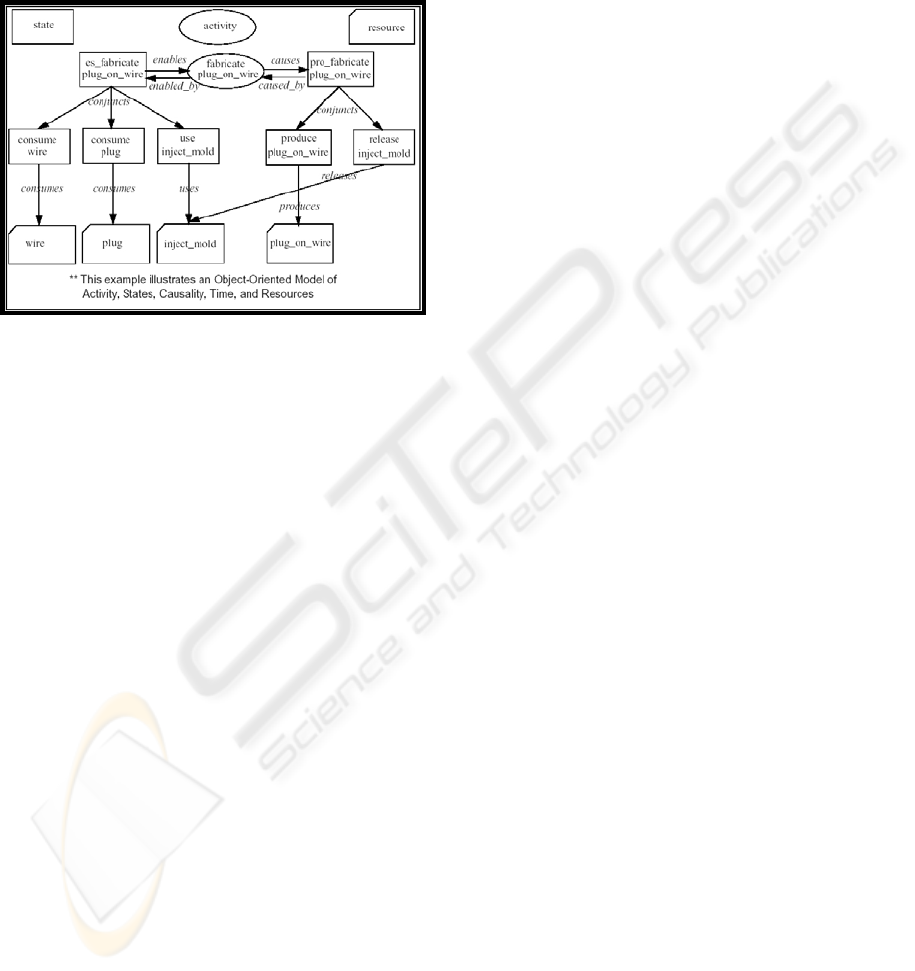

The formal activity-state-resource cluster (Fig. 1)

of TOVE is deployed for the representation of each

activity of the supply chain. In TOVE, action is

represented by the combination of an activity and its

363

Donald Tham K. (2008).

KNOWLEDGE REPRESENTATION AND COST MANAGEMENT FOR SUPPLY CHAINS.

In Proceedings of the Tenth International Conference on Enterprise Information Systems - ISAS, pages 363-366

DOI: 10.5220/0001718503630366

Copyright

c

SciTePress

corresponding enabling and caused states. An

activity is the basic transformational action primitive

with which processes and operations can be

represented. An activity specifies a transformation of

the world. Its status is reflected in an attribute called

status. The domain of an activity’s status is a set of

linguistic constants:

Figure 1: Activity-State Resource Cluster.

• Dormant – the activity is idle and has never been

executing before.

• Executing – the activity is executing.

• Suspended – the activity was executing and has

been forced to an idle state.

• ReExecuting – the activity is executing again.

• Completed – the activity has finished.

"Being a resource" is not an innate property of an

object, but is a property that is derived from the role

an object plays with respect to an activity (Fadel

et.al, 1994). The resource ontology includes the

concepts of a resource being divisible, quantifiable,

consumable, reusable, a component of, committed

to, and having usage and consumption

specifications.

A state in TOVE represents what has to be true in

the world for an activity to be performed. An

enabling state defines what has to be true of the

world in order for the activity to be performed. A

caused state defines what will be true of the world

once the activity has been completed. An activity

along with its enabling and caused state is called an

activity-state resource cluster (Fig.1) or simply

activity cluster.

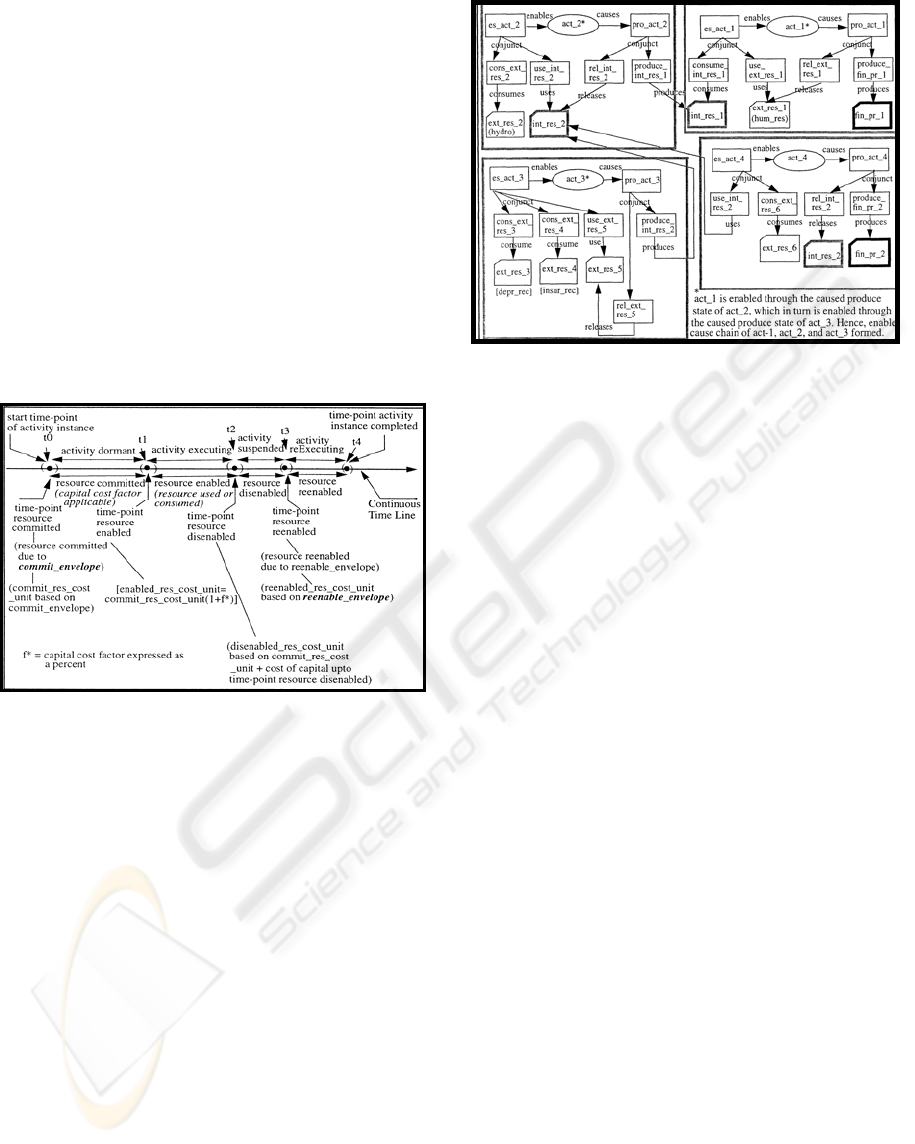

The status of a state, and any activity, is

dependent on the status of the resources that the

activity uses or consumes. All states are assigned a

status with respect to a point in time. There are five

different status predicates:- (i) committed - a unit of

the resource that the state consumes or uses has been

reserved for consumption or usage; (ii) enabled - a

unit of the resource that the state consumes or uses is

being consumed or used while the activity is

executing; (iii) disenabled - a unit of the resource

that the state consumes or uses has become

unavailable and the activity is suspended; (iv)

reenabled - a unit of the resource that the state

consumes or uses is re-available for the activity to

resume or reExecute; (v) completed – a unit of the

resource that the state consumes or uses has been

consumed or used and is no longer needed.

The resource cost unit of a resource is the cost of

a unit of the resource in the state that it exists in the

real world at some time point. The commit-resource-

cost-unit, the enabled-resource-cost-unit, the

disenabled-resource-cost-unit and the reenabled -

resource-cost-unit are respectively associated with

the commit, enabled, disenabled and reenabled states

associated with a resource.

For SCEM, representation of time is essential. As

in TOVE, time is represented by points and periods

(intervals) on a continuous time line (Fig.2) based on

Allen’s temporal relations (Allen, 1983).

Previously introduced, the Principle of Temporal-

ABC (Tham & Fox, 2004) states:- “A cost object,

i.e., a product or service, is the reason why activities

are performed. The assignment of costs to activities

is based upon their requirements of resources and

the possible changing temporal states of those

resources, thereby resulting in temporal costs for

activities. The cost of a cost object is based upon the

temporal costs of activities that produce it.”

In keeping with the Principle of Temporal-ABC,

the KR of activity, state, resource and time explicitly

recognizes the temporal status of the states

associated with the resources required by an activity,

which in turn affect the status of the activity.

To understand cost behaviour in Temporal-ABC,

resource cost units of a resource are explained as

follows (Fig. 2):

1. Committed Resource Cost Unit: A resource

that is committed to an activity may be viewed as

"inventory committed to the activity". From a

costing standpoint, the cost of borrowing the money

must be charged as the cost of capital (usually

expressed as some percentage factor) against the

activity to which the resource is committed.

2. Enabled Resource Cost Unit: The enabled

resource cost unit metric is taken to be equivalent to

the committed resource cost unit metric as each unit

of resource required by the executing activity costs

an amount equal to its commit resource cost unit.

ICEIS 2008 - International Conference on Enterprise Information Systems

364

3. Disenabled Resource Cost Unit: A disenabled

resource brings about the suspension of an executing

activity that requires it. The enterprise experiences

“lost opportunities” during this suspension. Hence,

from a costing standpoint, a lost opportunity cost

factor (usually some percentage factor) must be

taken into consideration when computing the

disenabled resource cost for an activity.

4. Reenabled Resource Cost Unit: The "repair" of

a disenabled resource, reenables the resource.

Hence, the cost value of a reenabled resource is

greater than that of the initial enabled resource

simply because the cost of "repair" activities must be

sunk into the disenabled resource. An enterprise may

consider cumulatively incrementing the value of the

reenabled resource cost unit with each iteration that

a resource is disenabled and then reenabled.

Figure 2: Activity Instance on Continuous Time Line.

3 KR OF A SUPPLY CHAIN

WITH ACTIVITY CLUSTERS

Activities of a supply chain are represented through

the activity-cluster representation. As illustrated in

Fig. 3, the activities of a supply chain are formed

through the linkages of the activity clusters. By way

of explanation, the activity, act_1, consumes a

resource, int_res_1. The activity, act_2, produces

int_res_1. More precisely, the enabling state of act_1

is linked to the caused state of act_2, thereby

forming an enable_cause link between act_1 and

act_2. However, the activity, act_2, requires the

resource, int_res_2. The resource, int_res_2, in turn

is produced by the activity, act_3. We now have an

enable_cause link between act_2 and act_3. Thus

far, the two links form the enable_cause chain to

consist of three activities sequenced as (act_3, act_2,

act_1). In order to produce the resource, int_res_2,

the activity, act_3, requires resources, ext_res_3 and

Figure 3: Activity Clusters of Supply Chain (activity

clusters boxed).

ext_res4 and ext_res_5. For this illustration, assume

that ext_res_3, ext_res_4 and ext_res_5 are

resources that are supplied from sources (or

companies) external to the enterprise modeled.

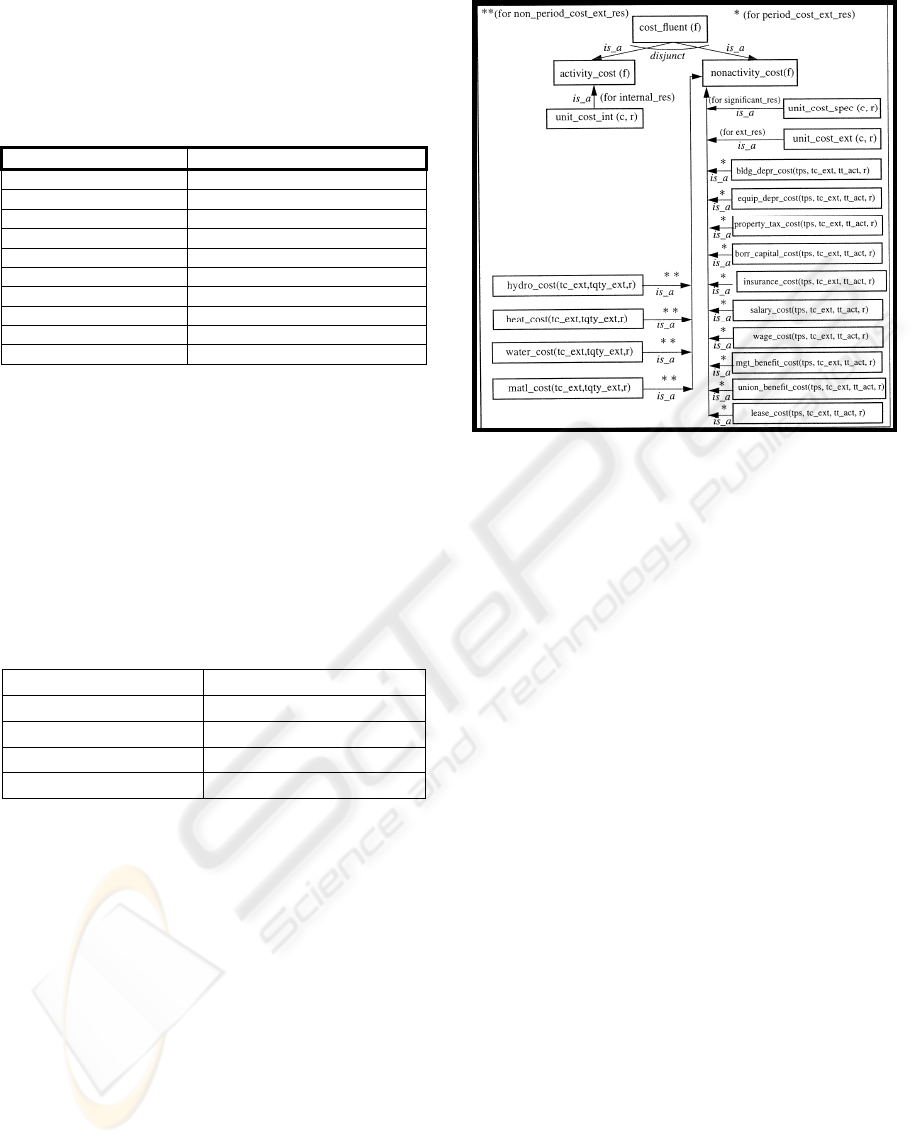

4 COST FLUENTS AND

OVERHEAD TAXONOMIES

In AI, a fluent is a condition that can change over

time. In logical approaches to reasoning about

Temporal-ABC costs in a supply chain, cost fluents

can be represented in first-order logic (FOL, i.e., a

formal language which supports expressing

propositions as well as predicates, where predicates

may have quantified variables as arguments) by

predicates having an argument that depends on time.

Period cost external resources are defined as

nonactivity cost fluents f based upon traditional time

period related overhead cost categories such as

building depreciation, equipment depreciation,

property taxes, borrowed capital interest, insurance,

salaries, wages, management/union supplemental

benefits, (refer Table 1), where:- f is a predicate

denoting class of nonactivity cost fluent for

overhead cost; tps denotes the time period under

study (e.g., 1 year, 6 months, etc.); tc_ext is an

externally given total nonactivity based cost

applicable to tps (e.g., if the fixed overhead of

depreciation is under study for tps = 1 year, then

tc_ext would be the annual depreciation cost); tt_act

is a total actual time or total estimated time for the

number of instances that occur in tps; r is the name

of the external resource associated with the

nonactivity cost fluent. If an enterprise has other

KNOWLEDGE REPRESENTATION AND COST MANAGEMENT FOR SUPPLY CHAINS

365

overhead cost entities, e.g., training, safety, etc., a

corresponding class of nonactivity cost fluent of the

form f(tps, tc_ext, tt_act, r) may be defined.

Table 1: Nonactivity Cost Fluents for Time Period

Overhead (OH) Costs.

Period Overhead Cost Nonactivity Cost Fluents

Building depreciation bldgDepCost(tps, tc_ext,tt_act, r)

Equipment depreciation eqDepCost(tps, tc_ext,tt_act, r)

Property taxes propTaxCost(tps, tc_ext,tt_act, r)

Borrowed capital interest borCapCost(tps, tc_ext,tt_act, r)

Insurance bldgDepCost(tps, tc_ext,tt_act, r)

Salaries salaryCost(tps, tc_ext,tt_act, r)

Wages wageCost(tps, tc_ext,tt_act, r)

Management benefits mgtBenCost(tps, tc_ext,tt_act, r)

Union benefits unnBenCost(tps, tc_ext,tt_act, r)

Leases leaseCost(tps, tc_ext,tt_act, r)

Non-period cost external resources are defined as

cost fluents f based upon traditional non-period

overhead cost categories such as material costs, and

utility costs like hydro, heat and water. The non-

period nonactivity cost fluents are shown in Table 2,

where tc_ext denotes a specified nonactivity-based

total cost parameter distributed over the total

quantity parameter tqty_ext associated with the

particular cost category.

Table 2: Nonactivity Cost Fluents for Non-period

Overhead (OH) Costs.

Non-period OH Costs

Nonactivity Cost Fluents

Hydro hydroCost( tc_ext,tqty_ext, r)

Heat heatCost( tc_ext,tqty_ext, r)

Water waterCost( tc_ext,tqty_ext, r)

“indirect materials” matlCost( tc_ext,tqty_ext, r)

First, the Cost Fluent Taxonomy (Fig. 4)

classifies cost fluents as being activity-based or

nonactivity-based so that unit costs of resources may

be deduced based upon some period of time or some

quantity associated with a resource, thereby drawing

upon the distinction between period cost resources

and non-period cost resources respectively. Second,

this taxonomy contains several defined classes of

nonactivity-based cost fluents to formalize the

concepts of the ever increasing traditional overhead

costs that are typically difficult to trace, allocate and

accurately compute otherwise (Tham, 1999).

Figure 4: Cost Fluent Taxonomy with Associated

Resource Classes.

5 CONCLUSIONS

By linking activity clusters, KR of supply chains is

achieved. The cost fluents introduced promote

reasoning of costs with Temporal-ABC and make

overheads traceable in activity clusters of a supply

chain.

REFERENCES

Allen, James F., 1983. Maintaining Knowledge about

Temporal Intervals, David Waltz (editor),

Communications of the ACM, Vol.26, No.11, pp.832-

843.

Fadel, F.G., Fox, Mark S. and Grüninger, M., 1994. A

Generic Enterprise Resource Ontology, Proceedings of

Third Workshop on Enabling Technologies: (WET-

ICE), Morgantown, WV., USA, pp. 117-128.

Fox, Mark S., Chionglo, John F., Fadi G., 1993. Towards

Common Sense Modelling of an Enterprise,

Proceedings of the Second Industrial Engineering

Research Conference, Norcross, GA., pp. 425-429.

Tham, K. Donald, 1999. Representing and Reasoning

about Costs using Enterprise Models and ABC, Ph.D.

Thesis, University of Toronto, Ontario, Canada.

Tham, K.Donald and Fox, Mark S., 2004. Determining

Requirements and Specifications of Enterprise

Information Systems, Proceedings of the Sixth ICEIS,

Porto, Portugal, pp.391-398.

ICEIS 2008 - International Conference on Enterprise Information Systems

366